imaginima/E+ via Getty Images

By OpenMarkets

Oil markets have been in focus since conflict began in the Middle East in late February, with prices at times surging past $100 per barrel. However, this time around, even as the effective closure of the Strait of Hormuz has removed a historically unprecedented share of global supply, prices have risen far less dramatically than past disruptions.

What explains this disconnect? And what does the move into backwardation – where prices for near-term delivery rise above prices for delivery further in the future – signal for investors navigating this volatile environment?

Erik Norland, CME Group’s Chief Economist, sat down with OpenMarkets to discuss what 40 years of market data reveals about oil futures dynamics during periods of backwardation. This conversation has been edited for brevity.

Can you explain what the current backwardation in the WTI Crude Oil futures curve tells us about market expectations for supply and demand?

It suggests that investors expect things to return to normal. In the near term, the market is disrupted with reduced supply coming out of the Middle East, pushing near-term prices to around $100 per barrel. However, the market seems to expect prices could return to around $75 by year-end if conditions normalize. Keep in mind, these are just market expectations, and they’re constantly changing.

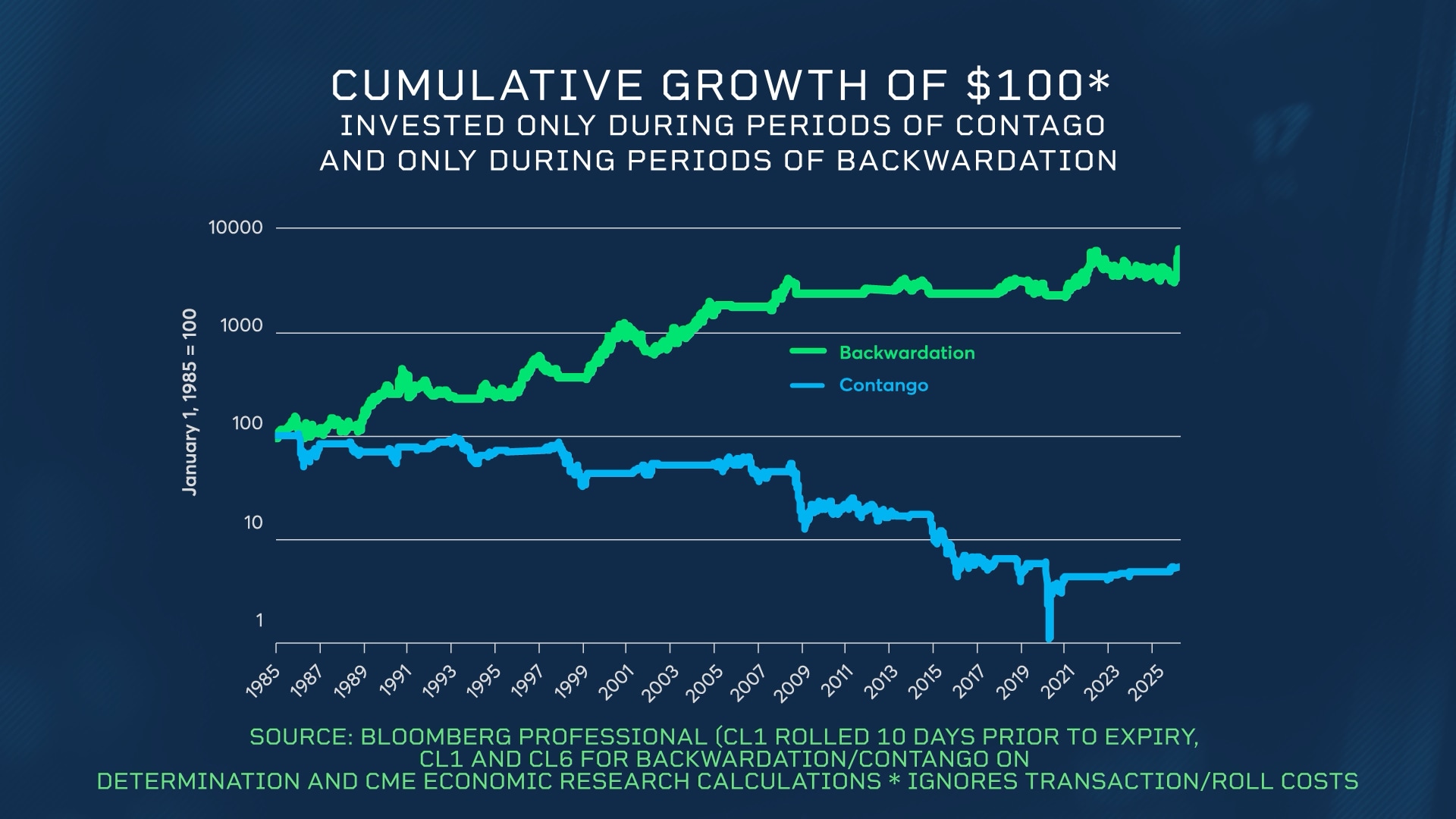

What historical trends or patterns have you observed in crude oil returns when the market structure is in contango compared to backwardation?

Since around 1985, a consistent pattern has emerged. When holding a long position during periods of contango, crude oil positions often (but not always) lose capital. By contrast, a long position in crude oil during periods of backwardation typically shows positive returns over time – though again, not always. There are always exceptions to every rule.

This pattern suggests that traders have historically underestimated the length of time markets remain oversupplied (in the case of contango) and undersupplied (in the case of backwardation).

What role do interest rates play in contango and backwardation, especially in different rate environments?

Interest rates are rarely the main driver of backwardation or contango. The reason for that is that it costs money to store oil. There is also an interest rate cost-of-carry; storing physical oil requires both facility fees and the tying up of capital.

As interest rates rise, the opportunity cost of that capital increases, further incentivizing a contango structure. However, interest rates remain just one of many factors, alongside supply levels and geopolitical risks, which ultimately dictate the curve’s shape.

How might the energy transition affect oil’s traditional market dynamics?

Oil producers often worry that higher oil prices could spark a renewed interest in the energy transition. With oil prices rising over the last couple of months, we have seen a renewed tendency on the part of consumers to buy electric vehicles and hybrids.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.