Motilal Oswal Mutual Fund has entered the contra fund category with an NFO in May, adding to a relatively under-populated segment that currently houses only three schemes: SBI Contra, Invesco India Contra and Kotak India EQ Contra Fund. The launch comes at a time when the category, though small, has quietly built a track record that merits closer scrutiny. The key question is whether these funds have consistently outperformed broader benchmarks over the long term, and how their stock-picking frameworks differ.

Contra funds invest in stocks or sectors that are currently out of favour and ignored by the market, betting on a turnaround in sentiment and business performance. In contrast, value funds focus on stocks trading below their intrinsic or fundamental value, irrespective of market popularity. While value investors may still buy popular companies if valuations are attractive, contra investors generally avoid crowded trades and prefer neglected opportunities linked to market inefficiencies.

The category’s limited size can be traced to SEBI’s 2017 classification norms, which required fund houses to offer either a value fund or a contra fund, but not both. Consequently, AMCs largely gravitated towards value strategies, leading to over 40 such schemes across active and passive categories. However, a regulatory shift in February 2026 now permits AMCs to operate both categories, subject to portfolio overlap remaining below 50 per cent.

Performance track record

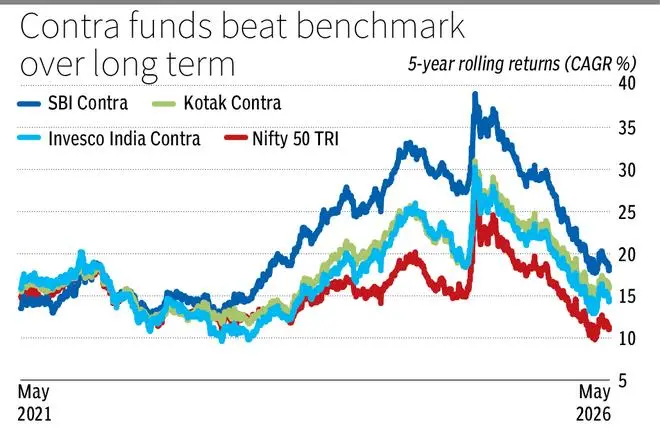

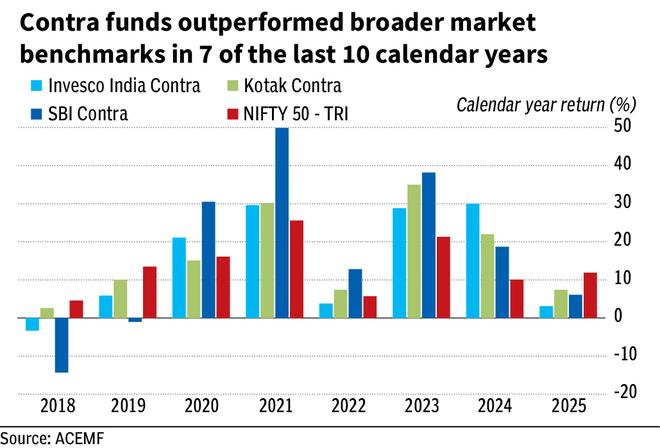

Despite its small universe, the contra category has delivered competitive returns. Over the last 10 years, five-year rolling returns averaged about 19 per cent CAGR, outperforming the Nifty 50 TRI (15 per cent) and Nifty 500 TRI (17 per cent). Flexi-cap funds, often considered a comparable diversified category, delivered around 16 per cent.

Within the segment, SBI Contra has been the standout performer, generating 22 per cent CAGR on this measure, followed by Kotak Contra and Invesco India Contra at 18 per cent and 17 per cent, respectively. On a three-year rolling basis too, contra funds maintained an edge, delivering about 18 per cent compared with 15 per cent for the Nifty 500 TRI.

Divergent frameworks

Each fund house deploys a distinct framework to identify contrarian opportunities.

SBI Contra adopts a three-bucket approach: turnaround, cyclical and value. Turnaround ideas focus on companies facing temporary operational or financial stress but with identifiable triggers such as management change or restructuring. The cyclical bucket tracks sectors nearing the bottom of their cycles, using indicators such as capacity utilisation and pricing power. The value segment targets overlooked businesses trading at significant discounts to long-term potential.

Kotak Contra builds a contrarian universe from its research coverage of over 550 stocks. Eligibility is based on five predefined filters: underperformance versus the NSE 500 index, trading below long-term average valuations, lower valuation multiples relative to sector peers, sectoral underperformance versus the benchmark, or trading below the 200-day moving average. From this universe, the fund applies its BMV framework (business, management and valuation) to identify fundamentally-strong companies with re-rating potential. The final portfolio usually consists of 50-60 stocks.

Invesco India Contra focuses on four categories of opportunities: companies in a turnaround phase, stocks trading below fundamental value, businesses benefiting from cyclical upturns and growth companies available at attractive valuations. It actively takes overweight and underweight sector calls against the benchmark based on valuation opportunities and sector rotation trends. The portfolio is mandated to maintain about 50-60 per cent exposure to value-oriented ideas.

The new Motilal Oswal Contra Fund plans to follow a “contra growth” strategy, differentiating itself from existing contra schemes that largely adopt a value-oriented approach while identifying contrarian opportunities. The fund aims to identify opportunities arising from sectoral dislocations, low investor interest, weak analyst coverage and valuation gaps relative to sector averages. The strategy categorises ideas into short-, medium- and long-term opportunities. It will primarily use the PEG (price/earnings-to-growth) framework targeting a portfolio PEG ratio of around 1.2 and focusing on companies with strong profit-growth visibility over the next two-three years. Key quality filters include operating cash flow-to-net worth, strong profit-to-cash-flow conversion and return ratios. The portfolio will remain concentrated with 25-30 high-conviction stocks and is unlikely to exceed 35 holdings.

Current opportunities

Across funds, current positioning reflects a mix of cyclical and structural calls.

SBI Contra has identified oil and gas as a contrarian opportunity, citing temporary earnings pressure linked to geopolitical developments. It also sees selective turnaround opportunities in pharma, while remaining cautious on IT from a sectoral perspective. Over the last three months, the fund has newly added UPL and significantly increased exposure to E.I.D. Parry (India), ICICI Bank and Prism Johnson.

Kotak Contra remains overweight on financials, citing valuations are below long-term averages even as credit growth and asset-quality trends improve. Healthcare is another preferred segment, particularly domestic pharma and hospital chains. Recent additions to the portfolio include Tata Steel, Indus Towers and Coal India.

Meanwhile, the fund manager of Motilal Oswal Contra sees short-term contrarian opportunities in auto, tyres and chemicals, where profitability has been temporarily impacted by elevated crude oil prices. The fund expects earnings recovery in these sectors once crude prices normalise over the coming quarters. Medium-term opportunities are being identified in banks, NBFCs and pharma. In financials, the fund expects greater clarity on asset quality and provisioning under the RBI’s expected credit loss (ECL) norms over the next two quarters, which could help differentiate stronger lenders from weaker peers. For long-term contrarian opportunities, the fund manager identified IT as a key structural play. While near-term disruption and revenue pressure may persist, the fund believes quality IT companies could emerge stronger over the next two-three years.

Investment takeaways

Contra investing is inherently timing-sensitive. Even well-founded ideas may remain out of favour for extended periods, leading to interim underperformance and testing investor patience. Another major risk is “value traps”, where beaten-down stocks fail to recover due to structural issues. Further, contra funds can lag during momentum-driven bull markets, as their portfolios are skewed towards under-owned or temporarily weak segments.

Not every stock in a contra fund portfolio necessarily represents a contrarian opportunity, as several holdings overlap with other diversified equity funds. While the initial stock selection is driven by contrarian ideas, portfolio exits are managed similarly to other actively-managed funds, based on factors such as weakening growth outlook, stretched valuations or deterioration in business fundamentals.

By targeting out-of-favour stocks, the contrarian approach takes time to deliver. Contra funds suit patient, risk-tolerant investors with an investment horizon of more than five years. They are suited as a satellite allocation within a diversified portfolio. All the three funds in the category managed to deliver better returns over long run. they could meaningfully enhance portfolio diversification and long-term return potential despite the occasional risk of value traps.

Published on May 16, 2026