Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

I thought I’d do something a little bit different today. I’m going to give my diagnosis of what I think is wrong with Japan and what – therefore – needs to be done to lift the country out of its current debt trap. I’ll then contrast my views with those of two good friends: Brad Setser from the Council on Foreign Relations in NY and Joe Gagnon from the Peterson Institute in DC. The big picture on Japan is complex and there’s plenty of room for reasonable people to disagree. So I’m contrasting their views – I apologize in advance for anything I screw up – mainly to highlight where I see things differently, which I think is quite instructive for debating Japan and what needs to happen.

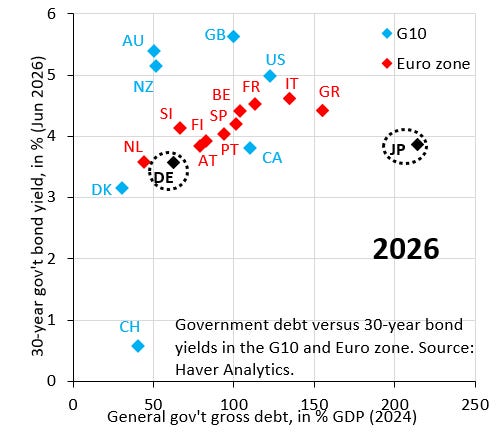

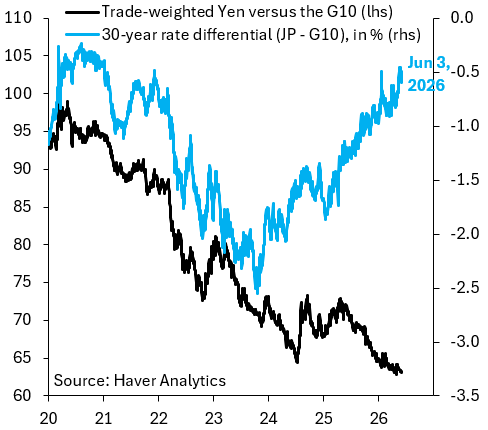

Let me start by outlining my position. In my opinion, Japan’s basic problem is that its long-term government bond yields are being kept artificially low by ongoing – and big – purchases of government bonds by the Bank of Japan (BoJ). The chart above shows how big this distortion is. Gross public debt is 240 percent of GDP, almost four times as high as Germany, but the 30-year government bond yield for Japan is basically the same as Germany. This means a fiscal risk premium, which would show up if the BoJ stopped buying government bonds, is being artificially suppressed, which is what’s putting depreciation pressure on the Yen. The BoJ is aware of this, which is why it’s reducing the pace of its bond buying in an attempt to let yields rise. But – because it’s likely that “true” yields are substantially above current yields – the BoJ has to do this very slowly and carefully, which – as the chart below shows – is what’s giving us the counterintuitive pattern whereby the 30-year yield differential of Japan versus its G10 peers is rising, which should lift the Yen, but the Yen is falling. That’s a signal – in my view – that observed yields are far below where markets would set them without BoJ interference. What would be a bond market crisis without the BoJ has morphed into a currency crisis. One way or another, Japan’s debt overhang is making itself felt.

What Japan needs to do to get out of this debt trap is have the government sell some of the financial assets it holds to pay down public debt. These holdings are huge and are the reason net debt is only 130 percent of GDP. That’s still high, but it’s a heck of a lot lower than 240 percent of GDP. This is where Brad’s views come in. Because net debt is so much lower than gross debt, my sense is that he doesn’t think there’s a debt problem. Therefore, it’s perfectly reasonable for Japan to use its official FX reserves to periodically intervene to stop the Yen from falling. Brad like to point out that Japan is doing these interventions at a profit, because it’s selling Dollars it bought when the Yen was much stronger. I disagree on two front. First, Japan isn’t a hedge fund. The objective isn’t to make profitable FX interventions. The goal is to sustainably stabilize the Yen. Only debt reduction can do that. Second, while it’s true that net debt is a lot lower than gross debt, this hardly matters if the government isn’t willing to mobilize these resources to pay down gross debt. The signal we’re getting so far – a signal that grows with every round of FX intervention – is that Japan isn’t ready yet to do that. If that’s true, only gross debt matters and net debt – at this point – is academic.

This brings me to Joe’s argument. Joe says that – by selling its FX reserves – Japan is doing exactly what I’m advocating, i.e. it’s selling its financial assets – in this case its holdings of US Treasuries – and presumably using the Yen it buys to pay down debt. While that’s true, in my opinion the signal’s all wrong. The signal Japan needs to send is that it recognizes debt is a problem. It can do that with a wave of privatizations and sales of domestic assets. In my view, markets would reward that with a stronger Yen and lower yields, i.e. exactly what Japan needs. FX interventions signal exactly the opposite. They signal denial, with the government papering over the symptoms of the debt overhang with FX intervention instead of confronting the problem. The market punishes this denial with continued depreciation pressure on the Yen. The signal is the wrong one because Japan has yet to reach “acceptance.”

So my disagreement with Brad and Joe is on the underlying root cause of what’s going on and – therefore – what needs to be done to fix things. It’s true that intervention has worked to cap $/JPY at 160, but the half-life of intervention is falling rapidly. In my opinion, Japan risks ending up in a place where intervention no longer stabilizes the Yen, which is when the real nightmare starts. Better to avoid that.