The name is misleading because people with ADHD don’t necessarily have a deficit of attention, but rather, the inability to focus their attention.

ADHD coach Brett Thornhill says, “It’s like your brain keeps switching between 30 different channels and somebody else has the remote.”

The stereotypical view of someone with ADHD is a hyperactive boy who can’t pay attention in class, has seemingly endless energy, and is constantly moving, fidgeting, and talking. But ADHD is also the person with their head in the clouds, the daydreamer. They are easily distracted and have problems sustaining their attention. With ADHD you can present more hyperactive symptoms, more inattentive symptoms, or have a balance of both. In addition to these types, ADHD exists on a spectrum and can impact people in different ways, to varying degrees. All three types interfere with the individual’s functioning in multiple settings. ADHD is very real, very challenging, and can often be debilitating.

I have the combined type of ADHD, so I experience both hyperactive and inattentive symptoms without one of those being far more prevalent. While I did well in school, almost every report card mentioned that I was a chatterbox. When I wasn’t busy talking, I was staring out the window, doodling, or working on homework for another class. None of these behaviours was flagged as a problem because of my grades. This is often what happens to women and girls with inattentive ADHD.

Since my moment of free-falling, I have found solid ground. I’ve built a successful business, transformed my financial situation, and found myself in the happiest, healthiest relationship I’ve ever had. It turns out the problem was never me, or my undiagnosed ADHD, but the fact that society is not designed to accommodate anyone who diverges from the norm. Of course, I would be remiss if I didn’t point out that my privilege greatly contributed to this outcome as well.

In this chapter, we are going to touch on some of the common challenging aspects of managing money with ADHD, and how you can work with your brain instead of against it. I want to acknowledge that there is a lot of research currently being done on ADHD, especially in women, so some of this information might change as new discoveries are made. It’s important to note that everyone experiences their ADHD differently, and some of the money struggles I talk about won’t be applicable to you. Whether you’re reading this chapter for yourself, or to support someone else in your life with ADHD, give yourself the space and grace to experiment and find what works.

How ADHD impacts your money

I opened up a $10,000 line of credit when I was in college to help cover some of my expenses as a student. I remember thinking to myself I’ll only use like $1,000 and pay it off once I’m back at my full-time summer job. But it only took me two months to max out that $10,000 line of credit because I couldn’t stop impulse spending.

Yes, I know, I’m wondering how that was possible too. Prior to my diagnosis, my brain was feeling so out of it most of the time that I would spend money just to feel something. This line of credit was the gateway to even more spending, and before I knew it I had a maxed-out credit card, two lines of credit, and my student loans.

This is how I ended up in $35,000 of debt, $15,000 of which was high interest. I would look at my credit card statement and not even remember half the purchases I made. It seemed like everyone around me had it all figured out, and here I was, free-falling.

The shame I felt followed me everywhere: when I went out for dinner with my friends, paid for my groceries, treated myself to a Starbucks, or bought another shirt that I definitely did not need. I felt so out of control, but at the same time I didn’t know how to change my money habits and behaviours.

Turns out, my struggle with impulse spending and debt was not a unique one. 65% of folks with ADHD say that having ADHD makes managing their money more difficult.

But that’s not all.

If you have ADHD you are…

- 2x more likely to suffer from anxiety linked to finances

- 3x more likely to struggle with debt

- 3x more likely to miss bill payments either occasionally or often

- 3x more likely to struggle with sticking to a budget

- 4x more likely to impulse spend

…than those who don’t have ADHD.

ADHD isn’t confined to one area of your brain or one major impact on your life. It affects how you take in sensory information, how you think and process, and how you respond and behave. When it comes to your finances, it’s going to impact how you understand, spend, and manage money. It will influence your emotions and mood, which we know both play a big role in financial decisions. Our challenges can lead to earning less and paying more than folks without ADHD. Just like every other chapter in this book, understanding how this piece of your identity impacts your money story, behaviors, and patterns is crucial for changing your situation.

When I was first diagnosed and started to learn more about how certain traits affected my money, I looked online to learn more. I was met with tumbleweeds, a couple YouTube videos and vague articles, but nothing that I could relate to. In fact, many of the articles giving advice on ADHD and money were filled with tips like “just make a budget” or “stop impulse spending.”

Thank you, Janet, I never thought of that!!

Much of the advice available completely misses the mark because it suggests using systems and tools designed for and by neurotypical folks instead of actually catering to neurodivergent brains. For those of you unfamiliar with those terms, “neurodivergent” refers to those whose brain and cognition differs from what is considered “typical” by society. This can include folks who have ADHD, autism, dyscalculia, dyslexia, dyspraxia, BPD, and more. The term “neurotypical” describes those who display “typical” cognitive function. Please be aware that this language is always evolving, and new terms might be in use by the time you read this book.

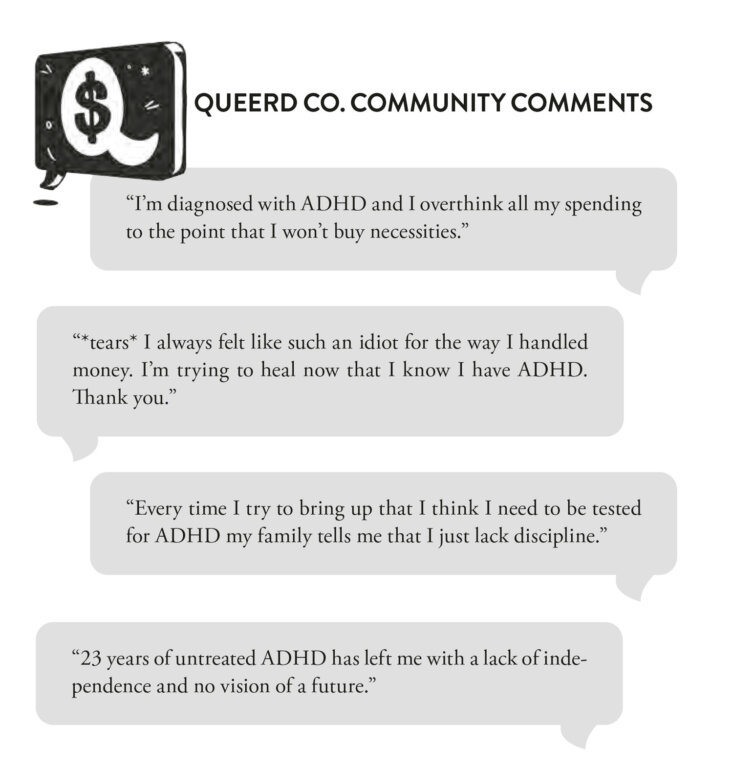

To fill the gap I had identified, I started creating content around how my ADHD impacts my finances. If you follow me on social media, you know I talk about ADHD and mental health on an almost daily basis. I’ve had multiple videos on ADHD and money go viral, and here are some of the comments I have received:

I hope after reading these comments, you know that you’re not alone. I hope you feel validated, that it’s not just you struggling with your money. I hope you know that your financial challenges are clearly not your fault. I’ve said that a lot throughout this book, but I will say it a million more times in an attempt to override society’s overarching message that your struggles are solely your problem.