As I’ve written about before, one of CPS’s big challenges is its debt service. As of June 30th 2025, CPS had roughly $9.1 billion in outstanding long-term debt, and service on that debt took up around 9.8% of last year’s budget. That’s a lot. CPS’s debt is also relatively expensive for a municipality: the district is currently non-investment grade (or ‘junk rated’) by all three major bond ratings agencies. That translates directly into a higher borrowing cost for the district when they need to issue new debt.

Given that, it sure seems like CPS should be thinking very deeply about ways to reduce our borrowing costs and get the district on firmer footing. Today I’d like to propose one somewhat quirky way to do that, by taking a page out of the city’s book with some clever financial engineering.

First, some background: while most of Chicago’s bond issuances are rated BBB (for now), the city also issues some bonds out of a structure called the Sales Tax Securitization Corporation, or STSC, which are rated AAA with Fitch and Kroll (and A+ with S&P). That rating difference is a big deal, with the interest rate on past issuances coming in over 100bps (1 percentage point) lower than the city’s general obligation bonds – that’s worth something like $60 million per year in annual debt service.

The Sales Tax Securitization Corp’s bonds are higher rated than the city’s general obligation bonds because of its unique structure which protects bondholders. Here’s how it works:

-

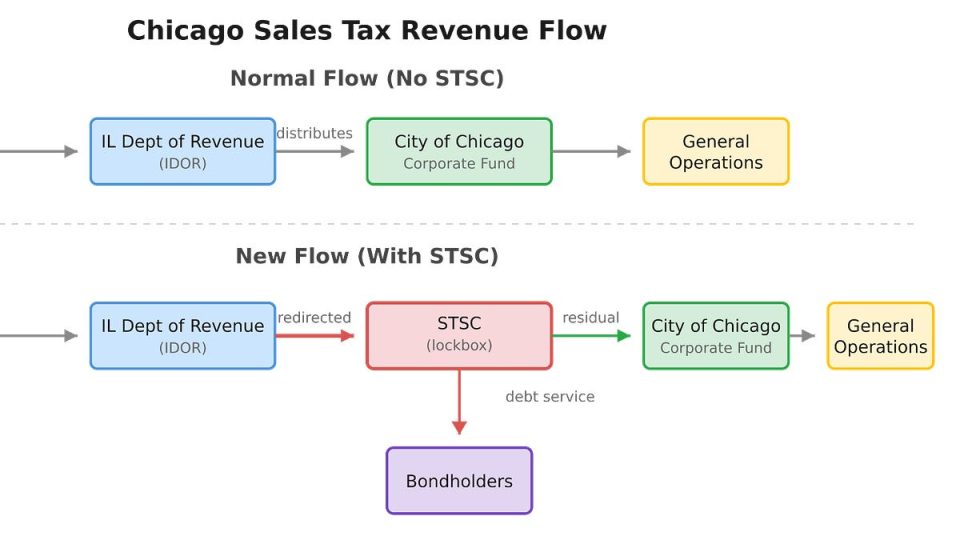

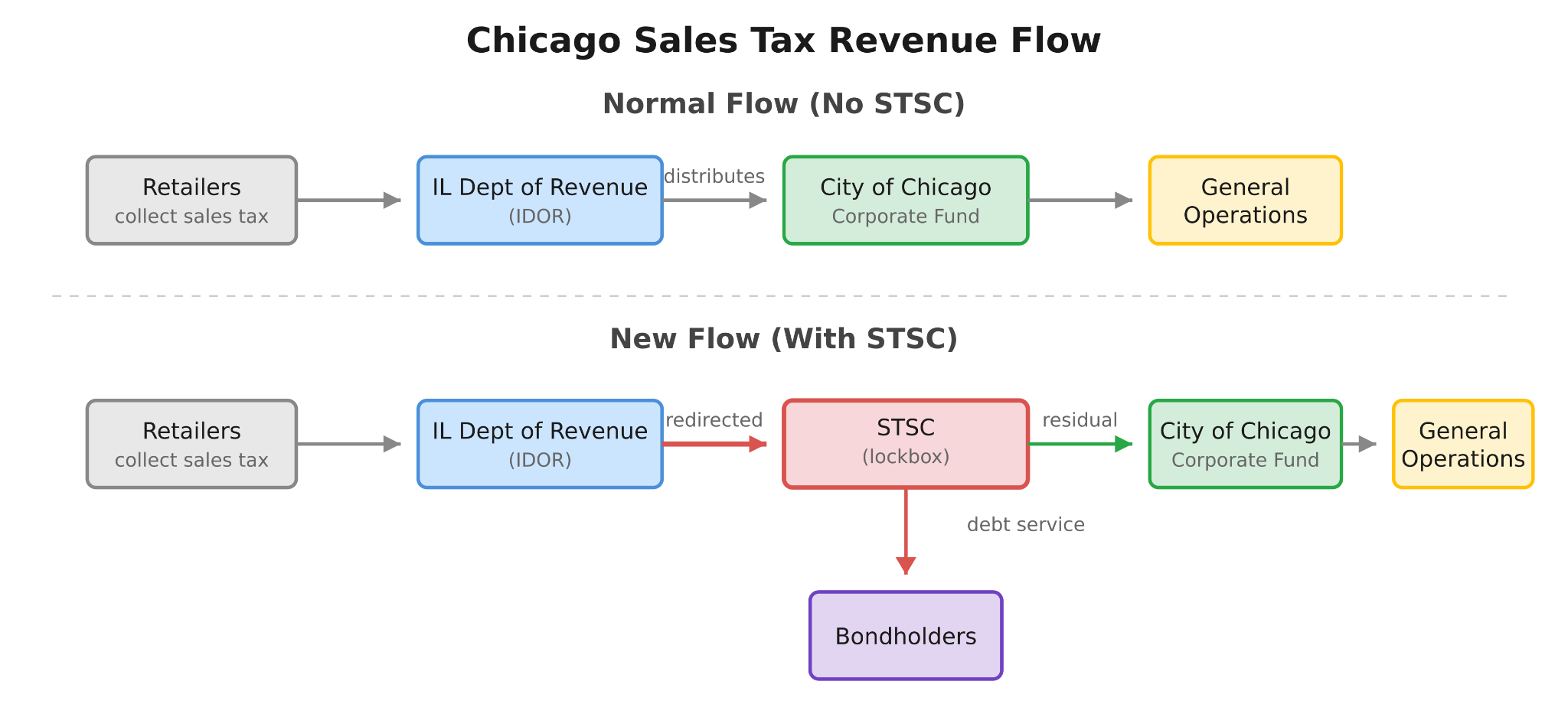

Sales tax revenues are collected by the State of Illinois, but the City of Chicago is entitled to a share of those revenues. Normally the State would just send the revenue to the City.

-

Instead of doing that, the State instead sends the revenue to the STSC. The STSC then uses that revenue to pay debt service on any bonds it’s issued. After it does so, any remaining revenues are then passed onto the city.

If you sketch it out, it looks something like this:

That might not sound like a big deal – “a middleman takes state revenue, pays bondholders, then passes it on to the city” – but by creating a legally distinct entity that pays the bondholders *prior to the city getting those revenues,* you’ve made the bondholders safer. They no longer need to worry about whether Chicago might default on that debt, since their credit risk is just to the Illinois Department of Revenue, not to the City. Because bondholders are safer, they demand a lower interest rate in compensation for their money, and the city’s finances benefit. It seems like magic, but it’s just financial engineering.

Focusing strictly on the financial/source of revenue side, it seems like some structure like this ought to be a strategy for Chicago Public Schools to consider.

For starters, a lot of CPS’s revenue comes from the state. Most obviously, they get around $1.8 billion in Evidence-Based Funding (EBF) dollars. They also receive about $250 million in Personal Property Replacement Tax (PPRT) revenue, which – like sales tax revenue – is collected by the state but remitted to local governments.

Moreover, these sources are already pledged to back some of CPS’s debt issuances (referred to as ‘Alternate Revenue Bonds’). In the case of PPRT dollars, it’s even already the case that the revenue flows from the state to a trustee to benefit bondholders. Setting up a separate entity to receive revenues from the state and pay bondholders before sending the remaining revenue onto CPS doesn’t fundamentally change things; it just takes things one step further and gives those bondholders a more steadfast guarantee than the revenue pledge they’re already getting. And my back-of-the-envelope math indicates that the revenue sources are likely large enough to refinance all of the outstanding Alternate Revenue Bonds debt into new securitized bonds which would be rated higher while generating significant savings (maybe as much as $100 million per year).

But I don’t want to sound naive about how easy this would be. For starters, most municipal bonds aren’t callable immediately; many have protections ensuring they remain outstanding for 5 or 10 years at least. That curtails our ability to redeem some of these securities into a better structure for the district.

And unless we do refinance everything in one wave, we’ll need to ensure that a new structure like this doesn’t violate any covenants on the remaining securities, so existing bondholders don’t have legal standing to come after the district for impacting their pledged revenue sources. My read of the latest EBF-backed Bond Placement Offering documents on CPS’s website is that this is likely doable, but difficult, and will require some creativity which I’m here going to relegate here to a particularly important footnote.

Secondly, the state statute that enables the STSC (65 ILCS 5/8-13-5) only permits home rule municipalities – like the City of Chicago – to create issuing corporations and divert revenues from the State. Chicago Public Schools is not a home rule entity, so Springfield would need to amend this to permit them to do something similar for anything like this to work.

Writing this from Chicago, I also feel compelled to point out the ways in which this is not a truly free lunch. In many ways, securitization is a neat magic trick; you just change the way money moves around and somehow your financing gets cheaper.

But CPS isn’t truly giving up nothing here. For one, they’re basically giving up the freedom to default on their bondholders. I think that’s a perfectly good trade – I think it would be very, very bad for CPS to default on their bondholders in the first place – but it is a tradeoff. Second, in theory this means that the risk associated with any non-securitized CPS debt gets higher. Less revenue is available to pay those non-securitized bondholders, since the securitized ones got paid back first. The interest rate on those non-securitized debts should go up accordingly. But that’s not necessarily a bug. It can be useful to have a capital stack that doesn’t just consist of one interest rate; that lets you prioritize which debts to refinance or pay down first. Phrased differently, CPS would be better off to have $5 billion in debt with a 3% interest rate and $5 billion in debt with a 7% interest rate than to have $10 billion at 5% interest rate. In the first scenario, they can lower their cost of capital by prioritizing 7% repayment; in the latter they can’t.

I am very very cognizant that much of the above is probably an oversimplification of CPS’s debt management situation. Moreover, any securitization structure is obviously not a panacea, and it wouldn’t solve CPS’s budget problems.

But even with all of that said, securitization can help make the debt management math a bit easier than it otherwise will be, and it’s worth looking into. We need to get creative in figuring out how to solve our public finance issues, and this is a good place to start. I’d encourage anyone at CPS to explore whether a structure like this makes sense to attempt anytime soon (and, if anyone reading this happens to be a municipal finance expert – please reach out! I would love to hear from you on this or any other ideas for solving our myriad of financial issues).