SUMMARY

- “Yield Matters” but investors cannot ignore real yields.

- Real yields are attractive near 2% despite rising inflation, in our opinion.

- Credit spreads are tight, but defaults are low.

Above Average Real Yields with Strong Fundamentals

Thus far 2026 has been a roller coaster year for fixed income markets. The 10-year Treasury, the benchmark rate for the bond market, saw its yield trade as low as 3.94% and as high as 4.43%. Currently, the benchmark is trading at 4.37%. While investors may not have enjoyed the volatility, the backup in nominal yields has gotten our attention. Our current fair value for the 10-year Treasury is 4.30% and would view rates above 4.50% as buying opportunities. The move higher in yields has been driven by worries surrounding the growing budget deficit of the US government and fears of inflation remaining elevated due to war-related energy supply constraints.

In this fixed income update we will explore real yields, credit spreads, and our outlook for the various sectors of the bond market for the remainder of the year.

Content continues below advertisement

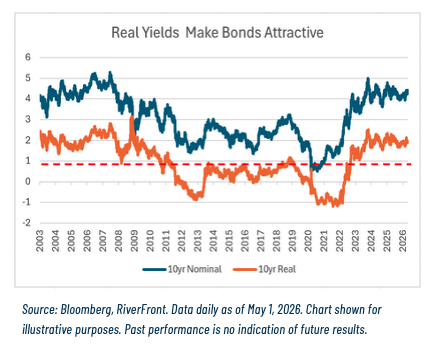

Real Yields Approaching 2%, Appear Attractive Again

Most investors focus on nominal yields when purchasing bonds because, as we have reiterated over the years, “yield matters.” Typically, the starting yield of a bond is the return that the investor will receive if they hold the bond to maturity. While the nominal yield is important, the ‘real’ yield (nominal yield minus implied inflation) is crucial as it calculates the true increase in purchasing power of the investment. Chart 1 above compares nominal yields and real yields back several years prior to the Great Financial Crisis (GFC) in 2008.

While real yields have averaged nearly 1% over the last 23 years, (the dotted red line in the chart), it has been a story of 3 regimes. From 2003 to 2010, and now in the post COVID world the average has been around 2%. By contrast, to prevent deflation after the GFC, the Federal Reserve ensured that both short- and long-term interest rates were below the rate of inflation, making bonds unattractive in our opinion. With real yields back around 2%, we see opportunities. Hence, bonds are attractive again in our opinion.

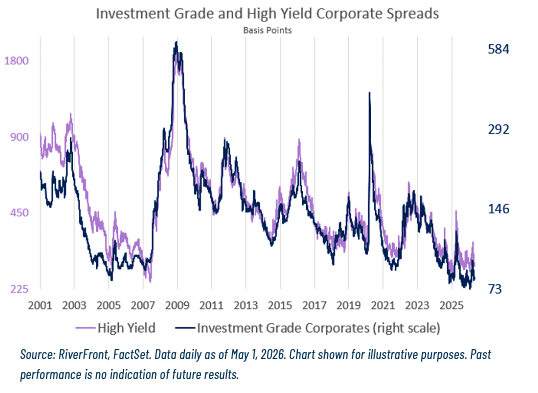

Credit Spreads Likely to Stay Tight, Due to Strong Corporate Earnings

While we view real yields as an important indicator of the attractiveness of bond valuations, we also view credit spreads (the risk premium paid to own corporate bonds rather than Treasuries) as an important input. When credit spreads are ‘tight’ compared to Treasuries (meaning investors require a smaller risk premium than normal to own bonds), this indicates that investors are confident that companies can meet their debt obligations. When credit spreads are ‘wide’ versus Treasuries, this suggests less confidence in their creditworthiness. Currently, credit spreads both in investment grade corporates (bonds rated BBB or higher) and high yield corporate bonds (rated BB or lower) are trading exceptionally ‘tight’, near their all-time lows as shown in Chart 2, above. High yield and investment grade risk premiums are 2.77% and 0.81% respectively above comparable maturing Treasuries. High yield credit represented by the left axis and investment grade risk by the right axis in Chart 2. Strong corporate balance sheets have kept investors’ appetites for bonds robust, leading to solid availability of credit. We believe that credit spreads will remain in a tight range for the remainder of the year, barring a global macroeconomic event, as corporate earnings in the US remain strong.

Conclusion:

We expect the bond market yields to face upward pressure the remainder of 2026, as the fallout from the Iran war will keep oil and gas prices elevated for an extended period. The combination of elevated oil and gas prices will put upward pressure on inflation via higher transportation costs passed along the supply chain into finished goods prices. Higher inflation will bring worries of stagflation to the forefront, causing bond yields to rise further, in our opinion. However, we believe that there is a ceiling on how high yields can go because higher inflation will slow the economy down and cause Fed officials to lower interest rates. Hence, we believe upside resistance for the 10-year Treasury in a stagflation scenario is around 5%…a level that would likely trigger significant demand from yield-seeking investors and slow economic activity enough to be self-correcting. Given a Kevin Warsh-led Fed will likely have a bias towards cutting rates, we do not believe the central bank will wait for yields to move that high. We view the oil and gas inflationary impulse as temporary and thus seek to take advantage of opportunities if yields move meaningfully higher than current levels.

The bottom line: bonds are offering real value again, in our view — something investors haven’t been able to say for much of the past fifteen years. With our balanced portfolios currently underweight fixed income, any further backup in yields driven by transitory inflationary pressures would represent an opportunity to add exposure at even more attractive levels.

Authored by Kevin Nicholson, CFA

Originally posted on RiverFont Investment Group

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.