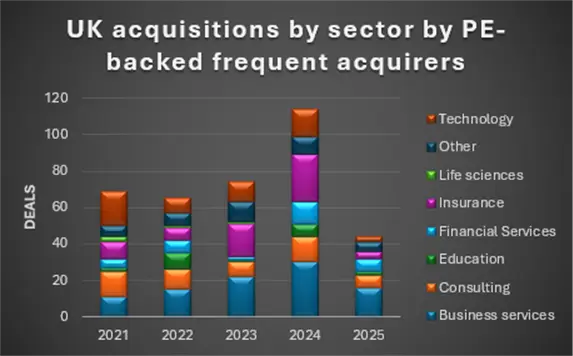

Mid-market bolt-on acquisitions by UK private equity and venture capital-backed platform companies fell 61% in 2025, according to research from Stevens & Bolton. Deal volumes dropped to 44 from 114 in 2024.

The analysis covered bolt-on deals completed since the start of 2021 by 45 of the UK’s most active serial acquirers, defined as platforms that have made 10 or more acquisitions over the past five years.

The figures mark a sharp reversal after a five-year high in 2024, when buy-and-build activity surged across the mid-market. Even with the overall decline, some areas remained more active than others, particularly business services, consulting and financial services.

Of the 44 deals completed in 2025, 36% were in business services, while consulting and financial services each accounted for 16%. Business services was already a major source of transactions over the full period studied, making up a quarter of all deals since 2021.

Technology saw one of the steepest pullbacks, with transactions down 80% in 2025. The decline came as investor attention increasingly shifted toward artificial intelligence.

Other sectors also recorded sharp falls. Insurance, which had previously attracted sustained interest, was down 85%, while education fell 71%.

Sector shift

The research suggests buyers spent more time integrating businesses acquired during the previous year’s rush of transactions. That is common in buy-and-build models, where a platform business acquires a series of similar or complementary companies before pursuing further expansion or an eventual exit.

The data also points to wider economic and political uncertainty as a factor in the slowdown. Geopolitical tensions, economic policy developments and changes in government at home and abroad were cited as likely contributors to weaker activity.

Joe Bedford, Head of Corporate at Stevens & Bolton, said: “The fall in bolt-on activity last year was sharp but doesn’t suggest that private equity or venture capital has fallen out of love with buy and build, which will still remain a naturally favoured strategy and significant driver of UK M&A activity.”

“M&A activity tends to act as a bellwether for economic confidence, which underpins stability and the alignment of buyer and seller price expectations, and therefore the ability to get more deals done more quickly. As a result, it is no surprise that 2025 saw a slowdown in buy-and-build activity. The impact of Reeves’ first Autumn Budget in October 2024, coupled with the crashing waves of Trump 2.0 and the resulting uncertainty, inevitably had a dampening effect on transactional activity. Conversely, the impending threat of that same Budget and anticipated Trump-led uncertainty had supercharged bolt-ons and M&A generally in Q1 to Q3 of 2024.”

“Experience would ordinarily dictate that 2025 was the calm before the brewing storm. As confidence picks up, pent-up M&A activity tends to be released and new deal volume rebuilds momentum. Private equity firms will always seek EBITDA scalability opportunities and consequential multiple arbitrage, and the data shows that there are plenty of sectors with strong and growing buy-and-build potential. If confidence, or opportunism and increased appetite for risk, can pull the market through the environment of global unrest, then 2026 bolt-on activity should at least return to pre-2024 levels and, because of a quieter 2025, could exceed that.”

AI focus

Jonathan Steele, Corporate Partner at Stevens & Bolton, said the technology figures may reflect a shift in capital allocation rather than a retreat from the sector altogether.

“Of course, macro-economic headwinds have had an effect on dealmaking, but aggressive acquisition strategies can be seen in a number of sectors, including business services, financial services and consulting.”

“Trends in technology deal activity might suggest that investor and acquirer attention has been focused on artificial intelligence, so it would not be a huge surprise to see a dip in buy-and-build transactions for existing technology companies. The AI bubble is dominating the market and, inevitably, PE is focused on tactical and strategic long-term investment in future technologies.”

“PE and VC were full throttle through much of 2024, so it is inevitable that they will need to invest time into integrating acquisitions. This means that we could be in for a period of consolidation ahead of a potential surge in exit activity. Despite the short-term dip in activity, the signs are there that PE, and buy and build with it, have dry powder to deploy and are set for a strong 2026, current global and geopolitical uncertainty allowing.”

The findings are based on data from Inven, a private deals database, and represent a screened cohort of active UK mid-market consolidators rather than the whole private equity market. Within that group, the numbers show that while overall buy-and-build activity retreated sharply after an exceptionally busy year, business services, consulting and financial services were the most resilient parts of the market.