Credit markets are navigating one of their most challenging environments in years, with default rates climbing across both public and private debt. The consequences could extend beyond individual borrowers as a result of the relationships between lenders, investors, insurers, and the broader financial system.

Fitch Ratings reported in May 2026 that the US private credit default rate reached a record 6% in April, while private-credit-backed corporate borrowers recorded a 9.2% default rate during 2025.

Stress indicators are flashing across multiple gauges. Proskauer’s Private Credit Default Index, which tracks 697 loans totalling $189.2 billion in US markets, reported a 2.73% default rate in the first quarter of 2026, up from 1.84% two quarters earlier.

Stephen Boyko, partner and co-founder of Proskauer’s Private Credit Group. said “While there are signs of pressure in certain segments, overall levels remain relatively contained and continue to track below those in the broadly syndicated loan market.”

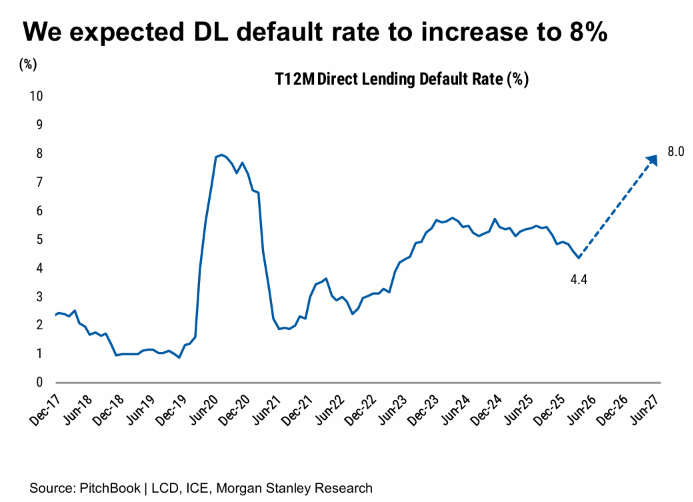

Morgan Stanley has reported leveraged finance will grow in size, with US high yield issuance increasing to US$440 billion, up 34% year on year, reflecting the growth in AI financing, but equally a software-led increase in loan and private credit default rates will rise to 5.5% and 8%, respectively, while HY may moderate to 3.5%. Private credit now makes up 30% of leveraged debt from 13% ten years ago.

Morningstar DBRS noted in March that a 78% year-over-year increase in default events in 2025 and expects the accelerated pace to continue into 2026, with a high proportion of borrowers currently rated in the CCC-through-C categories likely to weaken further.

A notable feature of this default cycle is the prevalence of so-called distressed exchanges, which are restructurings of debt arrangements that technically avoid hard payment defaults. Distressed exchange transactions now dominate default activity, accounting for 94% of downgrades to default or selective default during the 12 months ending February 2026.

David Hamilton, head of asset management research, at Moody’s estimates that debt exchanges, maturity extensions, and other distressed restructurings accounted for roughly 65% of private credit defaults during 2025. Critics argue these mechanisms simply kick problems down the road rather than resolving them.

Risks remain concentrated in highly leveraged, rate-sensitive debt, particularly among software companies and smaller borrowers, as AI disruption compounds structural pressures. Higher central bank rates are making it harder for companies to refinance, compounding existing credit weakness.

US banks had lent nearly $300 billion to private credit providers by mid-2025, according to Moody’s, meaning any contagion could ripple across markets if stress intensifies. Insurers face particular exposure. Rising impairments can reduce investment income, while downgrades can increase funding costs and place pressure on capital requirements, with delayed cash flows creating asset-liability matching challenges.

While Morgan Stanley notes that redemption pressures might persist within business development companies (BDCs) if retail sentiment remains weak, redemption limits could prevent ‘forced selling’ pressures.

The bank expects to see a shift to direct corporate loans, infrastructure private credit, real estate debt and asset-based finance (ABF) in a move it dubs “Private Credit 2.0”.

©Markets Media Europe 2025