U N I C U S R E S E A R C H

Staying ahead of the curve

Most research firms read the same filings at the same time and reach the same conclusions a bit too late. We have already established that we conduct deep-dive, investigative fieldwork for most of our short recommendations. Our edge is timing and thorough due diligence. We are trying to find stress signals before they are covered by the mainstream media.

A lot of that comes from working across borders. Defaults, redemption gates, fund freezes, and forced sales tend to get reported as isolated events, one fund or one country at a time. The UK and Europe disclose more and disclose it sooner than the US. Their regulators operate more tightly and are more risk-averse, so warning signs appear in European filings before the equivalent US data is available. We take those methods, adapt them for US reporting, and run them here. It lets us see a developing problem on this side of the pond while it is still forming, and act on it before the market does. That is why we have analysts in the UK and Europe.

Right now, most of that effort is pointed at private credit.

The reason is simple. The money behind these funds comes from banks, private equity, insurers, and pension funds. If the businesses, ABS, BNPL, and CLOs inside the funds start to deteriorate, the damage does not stay there. It runs back up into the returns of the institutions that funded them. Thoma Bravo stepping back from Medallia is the kind of early signal we watch for. Along with Bain Capital’s European CLO Tranche Default, the first default of its kind in the post 2008 CLO 2.0 market in Europe. And the institutions most exposed are the ones that cannot leave. A pension fund or an insurer cannot redeem the way a retail holder can, and even retail is finding the exits crowded.

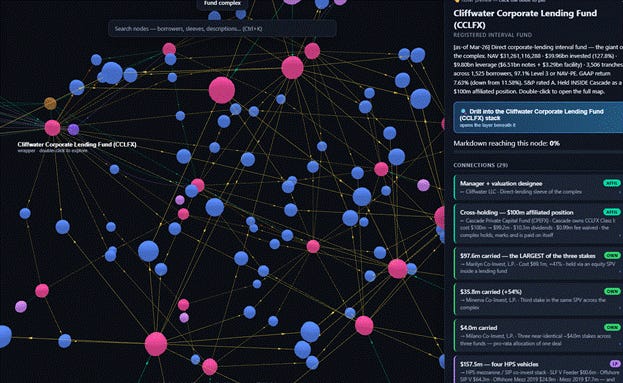

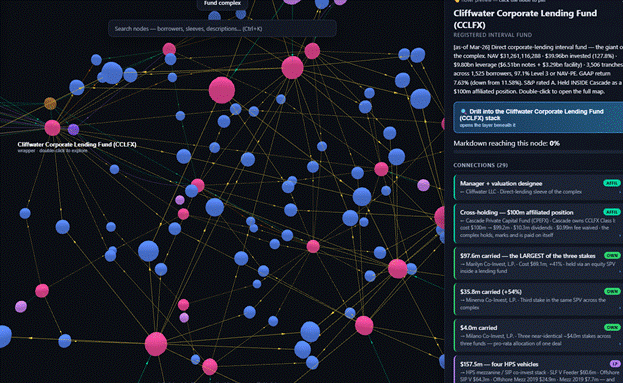

Our newest deep dive is on the Cliffwater Corporate Lending Fund, one of the largest interval funds in private credit.

The short version: In a recent quarter, investors requested to withdraw about 17% of the fund, against a 5% redemption cap. The requests came in roughly 3.4 times oversubscribed, and holders got back about a third of what they asked for. That is what sent us into the actual loan book.

Two-thirds of it are direct loans, concentrated in software and health care. But about 40% of net assets, roughly $12.5 billion, is not loans to operating companies at all. It claims on other lending vehicles: CLOs, BDCs, and stakes in funds run by other managers. A large part of what CCLFX does is lend to other lenders.

That is the part that matters to us, our investors and clients. It is the hardest piece of the book to sell, and it sits there in the exact quarter the fund needs cash. Selling it does not contain the stress; it pushes it out into the rest of the system. The individual credits look fine. The fragility is in the structure and the liquidity, which is usually where it lives.

We are doing this one fund at a time, reading the loans rather than the pitch, and tracking how the vehicles connect to each other. Stone Ridge first, then HLEND, now CCLFX. The team is into Apollo’s redemption loan books next. The goal each time is to see how stress would reach the equity side before it actually does, and to come out the other end with a concrete short idea, backed by deteriorating fundamentals and a full deep dive. Our engineering data team tremendously helps us with this.

The question we keep circling back to is what happens to the equity of these institutions when they realize they are stuck and not sitting where they thought they were.

So, we are building a map. It is an interactive view of the private credit fund complex, weighted toward non-traded BDCs and interval funds. For each fund, we parse the entire schedule of investments down to the individual borrower, then check those holdings against the balance sheet. We cross-reference borrowers across funds to see every place the same company appears within the complex. On top of that, we model how stress moves through the structure.

This is not a static holdings list. It is a way to watch concentration and redemption pressure build across the whole system at once, and then trace any single name back to the company-level problem driving it.

The point is the interlinked chain. Say a bank lends to an Apollo private credit vehicle, and that vehicle lends to a borrower like MFS. When MFS fails, the loss does not stop at the fund. It lands back on the bank as a second-order hit, and on the fund’s pensions and insurers as a third. Most of the market sees the first failure. We are working to map the second and third before they arrive.

There is currently a major focus on quantitative research, but our work here addresses a gap that lies before the numbers. The need to map and track opaque markets qualitatively, specifically across private credit, BNPL, and ABS. In these markets, the most important signals often appear first in the network of relationships, incentives, legal structures, funding channels, collateral flows, and risk transfers before they appear in clean, measurable data. This is why we are building a mapping and tracking framework: to identify where risk is moving, disguised, delayed, and concentrated beneath the surface.

The value-add is that this framework helps us bridge the gap between fundamental research and market-pricing intelligence. Traditional quantitative models are powerful when clean, frequent, and comparable data exists, but opaque markets often suffer from delayed disclosures, inconsistent reporting, manager discretion, model-based valuations, and legal structuring that changes the economic meaning of the data. Our approach aims to turn qualitative market intelligence into structured, repeatable datasets, enabling us to build time series, risk maps, entity-level exposure networks, valuation overlays, and early warning indicators that can sit alongside quantitative models rather than in isolation.

For now, this is available only for our clients. If you are interested in becoming our client, email us: laks@unicusresearch.com .