turk_stock_photographer

There are some stocks that income investors can buy and hold without having too much worry over the long run. To qualify, these stocks should have a strong track record of shareholder returns and durable revenue streams that can stand the test of time.

While many companies get filtered out by this simple criterium, the ones that do make it exemplify the survival of the fittest, and can be great ‘set it and forget it’ type holdings that don’t take up too much of an investor’s time. Time is a most precious and yet sometimes underrated resource, and there is plenty of value in not losing sleep over one’s holdings.

This brings me to Agree Realty (NYSE:ADC), which I last covered in December last year, highlighting its strong performance amidst high interest rates. It appears the market has agreed with my thesis. That, and the potential of an interest rate cut in September, have sent stock rising by 17%.

ADC has also given investors a 21% total return including dividends, surpassing the 17% rise in the S&P 500 (SPY) over the same timeframe. In this article, I revisit the stock and discuss whether it and its preferred stock remain buys in the current market, so let’s get started!

ADC: Common Or Preferred? One Is The Better Buy

Agree Realty is a sizable net lease REIT that focuses on recession resistant retail and service-oriented tenants. It has a $7 billion equity market cap that comprises 2,202 properties.

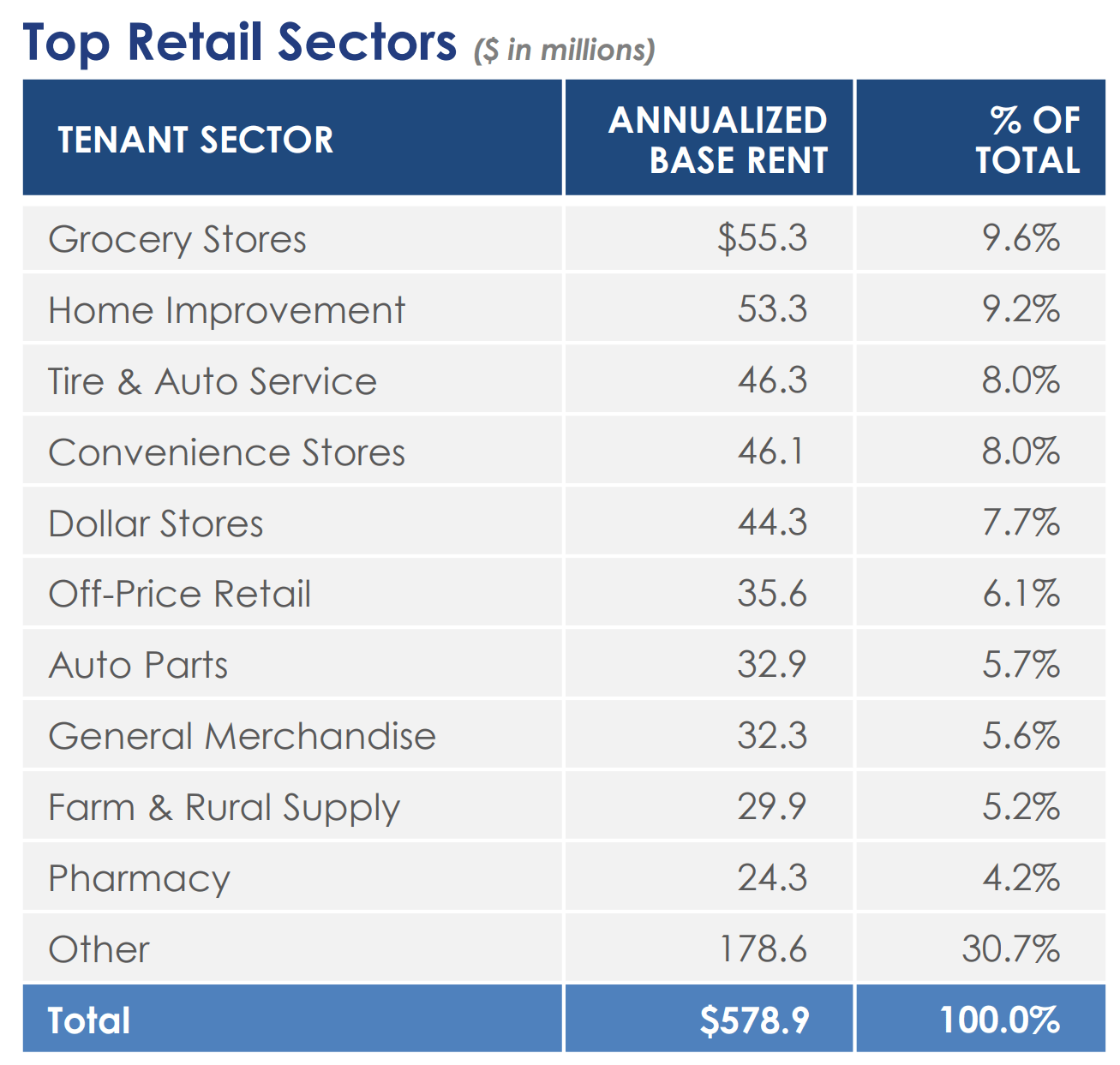

Its top 10 tenants include Walmart (WMT), Tractor Supply (TSCO), Dollar Tree (DLTR), TJX Companies (TJX), and Kroger (KR). As shown below, ADC focuses on necessity-based tenants and concepts such as convenience stores, home improvement, and consumer services that are hard or impossible to be replicated by e-commerce.

Investor Presentation

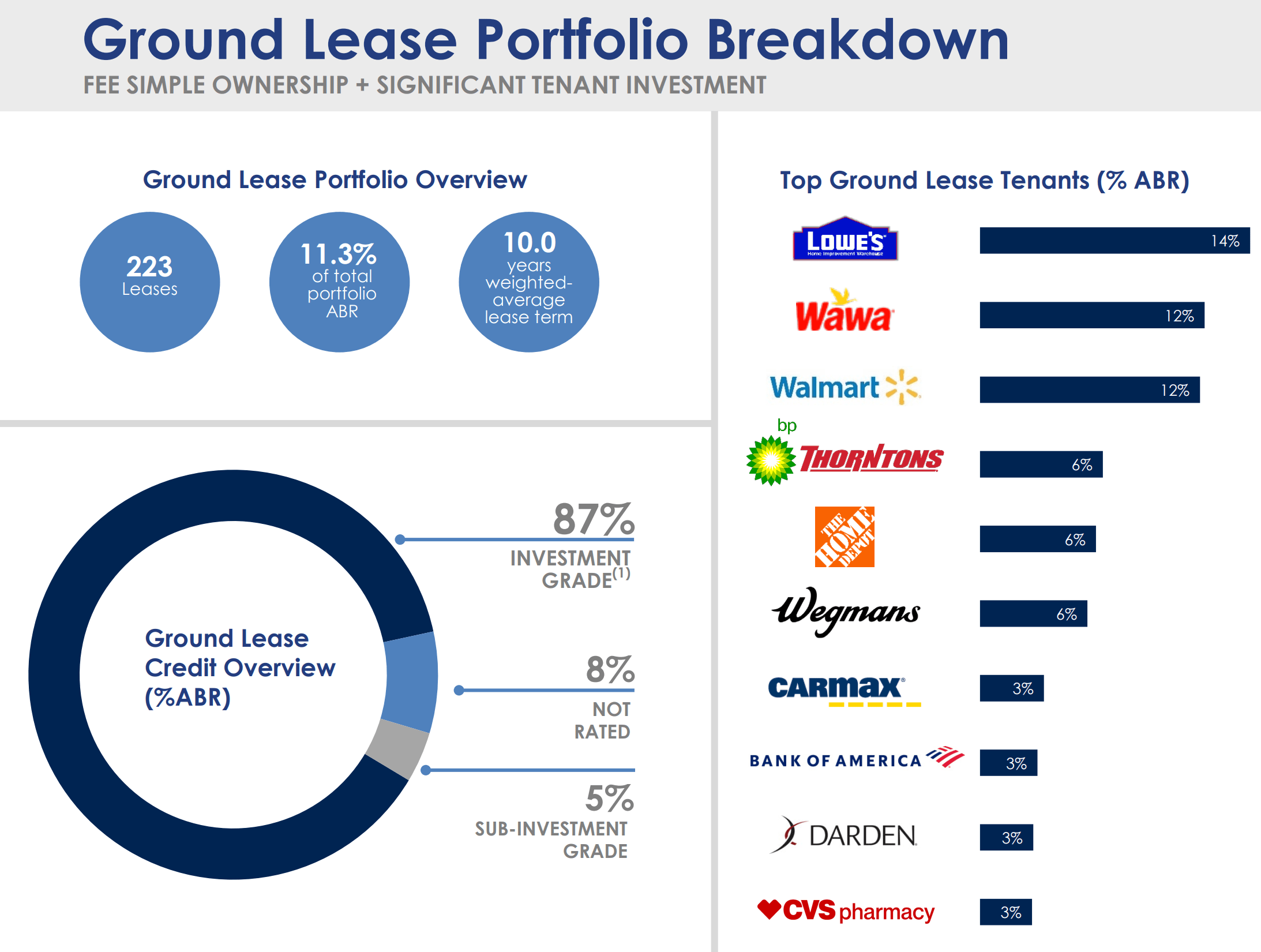

68% of ADC’s tenants carry investment-grade credit ratings, and ADC also has substantial exposure to ground leases, which represent 11% of annual base rent. These leases offer even higher safety than net leased properties due to ownership of the underlying land on which properties sit, and carry a weighted average lease term of 10 years. As shown below, top tenants include Lowe’s (LOW), Wawa, and Walmart.

Investor Presentation

ADC continues to demonstrate its ability to transact in this higher interest rate environment, acquiring 70 properties during the second quarter for $203 million. Contributions from new investments combined with annual rent escalators contributed to Core FFO per share growing by 5.7% YoY.

The acquired properties came at an attractive weighted average cap rate of 7.7%, representing a 90 basis points increase from the prior year period, and have a 9-year weighted average lease term.

The current higher interest rate market benefits well-capitalized REITs such as ADC, due to their cost of capital advantages. This is reflected by healthy investment spreads, with ADC issuing a 10-year bond for $450 million during the past quarter at a relatively attractive interest rate of 5.625%. ADC also carries a favorable cost of equity at 5.7%, based on its forward FFO per share of 17.6.

This equates to a combined cost of capital (debt and equity) of around 5.7%, which translates to a 200 basis points investment spread compared to the aforementioned 7.7% cap rate on property acquisitions.

Management raised its full-year FFO per share guidance by 20 cents to $4.13 at the midpoint of the range, representing a 4.4% growth rate from the 2023. This is based on expectations for continued high occupancy, which currently stands at 99.8% and the ability to recapture vacated Bed Bath & Beyond properties at higher rents, as noted during the recent conference call:

We are negotiating multiple letters of intent for the remaining parcels and will move to lease this quarter. As previously discussed, we anticipate recapturing over 150% of the former Bed Bath & Beyond rent, further highlighting our ability to identify and underwrite value-add real estate. As a result of our asset management team’s efforts, our 2024 lease maturities now stand at just 0.1% of annualized base rents.

Meanwhile, ADC carries a very strong balance sheet with BBB+ and Baa1 credit ratings from S&P and Moody’s. This is supported by $1.7 billion in liquidity, a net debt to EBITDA ratio of 4.9x, sitting far below the 6.0x level generally considered to be safe for REITs, and a strong fixed charge coverage ratio of 4.7x.

This lends support to the 4.2% dividend yield, which is well-covered by a 74% payout ratio. The current dividend rate is 2.9% higher than the prior year, sitting below the FFO/share growth rate, implying the preservation of retained capital to fund acquisitions.

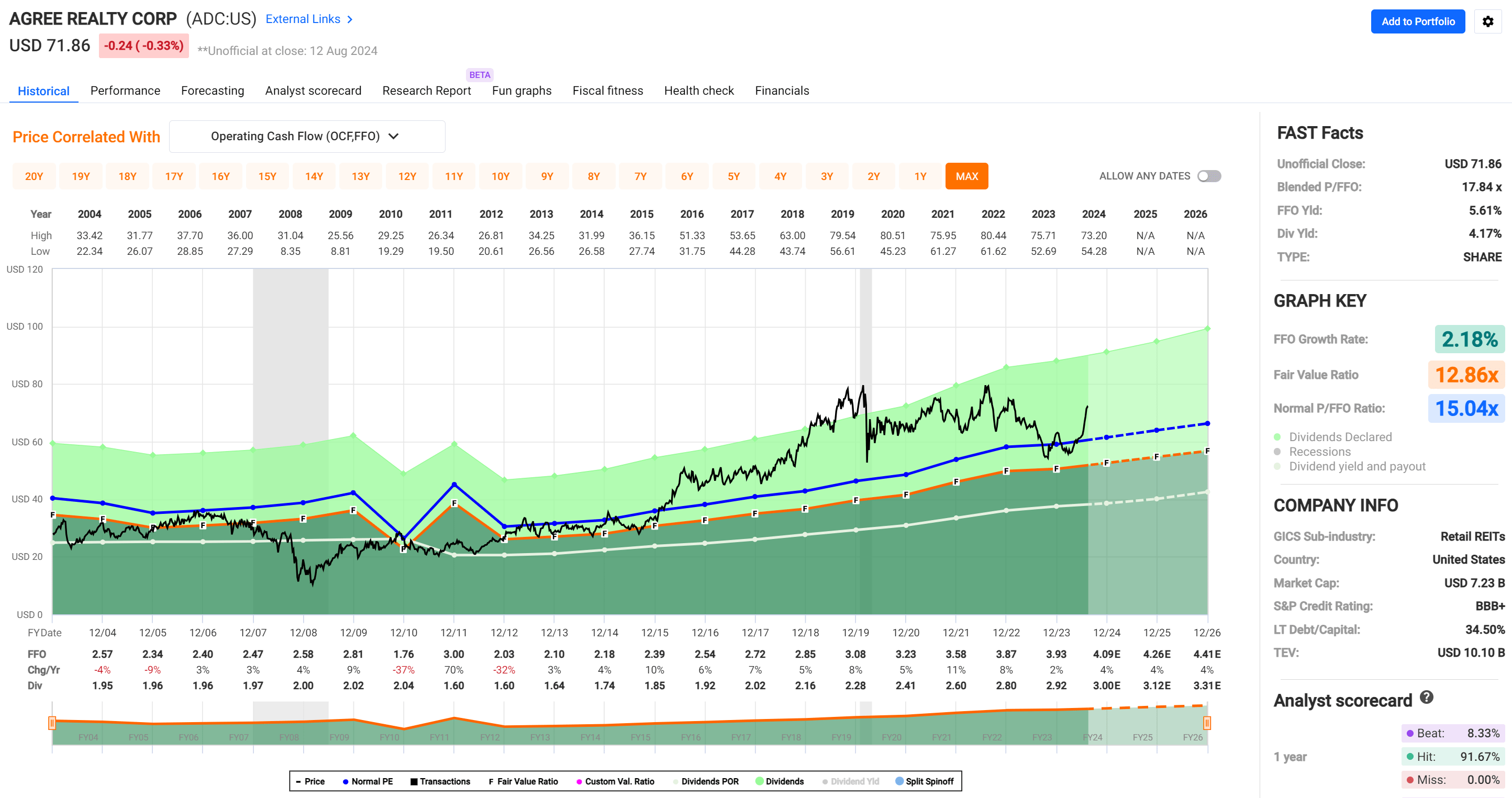

Turning to valuation, I believe much of the near-term alpha for ADC has already been realized at the current price of $71.86 with a forward P/FFO of 17.6x. As shown below, this sits above its historical P/FFO of 15.0.

FAST Graphs

With ADC trading comfortably above its normal valuation, I believe investors run the risk of overpaying at the current price. However, existing holders should benefit from accretive equity raises done by the company at these prices.

That’s why investors who want exposure to this company may want to consider the Preferred Series A (NYSE:ADC.PR.A), which carries a 5.6% yield at present, comparing favorably to the 4.5% rate on the 1-year Treasury Bond.

At the current price of $18.95, ADC.PR.A also trades at a 24% discount to its $25 par value. This means that even if the shares are called away on 9/17/26, investors get to realize the 24% capital gain plus all dividends accumulated along the way. Notably, this preferred series is also cumulative, which means that any missed dividends must be made up unless the company becomes insolvent.

Risks to the thesis include the potential for higher-for-longer interest rates, which may make both the common stock and preferred issue less attractive to investors, resulting in downside risk. Other risks include the potential for tenant headwinds due to a recession, which may result in them having trouble paying rent and negative sentiment around ADC’s stock, resulting in higher cost of equity.

Investor Takeaway

Agree Realty stands out as a resilient pick for income-focused investors due to its robust portfolio of recession-resistant, necessity-based tenants, including major retailers like Walmart and Kroger. With a strong balance sheet, solid credit ratings, and a well-covered 4.2% dividend yield, ADC is well-positioned to weather economic fluctuations and maintain steady growth.

However, ADC’s common stock has already seen significant gains, making its valuation higher than usual, and in my opinion, muting near-term alpha potential. As such, investors might consider its Preferred Series A shares, which offer a compelling 5.6% yield and potential capital gains at a discount, as a more attractive alternative at this time.