One of the best performing fixed-income asset classes of the first half of 2024 is still looking attractively valued, according to PineBridge’s co-head of Asia fixed income Andy Suen.

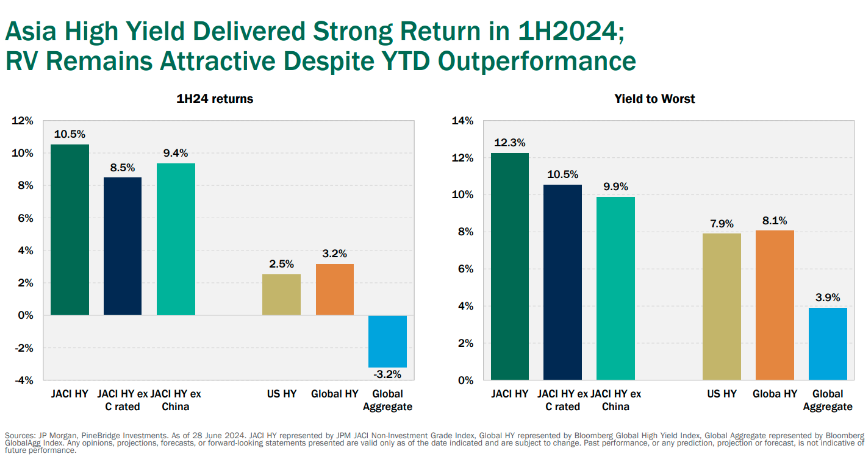

During the first half of 2024, US-dollar denominated Asian high yield bonds delivered a 10.5% total return compared to just 2.5% from US high yield and 3.2% from global high yield bonds.

This makes Asian high yield bonds, as measured by the JP Morgan Asia Credit Index (JACI), one of the best performing fixed income asset classes globally so far in 2024.

Yet despite this “stellar” performance from the once battered Asian bond market, it still looks reasonably valued, in Suen’s view.

“We are looking at a market which is offering higher yield but lower default rates,” Suen said at a recent media briefing.

He explained that Asian high-yield bonds excluding Chinese property names still delivered a strong total return over the same period: up 9.4% in total return terms.

A recovery in distressed Chinese property bonds

One of the main drivers for Asian high yield outperformance this year was a rally in distressed bonds, including Chinese property.

Aside from Chinese property bonds, the more distressed paper from triple-C issuers and various frontier sovereign bonds rallied significantly in the first half of 2024.

“These recovered quite strongly in the first half because they were trading at really distressed prices at the beginning of the year,” Suen explained.

But even if these lower quality issuers are stripped away, the Asian high yield excluding China index delivered returns well ahead of US high yield, which was weighed down by changing interest rate cut expectations.

Suen said: “After this round of strong performance we actually think the market is still cheap versus other major high yield markets.”

He pointed out that on a yield to worst measure, the JACI high-yield index has well over 400bp pick-up in yield versus the US high yield and global high yield indices (as shown in the bar charts below).

Even when taking out the triple-C segment of the Asian high yield bond market, which includes the distressed names, he flagged a 250bp additional yield versus US and global high yield.

Less defaults expected

Although the Asian high-yield bond market over the past few years has experienced a heavy round of defaults caused by the Chinese property market downturn and the spillover effects, Suen is optimistic on future default rates for the market.

He said defaults in the market peaked at 17% in 2022, then declined to 10% in 2023 and he now expects it to moderate at 4%-5% this year.

“One important thing to emphasise is that the defaults have been concentrated at the China property sector,” he said. “They account for over 90% of the defaults in Asia over the past couple of years.”

“If we put China property aside, the default rates historically in Asian high yield excluding China property is lower than US high yield.”

He pointed to how Asia high yield excluding Chinese property had a default rate of 1.3% last year versus 2.8% in the US high yield market in 2023. In 2022, the default rate was 0.9% versus 1.7% in the US high yield market.

Suen expects default rates in Asia high yield (excluding Chinese property) to stay below 2% this year.

One reason for this is because of how much more diversified the Asian high-yield market is compared to three years ago when it was dominated by Chinese property.

Another reason he cited was the market’s “very well managed maturity profile” and the access to local funding markets in Asia despite the US rate hikes.

He said: “The local markets in Asia, including China, have been quite favourable for funding from a cost perspective compared to US dollar funding.”

“If a company can assess the local markets, they are able to manage down their debt and funding costs.”

In terms of which sectors Suen prefers, he likes those where fundamentals continue to improve, namely Macau gaming, Indian renewable energy and short-dated paper from the commodity sector.