In the first half of this year, companies’ net issuance of corporate bonds shrank to the lowest level in 10 years since 2016. It is interpreted as a result of preferring bank loans to capital market procurement due to the aftermath of rising market interest rates. It is predicted that this trend will continue in the second half of the year.

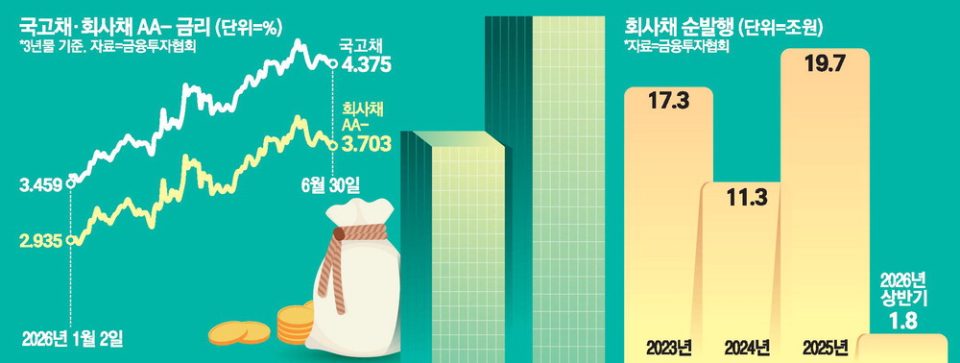

According to the Korea Financial Investment Association on the 5th, the total amount of corporate bonds issued in the first half of this year was 67.3783 trillion won. The figure is down about 10% from 74.9574 trillion won during the same period last year. Among them, net issuance amounted to 1.8531 trillion won, a 90% drop from 19.7323 trillion won in the first half of last year. This is the lowest level in 10 years since 2016 (2.489 trillion won). Net issuance is a new issuance minus maturity repayment, which refers to the amount of funds that companies have actually raised in the corporate bond market.

The corporate bond market has maintained a net issuance trend since it recorded net repayment in 2014 (-2.1667 trillion won), but its size has virtually fallen to the bottom level this year. This means that there are more cases in which companies do not refinance maturing corporate bonds and finish them with repayment, which is interpreted as a significant contraction in corporate financing through capital markets.

Rising market interest rates have further frozen the corporate bond issuance environment. The interest rate on AA-grade three-year corporate bonds has risen from 3.4% at the beginning of the year to 4.4% recently. The interest rate difference with the three-year treasury bond also widened from 52bp (1bp = 0.01 percentage point) at the beginning of the year to 67bp. The higher the interest rate, the greater the interest burden on companies issuing bonds, and the lower the price of existing bonds for investors buying bonds, leading to a vicious cycle in which both demand and supply contracted.

Companies seem to have turned to bank loans instead of issuing corporate bonds. As of the end of the first half of this year, the balance of corporate loans by the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup) was 873.84 trillion won, up 28.3591 trillion won from the end of last year. Banks have also been active in lending to companies. This is because financial authorities are curbing household loans from banks to manage household debt, while corporate loans are encouraged in terms of productive finance.

There is also an analysis that procedural reasons have also affected it. In order to issue bonds, they have to go through complex procedures such as demand forecasting, securities report submission, and investor recruitment, while bank loans are relatively simple as they are focused on confirming collateral. Analysts say that if the interest rate burden is similar, it is a natural trend for companies to choose bank loans with a simple procedure.

“While rising interest rates have dampened demand for corporate bonds, banks are actively taking on corporate loans as authorities tighten household loans and encourage productive finance,” a bond market official said. “From a corporate point of view, it is a flow that naturally moves to bank loans instead of issuing corporate bonds.”

It is observed that this trend will continue in the second half of the year. In the early stages of the rate hike, there is a high possibility that the credit spread (the difference in corporate bond rates compared to government bonds) will continue to expand due to a rise in short-term interest rates, which will increase companies’ procurement costs and reduce investor demand. As short-term procurement measures such as corporate bills (CPs), which have lower interest rates than corporate bonds, are still in effect, the incentive for companies to issue corporate bonds is not expected to be large for the time being.

“As the net repayment of corporate bonds continues in the second half of the year, the issuance market is expected to remain sluggish,” said Kim Eun-ki, a researcher at Samsung Securities. “The recovery of the corporate bond market will be possible only when investment demand increases due to the increased absolute interest rate merit as it enters the second half of next year rather than the second half of this year.”

[Reporter Oh Goes Back]