tum3123

I always like high yield and high dividend investments, especially when I make them through ETFs or other types of funds. I haven’t really encountered many passive funds that weren’t at least able to preserve their value. I started a DCA (Dollar Cost Averaging) strategy on iShares Broad USD High Yield Corporate Bond ETF (USHY) during the 2022 drawdown, which I discussed in this article. I haven’t updated it since, but I have to say that I’m quite satisfied with my choice, especially now, after the significant drawdown in the S&P 500.

Unfortunately, the spread between US High Yield and Investment Grade bonds rapidly decreased, reaching a historical low. For that reason, I shifted my focus and my DCA strategy to the global bond market, particularly the investment grade sector. Why? It’s simple—the risk premium became more attractive. I wrote about this in this article.

However, I want to be very clear: if I had to choose something to invest in for the long term, I would prefer to accumulate more shares of a high yield fund rather than a “monetary fund.” Why? Again, it’s pretty simple. The diversification within a high yield corporate bond fund lowers the risk while maintaining strong performance, providing great alpha to this type of fund.

And today, I don’t want to miss the opportunity to accumulate in the most ‘dangerous’ segment of the high yield markets: the emerging markets. I will do this by using the VanEck Emerging Markets High Yield Bond ETF (NYSEARCA:HYEM)

Why choose the VanEck Emerging Markets High Yield Bond ETF?

By following the structure of the benchmark (ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index), it becomes easier to estimate the composition. The current geographical composition of the fund is as follows:

- China: 12.43%

- Turkey: 8.49%

- United Kingdom: 8.21%

- Brazil: 6.61%

- Colombia: 5.47%

- Mexico: 5.39%

- Argentina: 5.33%

- India: 4.24%

- United States: 3.52%

- Israel: 3.11%

This is a really curious composition, don’t you think? It’s interesting to see UK bonds make up about 8.21% and U.S. bonds about 3.52% of this ETF. Why? I think this is a good composition choice, as it could help stabilize the ETF’s performance.

A slight negative note: the Total Expense Ratio (TER) is 0.40%, which is somewhat high, especially considering that the ETF also invests significantly in non-emerging markets (like the UK).

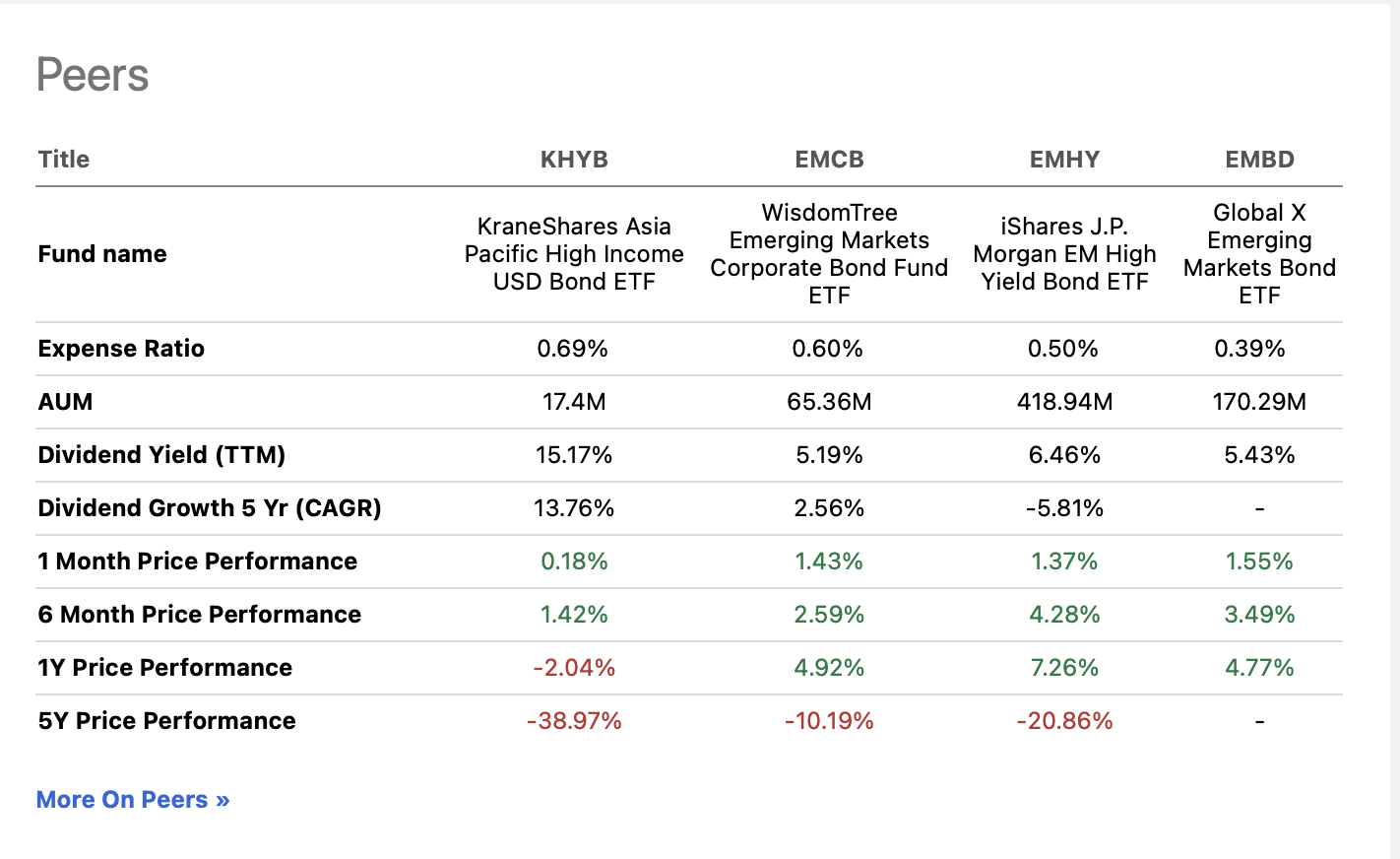

But don’t worry; this parallel with its peers should reassure investors because HYEM shows a performance chart in line with other passive funds.

And at least, the expense ratio itself is not higher than its peers.

HYEM peer (seekingalpha)

Why I think it has become a great time for high yield in emerging markets.

There are a few reasons to become bullish about high yield in emerging markets; many of these I already introduced when I discussed my investment in BNDX, to take advantage of the global investment-grade market ex-USA. The macroeconomic concepts behind these ideas are similar, and that intuition also led me to write this content about the Brazilian stock market.

The motivation behind this conviction has become even stronger after the recent S&P 500 collapse, along with the sudden increase in the risk of recession.

So why could investing in HYEM be a good decision right now? For two reasons:

Increase in the risk of recession

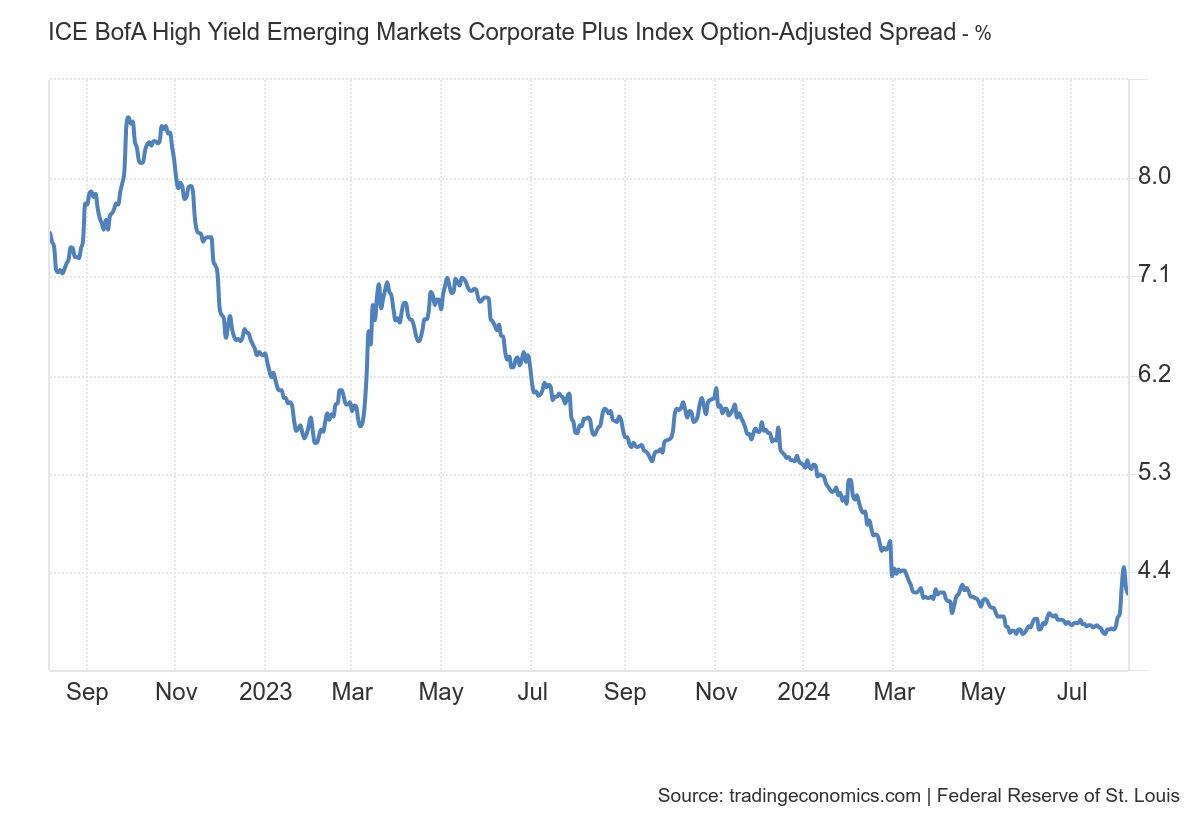

The increase in the risk of a U.S. recession is affecting the ICE BofA High Yield Emerging Markets Corporate Plus Index Option-Adjusted Spread. Currently, it is around 4.20%, whereas the average over the past few years was above 10%. So, I’m not saying this is the greatest risk premium we’ve seen recently. On the contrary, even though the spread has increased in the U.S. and Europe, in emerging markets, the investment discount reflects an unusual stability. Why? It’s difficult to pinpoint, but it could be that the increased recession risks in the U.S. might lead to higher demand for EM bonds.

ICE BofA High Yield Emerging Markets Corporate Plus Index Option-Adjusted Spread (tradingeconomics.com)

In my opinion, this will lead to a decrease in the price spread between U.S. high yield and EM high yield, which had widened significantly during the Federal Reserve’s interest rate hikes.

So, I’m not saying that HYEM will go up and USHY will go down; there is a positive correlation between these two ETFs. I believe the performance spread will decrease significantly, thanks to an outperformance of the EM sector.

Whether one believes in a hard landing or a soft landing, the bond market, particularly in the United States, will continue to price in further rate cuts by central bankers, leading to an appreciation of investment-grade bonds in ETFs like USHY, which may negatively impact yields.

DXY is contracting

Additionally, the carry trade between Japanese and U.S. bonds is exacerbating this macroeconomic instability, and the DXY is contracting even more than could have been expected from the natural course of events, as discussed in this article. A weaker dollar can be positive for emerging markets today, and I think it might be interesting to consider starting a DCA on this ETF, as many of their bonds are denominated in dollars. With a weaker dollar, dollar-denominated debt becomes less burdensome for emerging markets to repay, reducing the risk of default and thereby supporting bond prices.

What could go wrong?

As you may know, in the short term, a recession tends to work against emerging markets because, as happened during the 2008 crisis, the dollar could paradoxically strengthen due to a ‘flight-to-safety.’ However, in my opinion in the long term, these declines (already widely priced in by the market) could make emerging market bonds more attractive to international investors due to their relatively higher yields, potentially increasing demand for these bonds. This, too, is a cyclical issue.

Similarly, it is important to note that a very low OAS could also indicate that investors are underestimating the risk, which could lead to vulnerabilities if market conditions suddenly worsen. Often, lows of this level have preceded severe global crises in the past; however, this does not mean that this ETF cannot still reduce the performance spread compared to other high-yield options

Conclusion

In conclusion, I would like to reaffirm the ‘hold’ rating for HYEM for several reasons. In my opinion, the ICE BofA High Yield Emerging Markets Corporate Plus Index Option-Adjusted Spread provides valuable insights for our analysis. Additionally, recent developments suggest a potential decrease in the DXY, which could positively impact the emerging markets sector.

Moreover, I would like to offer a consideration that I believe some might discuss with me in the comments: if it is important to maintain adequate diversification in a balanced portfolio, and if that means including debt from all countries, what better time to increase or build a position in HYEM than now?