Market volatility has exceeded the estimates in my outlook as a result of the unforeseen Iranian crisis. Growth expectations are likely to be challenged and inflationary pressure may reassert itself on the monetary policy narrative depending upon the duration of the conflict and the associated disruption to the free flow of oil through the Strait of Hormuz. The impact of overall supply chain disruption will need to play out as a potential accelerant to inflation.

Processing Content

The risk-on/risk-off pendulum is in full swing, with directional movement tied to the day’s rhetoric. During these periods of market uncertainty, fixed-income investors are encouraged to maximize strategic decision-making as a way to shield portfolios from episodic shocks and benefit from investment opportunities.

Emergent crisis-related conditions have meaningfully elevated the value proposition across the municipal bond market, with particular attention being paid to compelling yield and income conditions made prominent by duration extensions. Although we are witnessing evolving credit concerns, largely brought on by shifting policy developments, overall credit quality remains resilient.

Municipal bonds are known to provide a shelter for tax-efficient strategies, yet the tax-exemption may not be as valuable for lower bracket investors, tax-advantaged accounts and certain classes of institutional and crossover buyers. This is where taxable municipal bonds can bridge the efficiency gap and still provide portfolio diversification and credit ballast.

Domestic buyers of taxable munis are generally not incentivised by the tax-exemption, with life insurance companies, pension funds, and IRA accounts comprising the primary audience. Life insurance companies in particular benefit from the asset/liability matchup that longer duration taxable munis provide.

Taxable munis offer a viable investment alternative to conventional taxable asset classes and their inherent characteristics more than offset the liquidity premium associated with municipal securities. Taxable munis have the ability to engineer wide-ranging portfolio diversification with longer duration (relative to investment-grade corporates), a low risk correlation to equities and corporates, lower volatility, and upside spread potential. I would point out, however, certain taxable buyers may avoid taxable pension obligation bonds, given their connection with the stock market.

Although volatility-induced yield spikes can produce opportunistic entry points, particularly as fund flows turn negative, attendant spread-tightening could favorably impact performance. Many investors acquire taxable munis that are benchmarked against a taxable index, but additional yield pickup may be available with smaller CUSIPs that are not benchmarked. Taxable munis do have relatively greater sensitivity to interest rate changes.

Taxable munis offer higher yields than tax-exempts, with outsized spreads typically emerging during episodic market dislocations, such as the Build America Bond (BAB) phenomenon (2009), taper tantrum (2013), and COVID (2020). The long-term average spread between tax-exempts and taxable munis ranges between 100 and140 basis points, with wider spreads of between 160 and 170 basis points now being seen, reflecting heightened market volatility. The introduction of BABs spiked taxable muni yields and altered the buyer base with significant crossover interest.

Taxable munis enjoy similar credit dynamics of a low default experience and high recovery rates that backdrop the broader municipal bond market. Taxable muni yields are generally higher than those on U.S. Treasuries, and while they are more aligned with investment-grade corporate yields, credit quality disproportionately favors taxable municipal bonds.

Issuers and municipal advisors appreciate the flexible nature of taxable munis as the Internal Revenue Code prohibits the use of tax-exempt municipal bonds for certain purposes and projects, and there are more liberal requirements detailed in the offering documents about how taxable muni bond proceeds are to be used. Given that the Tax Cuts and Jobs Act of 2017 removed the ability to issue tax-exempt bonds for advance refunding purposes, taxable munis can step in under appropriate market conditions.

Call optionality on taxable munis may be more beneficial to investors, as many are structured with “make-whole” calls, which compensate the investor for loss of future cash flow should bonds be subject to early redemption. The “make-whole” provision may be more appealing for life insurance companies as opposed to standard par calls, given their need for asset/liability alignment.

The call price for “make wholes” is typically formula-based, being the greater of par or the present value of remaining discounted cash flows (Treasury yield plus stated spread). This structure is typically associated with BABs and munis with corporate CUSIPs. Extraordinary redemption calls, which are embedded in BAB deals, protect issuers should subsidy reductions occur through sequestration and are generally less predictable than standard 10-year calls given policy nuances.

To a large extent, wider spreads available on BABs compared with other taxable munis and comparable IG corporate bonds can be attributed to these inherent call features. Lower dollar (below par) callable bonds where the call is “out of the money” may provide opportunities in the taxable space — such as additional yield and improved total returns — should spreads tighten.

Meaningful expansion to the taxable municipal bond market can trace its genesis back to the Tax Reform Act of 1986, which tightened eligibility standards for tax-exempt issuance, lowered top marginal tax rates and imposed more stringent arbitrage rebate rules — all dilutive for the tax-exemption. These developments elevated the competitive advantage of taxable munis in many situations and led to compelling interest from the crossover buyer.

The introduction of the taxable BAB program through the 2009 passage of the American Recovery and Reinvestment Act was designed to finance “bedrock” municipal projects, attracting a broader group of foreign and domestic buyers that did not historically participate in the tax-exempt municipal bond market. Many of these investors previously focused on corporate IG and U.S. Treasury debt. Just over $180 billion of BABs were issued in 2009 and 2010 before the program expired at the end of 2010.

The appeal of taxable munis extends to portfolio-optimization and relative-value-centric foreign buyers who are not seeking tax-efficiency, yet who are strategizing to diversify their portfolios and boost investment performance with a view to investing in U.S. infrastructure. Taxable muni interest grows stronger when foreign sovereign yields turn negative, as was the case during the COVID period.

Less restrictive capital set-aside requirements for foreign insurance companies when acquiring infrastructure debt and their liability-driven objectives requiring long-dated assets add further support. Currency considerations and hedging costs are not unique as similar challenges apply to Treasuries and corporates.

Active interest can be found in Europe and Asia, and as of Q4 2025 foreign investors held about 2.9%, or approximately $125 billion of the $4.3 trillion municipal bond market according to Federal Reserve data. By comparison, about 30% of U.S. Treasury securities are held by foreign investors.

I do not expect foreign ownership of municipal bonds to grow beyond the margins in the foreseeable future. As mentioned, the tax-exemption offers no benefit to foreign buyers. The various inefficiencies illustrative of the muni market — including fragmented supply, over 50,000 issuers, tighter liquidity, embedded call features, and lighter disclosure and transparency — soften foreign interest.

In addition to logistical challenges, a thinly traded taxable muni market, smaller deal sizes, pushback for certain sectors and credit types with a general lack of credit resources, and relatively low portfolio (foreign) turnover make foreign portfolio allocations into taxable munis difficult to scale. I also believe that shifting buyer dynamics, particularly with explosive SMA growth and a continued mutual fund presence, creates a more tailored deal formation for these cohorts and detracts from the focus on foreign investors.

I would point out that there are not many lower-rated munis of size and scale. Rating inefficiencies, however, tend to be more digestible by the foreign buyer once explained.

Further, the muni market’s reduced liquidity, credit concerns — such as unfunded pension liabilities —- , and municipal-centric political vagaries and associated headlines could undermine desirability.

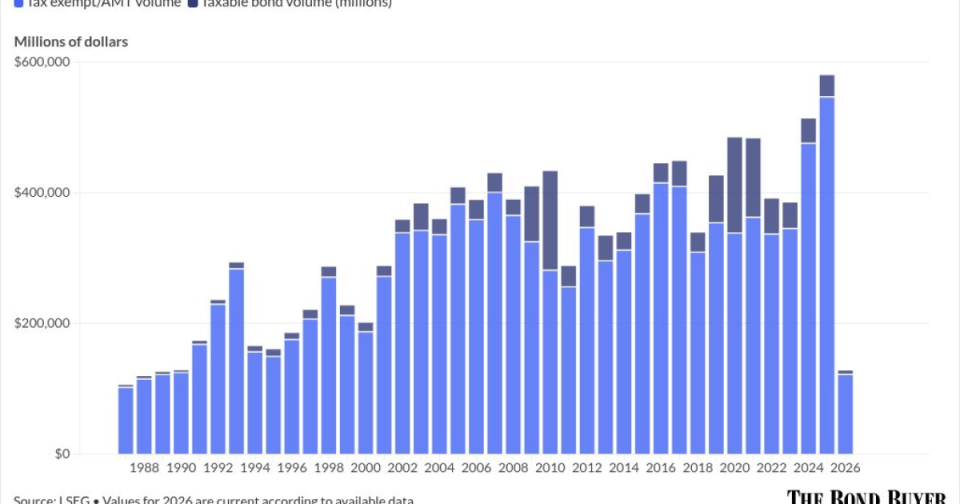

Looking at taxable issuance activity over the past five years tells an interesting rate-driven story. In 2021, taxable supply as a percentage of total issuance approximated 25%. Taxable issuance dropped to 13.9% of total in 2022, declining to 5.7% by the end of 2025. Year-to-date, taxable issuance is about 4.7% of aggregate volume.

The outsized taxable volume in 2021 was attributable to a pandemic-driven, near-zero interest rate environment, which triggered heavy taxable advance refunding issuance. Again, the Tax Cuts and Jobs Act of 2017 eliminated the ability to market tax-exempt advance refunding bonds. An aggressive rate-hiking cycle beginning in Q1 2022 to combat rising inflation removed the economics of doing taxable advance refundings and pushed taxable issuance market share significantly lower. With higher rates, tax-exempts became cheaper versus taxables, prompting issuers to book the lowest cost of funding.

A pivot to an easing bias in late 2024, given moderating inflation, kept taxable issuance on a steady downward course as the pool of refunding candidates was already thin against a still-elevated rate backdrop. I would also point out that issuer balance sheets still carried COVID stimulus funds, thus removing some of the urgency to refinance outstanding debt.

Taxable municipal bonds returned 7.89% in 2025 according to the Bloomberg taxable muni index, versus 4.25% for the broader investment-grade tax-exempt market. Outperformance for taxable munis was attributed to declining Treasury yields combined with “carry” attribution. For year-to-date 2026, taxable munis are underperforming the broader muni index as their longer durations are more sensitive to rising interest rates and geopolitical risks. However, taxable munis are outperforming both corporates and Treasuries year-to-date.

While taxable munis are heavily correlated with Treasuries — given the federal tax exemption and mutual competition for a similar institutional buyer base — they enjoy a degree of insulation from outside influences thanks to credit resiliency relative to IG corporates and strong technicals — largely due to light supply and heavy reinvestment demand. These factors have created fertile ground for spread compression within the taxable muni space.

Over the past three decades, taxable municipal bonds have been part of the investment narrative. Their appeal has been proven across tax advantaged accounts, lower-bracket investors, life insurance companies and crossover buyers. They enjoy the strong credit quality attributes that backdrop the public finance industry and they provide issuers with financing flexibility.

Taxable munis offer portfolio diversification and ample potential for outperformance. While they are not likely to see a significant advance in issuance, they may offer a more prominent financing solution as issuers address funding needs for infrastructure, cyber threat preparedness and climate change initiatives.