Hamilton Lane’s head of Canada explains how the ‘unsung’ benefit of alternatives helped investors in a tumultuous moment

There’s nothing like a US selloff on a Canadian holiday Monday. Last week’s equity drawdowns began when Canadians were still enjoying the August long weekend, though it’s unlikely that anybody in asset management was still enjoying themselves that Monday. The week of volatility that followed, with recovery rallies, false starts, and whipsaw swings were enough to give even seasoned investors a bit of whiplash.

Watching his own RRSP last week, Mike Woollatt says that he was reminded of a key tenet of his work: that private assets offer volatility offsets. Woollatt is the managing director and head of Canada at Hamilton Lane, one of the world’s largest private market investment managers. While private assets are often cited for their outperformance against public markets overtime, Woollatt thinks that this particular moment drives home their utility as a volatility offset.

“There’s long-term outperformance by private markets versus their public peers, and their performance all the way through is less volatile,” Woollatt says. “A lot of people point to the outperformance, but the unsung hero is that lower volatility.”

That volatility, Woollatt explained, is a product of a number of features in private assets. First and foremost is pricing frequency. Most private assets are priced on a monthly or quarterly basis through independent valuation reviews. Public assets go through intra-day price swings. Thousands of price snapshots will always imply a more volatile picture than two moments a month or three months apart.

Woollatt argues, however, that these assets have other underlying factors that result in lower volatility. In the case of private equity, governance structures play a key role. Where publicly held companies are subject to the competing whims of a vast array of shareholders and are focused more on delivering short-term returns, private equities are more able to focus on long-term growth.

Investors’ view of the assets also plays a role. Public equities are far more subject to rapid changes in investor sentiment. Private assets are often viewed more as a long-term asset, in part due to their relative illiquidity. That means investors are less likely to make short, sentiment-driven, entry and exit moves.

Concentration risk is another factor Woollatt is keenly aware of. He highlights just how concentrated US public equities have become, with a few mega-cap names dominating performance. Private assets, conversely, tend to involve a far greater degree of diversification.

“If we told our investors that one per cent of our investments are driving the vast majority of our returns, and we’re holding them at 45 times earnings, our investors would be coming at our valuations,” Woollatt says.

Those volatility offsets don’t insulate private assets from macro sentiment entirely, and Woollatt accepts that. He notes, as well, that there is some correlation between private and public markets — though at a bit of a lag. However, the broad array of names and styles that can be held in private asset portfolios, coupled with their aforementioned volatility offsets, the typical result is smoother investment returns.

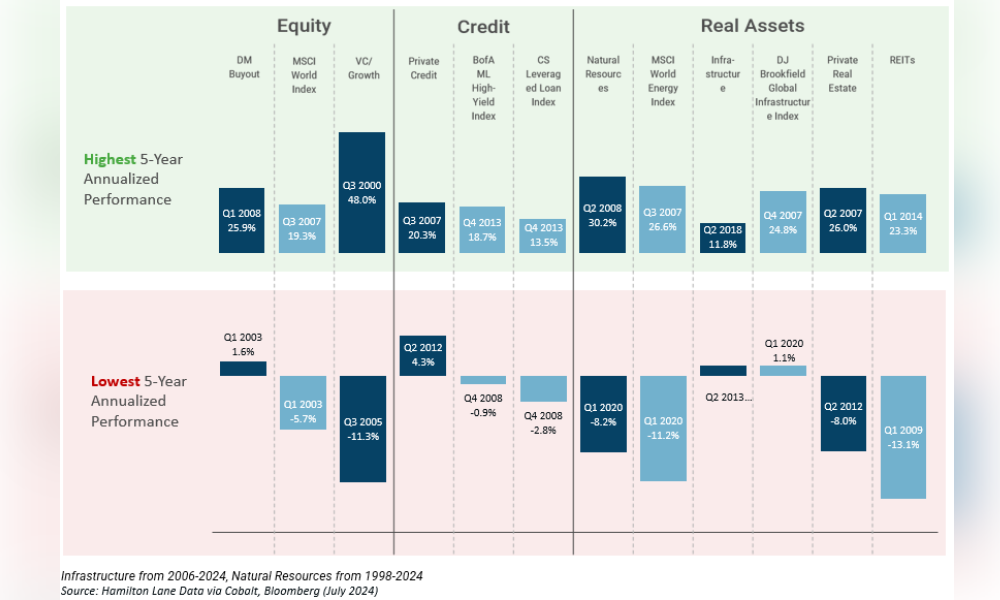

Woollatt cites the below graph – demonstrating the highest and lowest performance periods across asset classes, to show that private asset outperformance against public markets tends to be higher during down periods, with the notable exception of the VC/Growth category.

Woollatt explains that these returns profiles, and their broad lower volatility, make it far easier for asset managers to plan for the future. These assets can offset some of the stress that comes with your public market allocations. A more stable portion of the portfolio can help inform better decisions and provide an island of calm when public markets get stormy. Even the most experienced asset manager can experience some fear when markets start dropping below certain thresholds. The ballast of a private allocation — Woollatt argues — can help protect against panic-driven decision making.

“The advantage of having a private allocation that isn’t bouncing around daily like a roller coaster is pretty obvious. From a from a behavioral standpoint, you’re not having to jump on a million calls,” Woollatt says. “The outperformance is there and that’s great, but if the outperformance involved bouncing all over the place, it would be a lot less attractive of an asset for the long-term.”

RELATED ARTICLES