The private credit market is adjusting after a period of depressed dealmaking, as investors trim their exposure to software borrowers, according to LCD’s quarterly survey.

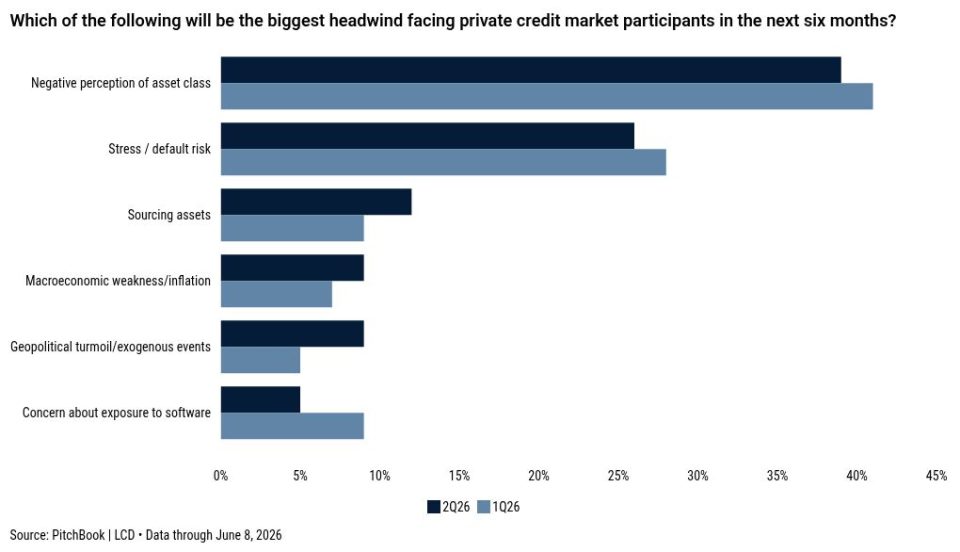

For a second consecutive quarter, survey respondents said the greatest challenge for private credit was the negative perception of the asset class, followed by credit stress and sourcing assets, survey respondents told LCD.

Compared to the Q1 survey, fewer respondents identified software risks among the top headwinds facing private credit, but many lenders have moved to shield their portfolios from the risks posed to software borrowers by generative AI.

Slightly more than half of those surveyed by LCD said they had reduced their exposure to software borrowers, including 21% who said they had significantly reduced their exposure and 6% who had stopped lending to them entirely. Nine percent of respondents said they had increased their exposure, looking to capitalize on the dislocation.

LCD’s second-quarter survey was conducted between May 27 and June 8. Respondents included a mix of credit providers, banks, PE firms, advisory firms and other market participants from the US and Europe.

Recalibrating

So far, Q2 has been a disappointment for those hoping for a brisk return to dealmaking. The three months through May have brought fewer deals than any quarter since 2023, according to LCD’s Private Credit Monitor.

However, respondents expressed optimism that deal flow would pick back up. A majority said they expected deal activity to increase at least slightly in the next 90 days.

Looking out over the next 12 months, several factors could accelerate M&A activity. The most important, according to respondents, is the wealth of dry powder in the PE market. Others said they are looking for an improved economic outlook, less geopolitical uncertainty or attractive valuations and distressed opportunities.

One of the most striking changes in the private credit market comes from the shift in pricing. In just two quarters, the percentage of respondents who reported that a unitranche loan to a non-cyclical business with $50 million of EBITDA would price below S+500 dropped to 21%, from 67% at year-end 2025.

A plurality expected such a loan would instead price at S+500-549; roughly a quarter suggested S+550-599.

However, respondents indicated that the premium pricing may not last. A plurality of respondents said they expected the same unitranche loan would price below S+500 six months from now. Notably, opinion was far from unanimous.

If those respondents are correct, that would renew a downward trend that has compressed spreads since 2022. The private credit market has increasingly been pricing in the S+450-499 range, LCD data shows.