IMPORTANT NOTE: This newsletter contains information for educational purposes only, and the content below should not be considered financial advice to readers. We DO NOT publish our short research and ideas on Substack for compliance reasons. We do not recommend shorting to retail investors. Our short ideas and research are only for institutional investors, not individual (retail) investors. If you are an institutional or sophisticated investor and would like to become our client, email laks@unicusresearch.com.

A UK bridging lender, Market Financial Solutions, applied for administration on 20 February 2026; administrators were appointed five days later. The loan book ran to about £2.4 billion. The firm collapsed owing roughly £2.6 billion to creditors, a list that includes some of the largest names in private credit and banking. Administrators accuse the founder, Paresh Raja, of misappropriating at least £1.3 billion from the business. Through a spokesman, Raja denies any fraud or dishonesty and says he will give his full account in court. He has reportedly left for Dubai. The Financial Conduct Authority has opened a formal enforcement investigation, and the Bank of England is examining the collapse.

MFS did not take deposits. It funded its loan book by borrowing from banks and institutions. The list of funders reads like a structured finance roll call: Barclays, Santander, Wells Fargo, Jefferies, Apollo’s Atlas SP, and Castlelake. Barclays froze MFS accounts in January 2026 after detecting anomalies in November.

The alleged mechanism was double pledging. The same property was pledged as collateral to more than one lender. When that happens, a lender who believed it held a senior, exclusive claim discovers the collateral is not there to take.

That is the part worth zooming in on. The banks did not lend to MFS’s end borrowers. They lent to MFS, a non-bank, which lent to the borrowers. The risk appeared to sit outside the banking system. It did not.

MFS is the small, ugly version of a much larger arrangement. We are mapping one redemption at a time to see the bigger picture.

Private credit is often described as the replacement for bank lending after 2008. That framing is half the picture. Banks sit underneath the private credit market. Banks are now financing private credit.

The Financial Stability Board, in its 6 May 2026 report on vulnerabilities in private credit, sets out the connections plainly. Banks lend to private credit funds. Banks lend to the same companies that the funds lend to, often through a revolving facility sitting alongside the fund’s main loan. The banks run partnerships with the asset managers that manage the funds. Banks also provide warehouse financing to CLOs, and they invest in private credit CLOs themselves. The market they supposedly ceded is partly underwritten by their own balance sheets. The private credit market reached about $1.75 trillion in 2025, according to one industry estimate, and banks channel a meaningful share of it.

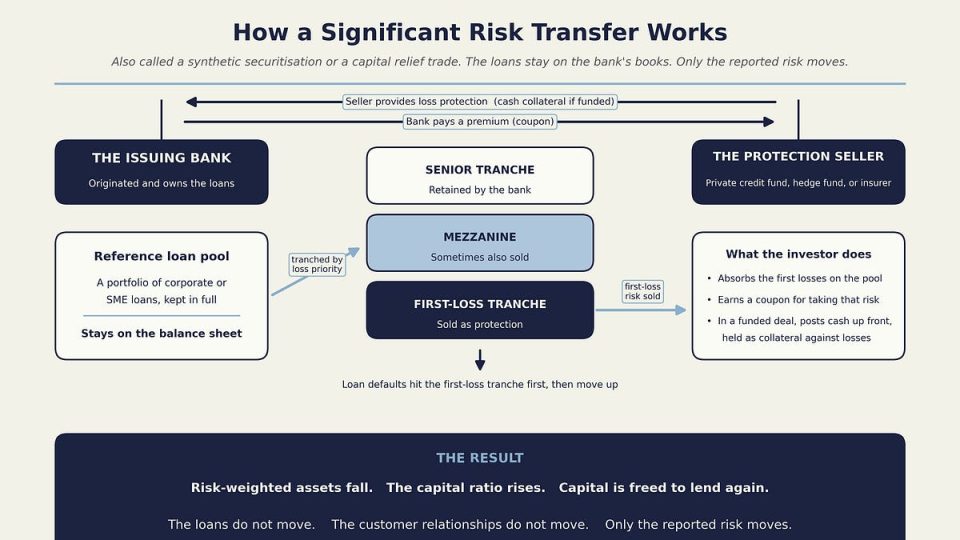

Then there is the cleanest connection of all, the one this piece is about. Banks use synthetic risk transfers (SRTs) to shed credit risk on loans they keep while the loans remain exactly where they are.

On May 30, we published Deep Dive II and mapped the MFS chain: a UK borrower, a US warehouse platform, a UK G-SIB loss, a Singaporean exit, and a Gulf substitution. Five regulatory perimeters in under three weeks, and no single regulator has visibility into the full mechanics.

THINK ABOUT THAT FOR A MOMENT.

This piece picks up where our May 30th article left off. Below the paywall: who is issuing, who is buying, who is lending to the buyers, what Minsky would have called the funding model, and why, by the regulators’ own admission, no one can trace the chain.