Ares Management Corporation ARES and KKR & Co. Inc.KKR are prominent alternative asset managers with diversified investment platforms across private equity, credit and real assets. ARES primarily focuses on alternative investment solutions spanning credit, private equity, real assets, secondaries and insurance-related strategies. In contrast, KKR operates a broader model that integrates alternative asset management with capital markets and insurance solutions. Both firms benefit from strong institutional relationships, wide-ranging investment capabilities and expanding sources of perpetual capital. However, differences in business mix, growth strategies and revenue drivers could shape their relative performance going forward.

The asset-management industry is navigating a shifting operating backdrop. Rising investments in technology and artificial intelligence are increasing cost pressures, while the rapid growth of ETFs, especially actively managed products, is intensifying competition. Additionally, concerns around private credit markets may weigh on near-term flows into select alternative investment strategies. Still, favorable market conditions and steady inflows continue to support AUM growth across the industry.

Against this backdrop, investors naturally ask: Which firm, ARES or KKR, is better positioned for long-term growth? To answer that, we need to examine their fundamentals more closely.

The Case for ARES

Ares Management has been strengthening its platform through strategic acquisitions and partnerships. In February 2026, the company acquired BlueCove Limited to strengthen its credit platform and partnered with Slate Asset Management to acquire a Polish retail real estate portfolio, expanding its European footprint. Earlier, the company acquired GCP International in 2025 to broaden its real assets platform. Together, these initiatives have diversified Ares Management’s investment offerings, expanded its global footprint and strengthened its position across key alternative asset classes, supporting long-term growth prospects.

Supported by these strategic acquisitions and partnerships, Ares Management’s AUM has witnessed consistent growth over the years. Strong fundraising activity through the wealth management channel, growing insurance-related assets, and continued demand for private credit, real assets and secondaries strategies have supported its AUM growth. Further, the company’s expanding perpetual capital base and broad distribution network are expected to drive fundraising and deployment activity. With management targeting AUM of more than $750 billion by 2028, ARES appears well positioned to sustain growth over the long term.

Organic growth remains a key strength for Ares Management. Higher management and performance fees from a growing fee-paying asset base have continued to support revenue growth. The acquisition of GCP International has further enhanced the company’s real assets and digital infrastructure capabilities, adding incremental management fee revenues. Management continues to target annual organic growth of 16-20% or more in fee-related earnings and more than 20% growth in realized income over the medium term. Going forward, continued expansion in private credit and real assets is expected to support revenue growth and earnings generation.

However, ARES’ expense base has been rising due to higher compensation and benefits costs, ongoing investments in fundraising and platform expansion, and expenses associated with integrating acquired businesses. These factors are likely to keep costs elevated and could pressure near-term profitability.

The Case for KKR

KKR has been expanding its platform through strategic acquisitions to enhance its investment capabilities and drive asset growth. In May 2026, the company acquired Arctos Partners, an investment firm managing approximately $16 billion in AUM, expanding its capabilities across sports investing, GP solutions and secondaries. Earlier, in July 2025, KKR acquired a majority stake in HealthCare Royalty Partners, adding nearly $3 billion to its AUM and expanding its healthcare-focused investment capabilities. These initiatives have supported KKR’s efforts to scale its alternative investment platform, diversify revenue streams and accelerate AUM growth, positioning the company well for long-term expansion.

Building on these initiatives, KKR’s AUM balance has grown steadily over the years, reflecting the strength of its diversified investment platform. The company’s expanding presence across private equity, credit, infrastructure, real estate and insurance has supported AUM growth, while fundraising and capital deployment activity have remained healthy. Further, a growing perpetual capital base and continued expansion of investment capabilities are expected to support future asset growth. The Arctos acquisition is also expected to increase KKR’s exposure to perpetual and long-dated capital and strengthen its wealth and institutional distribution capabilities. Management’s goal of reaching at least $1 trillion in AUM by 2030 further underscores confidence in the company’s long-term growth prospects.

Organic growth also remains a key strength for KKR. The company continues to benefit from the expansion of its traditional private equity and third-party businesses while adding capabilities across infrastructure, real estate, growth and core investing strategies. These efforts have increased deal activity and broadened KKR’s revenue base over time. Continued expansion across these investment platforms is expected to support revenue growth and earnings generation over the long term.

Nevertheless, an elevated expense base remains a headwind for KKR. Higher commission, reinsurance and employee compensation expenses have increased costs, while continued fundraising activity is expected to drive higher placement fees. This could pressure the company’s near-term earnings growth.

How Do Earnings Estimates Compare for ARES & KKR?

The Zacks Consensus Estimate for ARES’ 2026 and 2027 earnings implies a year-over-year rise of 27.3% and 24.4%, respectively. Earnings estimates for 2026 have been revised upward, while for 2027, it has remained unchanged over the past month.

ARES Estimates Revision Trend

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for KKR’s 2026 and 2027 earnings implies a year-over-year rise of 24.6% and 23.5%, respectively. Earnings estimates for both years have been revised upward over the past month.

KKR Estimates Revision Trend

Image Source: Zacks Investment Research

ARES & KKR: Price Performance, Valuations & Other Comparisons

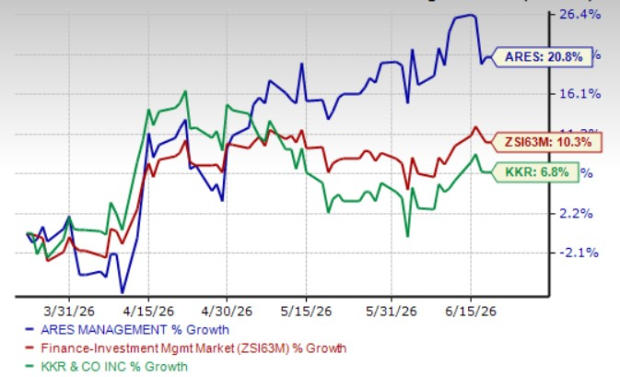

Over the past three months, ARES and KKR shares gained 20.8% and 6.8%, respectively, compared with the industry’s growth of 10.3%.

Price Performance Comparison

Image Source: Zacks Investment Research

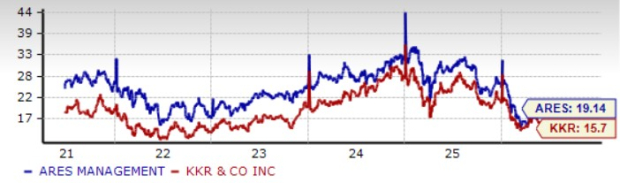

From a valuation standpoint, ARES is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 19.14X, while KKR is currently trading at a forward 12-month P/E multiple of 15.7X. Both are trading at a premium compared with the industry average of 13.66X; however, KKR stock is cheaper than ARES.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

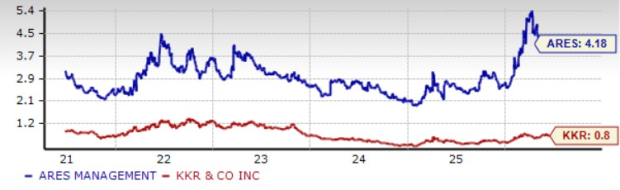

Meanwhile, both Ares Management and KKR & Co reward their shareholders handsomely. In February 2026, ARES raised its quarterly dividend by 20.5% to $1.35 per share. It has a dividend yield of 4.2%. Similarly, KKR raised its annualized dividend by 5.4% to 78 cents per share in May 2026. It has a dividend yield of 0.8%.

Dividend Yield

Image Source: Zacks Investment Research

ARES or KKR: Which Stock Offers More Value?

Ares Management and KKR & Co. both benefit from diversified alternative investment platforms, growing perpetual capital bases and healthy fundraising activity, supporting long-term AUM growth. Both companies are also expanding through acquisitions to strengthen their investment capabilities and broaden their market reach.

However, ARES appears to have a slight edge, supported by stronger earnings growth expectations and a significantly higher dividend yield. While KKR trades at a lower valuation and offers solid growth prospects, ARES provides a more compelling combination of growth and income.

Therefore, despite its premium valuation, Ares Management appears better positioned to deliver attractive long-term shareholder returns, making it the more favorable choice for investors seeking both growth and income.

ARES and KKR currently carry a Zacks Rank #3 (Hold) each. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA’s enormous potential back in 2016. Now, he has keyed in on what could be “the next big thing” in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

This article originally published on Zacks Investment Research (zacks.com).