June 15, 2026

Senior Portfolio Strategist

Fixed Income Strategies

Portfolio Advisory Group–U.S.

Key points

-

Geopolitical events drove global bond yields higher in the first half

of the year, but this latest leg higher only continues a much broader

trend that has been in place for years. -

Markets have repriced modest central bank rate hikes ahead, but the

reaction in longer-dated bond yields has been more significant,

suggesting bigger factors are at play. We see higher government bond

yields ahead. -

Despite higher yields on offer, bond markets have struggled to perform

this year, which we expect to continue into year-end. We believe

investors should focus on coupon income as bond price appreciation due

to lower yields should remain elusive.

At the halfway point of 2026, global bond markets are lagging the already

low expectations we held at the start of the year. Not only have many

major global bonds failed to earn their coupons, rising bond yields – which

move inversely to bond prices – have pressured prices lower to such a degree

that declines have more than offset coupons earned, putting total return

performance modestly in the red year-to-date.

A simple explanation would be that the unexpected war in the Middle East

and the subsequent jump in oil prices, along with another round of supply

chain disruptions, have caused a temporary spike in inflation, central

bank rate hike expectations, and bond yields. There’s a sense then that

these moves could be unwound just as quickly as they appeared if/when

there’s a resolution to the conflict. But we think that could be too

simple, and perhaps too myopic.

While the Middle East conflict is no small issue, we do see it as just

another tree in a forest of reasons that has pressured global yields

higher not just this year, but for many years running at this point.

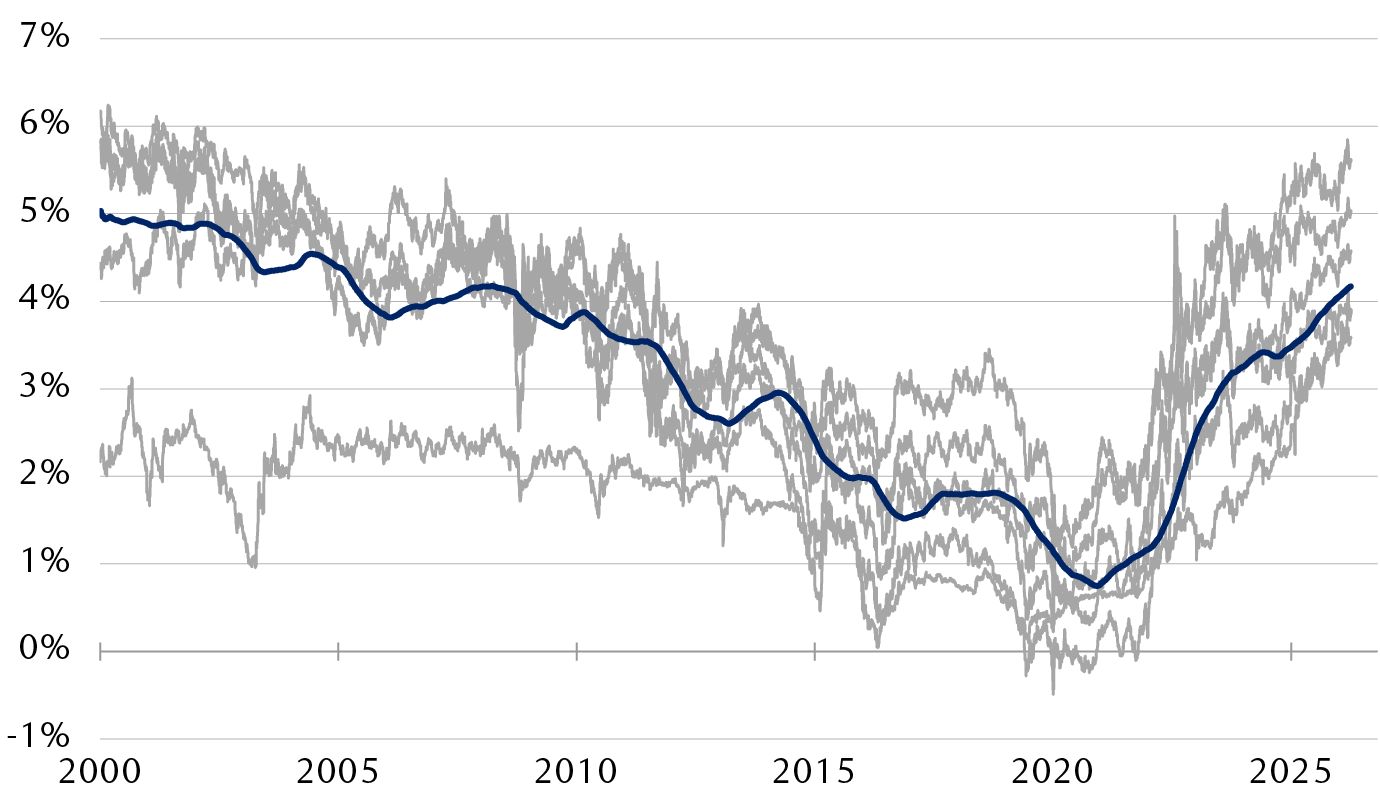

The chart below stylizes just that. The gray lines represent the 30-year

government bond yields of the U.S., Canada, Germany, Japan, France, and

the UK. Which is which doesn’t matter, and that’s the point – nearly all are

at or near 20-year highs, while the simple average yield of the group has

breached 4.0 percent for the first time since early 2009.

The forest of global 30-year sovereign bond yields shows a rising trend

with no signs of slowing

30Y bond yields of Canada, U.S., UK, Germany, Japan, and France

-

Average of 30-year global sovereign bond yields

Source – RBC Wealth Management, Bloomberg

The chart shows key 10-year government bond yields from major regions

against the simple average of the group on a rolling one-year basis.

That average now stands at 4.2%, up from just 0.8% in 2021.

Oil prices and central bank rate hike fears are dominating the narrative

at the moment, but we think markets are pricing a bigger confluence of

factors as driving these trends, and these factors largely continue to

point in the same direction – higher yields still.

Everything costs more, including money

So, as we take stock of the first half of 2026, and what we might expect

for the rest of the year, we can’t help but feel the desire to take an

even bigger step back.

The technology hyperscalers are issuing massive amounts of debt and equity

to raise funds for the ongoing AI buildout. Governments, not to state the

obvious, continue to issue massive amounts of debt to fund ongoing

deficits, and defence costs for certain regions are only likely to

compound those deficits. The demand for capital amid a global economic

backdrop that remains steady is increasingly overwhelming the supply of

capital, as savings rates decline and aging populations pivot from saving

money to spending it.

Where might it end? We would concede that we don’t have a high-conviction

view on that front. We had anticipated a return to pre-global financial

crisis levels – which appears to be where we are now. A return to pre-2000

yield levels of five percent to six percent appears increasingly likely as

the tech boom of today seems at least comparable to the tech boom of the

1990s, propelling near-term economic growth and inflationary pressures

higher.

Central banks ready a response

For all the hyperfocus of late on central banks and the potential for rate

hikes, we think any adjustments will be both modest in nature and little

more than necessary recalibrations to economic realities on the ground.

Single-mandate banks such as the European Central Bank (ECB) and the Bank

of England (BoE), which target only price stability, will need to act

sooner rather than later, while others have more time to gauge the impact

on economic growth, labour markets, and inflation in their totality.

Federal Reserve and Treasury yields

-

Our base case is that the Fed keeps rates on hold through 2026 and 2027,

but with a bias toward rate hikes. Though markets are pricing a 100

percent chance of a rate hike this year, we would highlight that they

are giving the Fed a longer runway for potential action than other

central banks, as market-implied prospects don’t exceed the key level of

80 percent until the Fed’s December meeting. -

With respect to the benchmark 10-year Treasury yield, on balance we

expect it to hold at current levels around 4.50 percent, but with an

upward bias. Importantly, we do see scope for it to test key technical

levels of this cycle: 4.80 percent in 2025 and 5.0 percent from 2023.

European Central Bank and German Bund yields

-

The ECB was the first G7 central bank to raise rates this year at its

June 11 meeting, and we see two more 25 basis point rate hikes in the

pipeline this year before the ECB likely holds at a policy rate of 2.75

percent into 2027. -

The German Bund yield broke above 3.0 percent following the onset of the

Middle East conflict and has largely held that level since. Our forecast

has it rising modestly toward 3.25 percent this year, and to 3.40

percent in 2027.

Bank of England & Gilt yields

-

After the ECB, we think the BoE will likely be the next to act with a

singular rate hike at its September meeting to 4.0 percent before

pausing through 2027. -

Despite a modest BoE rate outlook, the 10-year Gilt yield has been

highly volatile this year, trading as low as 4.2 percent and as high as

5.2 percent. For now, we see it steadying around 5.0 percent through

year-end.

Bank of Canada and Government of Canada yields

-

The Bank of Canada (BoC) is stuck between weak economic growth and

rising price pressures. But like the Fed, we think the BoC will remain

on hold this year, with potential hikes in early 2027. -

The benchmark 10-year Government of Canada yield has averaged 3.4

percent over the past year, is currently trading around 3.5 percent, and

we see it only rising toward 3.6 percent by year-end.

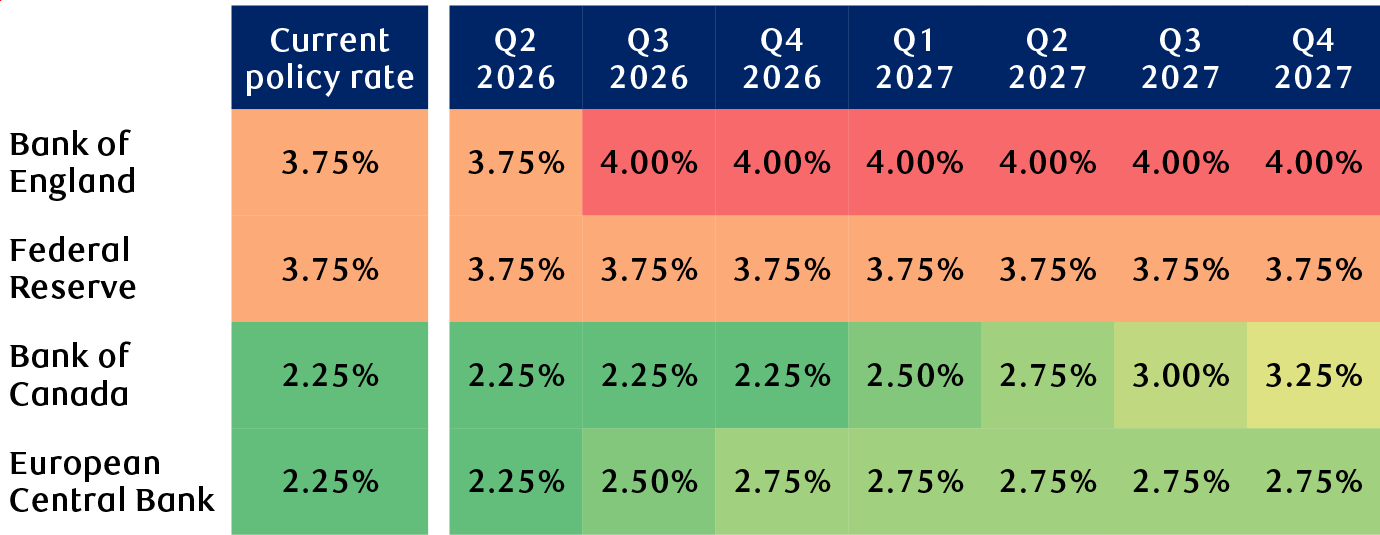

Current RBC central bank rate projections

Source – RBC Wealth Management, RBC Capital Markets

The chart shows the current policy rates and future quarterly

projections through 2027 for the Bank of England, U.S. Federal

Reserve, Bank of Canada, and European Central Bank. The United Kingdom

and the U.S. policy rates are at 3.75%, while Europe and Canada are at

2.25%. The UK is projected to raise its rate to 4.00% by the end of

2027, and the U.S. is projected to keep its rate steady. Canada is

projected to raise to 3.25%. Europe is projected to raise to 2.75%.

Chopping wood

While bond markets focus on the forest of interest rate dynamics,

individual bond investors need to know which trees to chop down for yield.

Despite rising yields, and to what are certainly historically attractive

levels, we still expect a somewhat challenging landscape for bond

investors. Given that we see little scope for sovereign bond yields to

move materially lower absent economic downturns, investors should simply

aim to maximize income, as bond price appreciation on top of coupons could

remain elusive.

Global corporate bonds present just 0.76 percent of incremental yield over

their government bond peers for potential credit and default risks. While

not quite as low as the lowest lows of 2005 (+0.55 percent), the margin

for error is clearly miniscule.

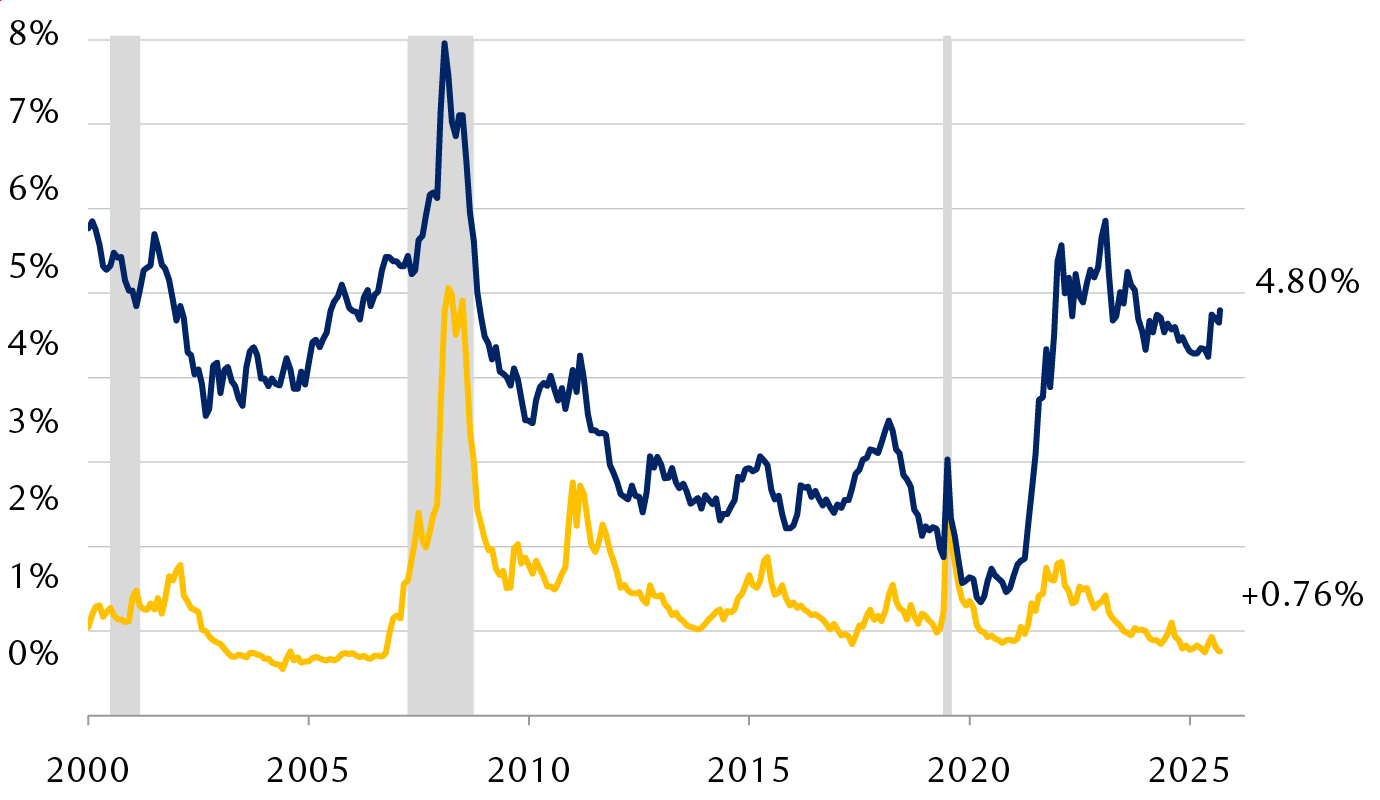

Global corporate bonds offer plenty of yield, but little excess yield for

potential credit risks

-

U.S. recessions

-

Index credit spread

-

Index yield

Source – RBC Wealth Management, Bloomberg Global Aggregate Corporate

Bond Index

The chart shows the average yield of the Bloomberg Global Aggregate

Corporate Bond Index relative to the average credit spread, or

incremental yield over comparable government bond yields, for implied

corporate credit risks. Both the index credit spread and the index

yield rose significantly during the 2008 financial crisis and again

during the 2020 U.S. recession. The index yield rose sharply in 2021

and remains high relative to the credit spread, at 4.80% vs. roughly

+0.76%.

Therefore, we hold a cautious outlook on credit, but absent a recession

the asset class should perform reasonably well, and at the end of the day,

extra yield is extra yield. There’s also the not-so-tongue-in-cheek idea

that corporate balance sheets might look healthier than government balance

sheets.

The material herein is for informational purposes only and is not directed at, nor intended for distribution to or use by, any person or entity in any country where such distribution or use would be contrary to law or regulation or which would subject Royal Bank of Canada or its subsidiaries or constituent business units (including RBC Wealth Management) to any licensing or registration requirement within such country.

This is not intended to be either a specific offer by any Royal Bank of Canada entity to sell or provide, or a specific invitation to apply for, any particular financial account, product or service. Royal Bank of Canada does not offer accounts, products or services in jurisdictions where it is not permitted to do so, and therefore the RBC Wealth Management business is not available in all countries or markets.

The information contained herein is general in nature and is not intended, and should not be construed, as professional advice or opinion provided to the user, nor as a recommendation of any particular approach. Nothing in this material constitutes legal, accounting or tax advice and you are advised to seek independent legal, tax and accounting advice prior to acting upon anything contained in this material. Interest rates, market conditions, tax and legal rules and other important factors which will be pertinent to your circumstances are subject to change. This material does not purport to be a complete statement of the approaches or steps that may be appropriate for the user, does not take into account the user’s specific investment objectives or risk tolerance and is not intended to be an invitation to effect a securities transaction or to otherwise participate in any investment service.

To the full extent permitted by law neither RBC Wealth Management nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct or consequential loss arising from any use of this document or the information contained herein. No matter contained in this material may be reproduced or copied by any means without the prior consent of RBC Wealth Management. RBC Wealth Management is the global brand name to describe the wealth management business of the Royal Bank of Canada and its affiliates and branches, including, RBC Investment Services (Asia) Limited, Royal Bank of Canada, Hong Kong Branch, and the Royal Bank of Canada, Singapore Branch. Additional information available upon request.

Royal Bank of Canada is duly established under the Bank Act (Canada), which provides limited liability for shareholders.

® Registered trademark of Royal Bank of Canada. Used under license. RBC Wealth Management is a registered trademark of Royal Bank of Canada. Used under license. Copyright © Royal Bank of Canada 2026. All rights reserved.

Senior Portfolio Strategist

Fixed Income Strategies

Portfolio Advisory Group–U.S.