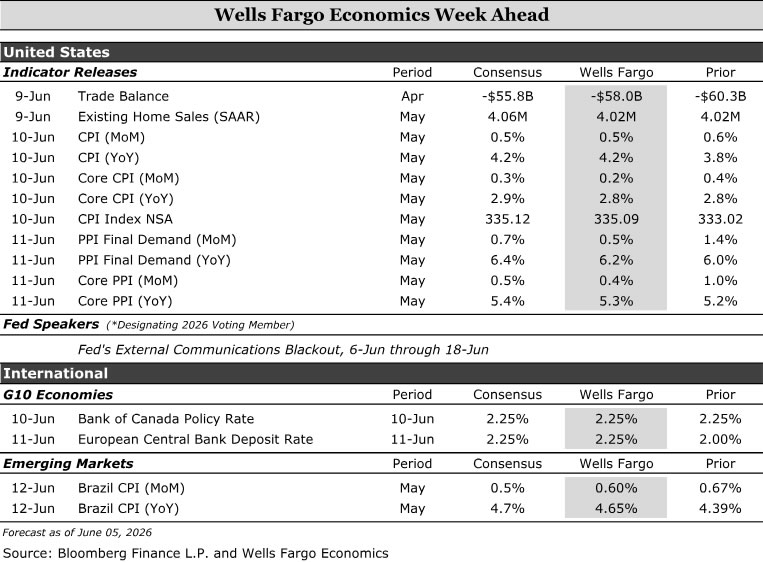

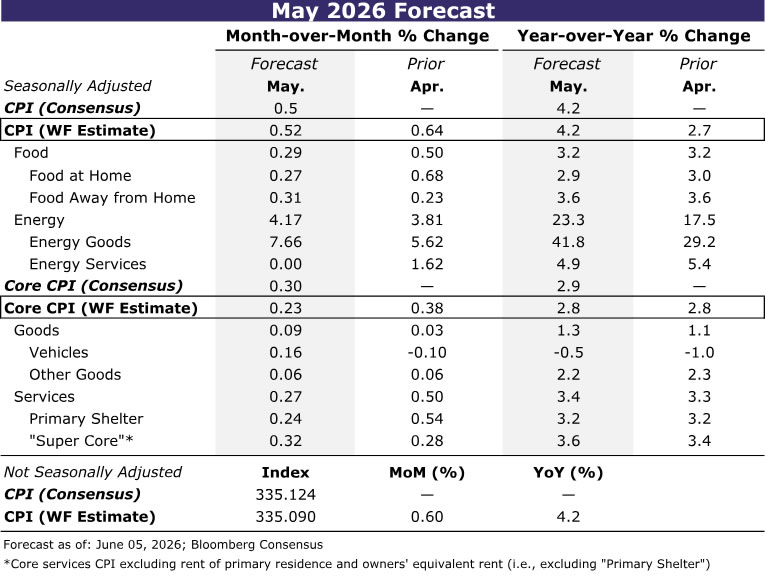

U.S. inflation is showing renewed upward pressure, with our expectations for May CPI to rise 0.5% and the year‑over‑year rate pushing to 4.2%, largely driven by an 8% surge in energy goods and firmer food prices. We believe core inflation will be 0.2% as goods stabilize and services stay broadly steady outside of pockets like airfares. In the Eurozone, inflation is broadening more decisively, with high three‑month annualized rates and firming pressures across both services and goods likely prompting the ECB to begin a tightening cycle, starting with a 25bp hike and maintaining a hawkish bias. In Canada, the Bank of Canada is likely to hold rates at 2.25% in the near term, balancing softer recent growth and core inflation against still supportive commodity dynamics and tight labor supply, leaving the policy path tilted toward gradual future hikes. In Brazil, inflation is moving further above target, with our expectations for headline nearing 4.7% as price pressures shift from energy toward food, complicating the outlook and raising the likelihood that easing gives way to a pause as inflation risks intensify.

United States:

G10 Economies:

- ECB Policy Rate (Thursday), Bank of Canada Policy Rate (Wednesday)

Emerging Markets:

U.S. Week Ahead

CPI • Wednesday

The inflationary effects of the Iran conflict continue to ripple through consumer prices. We estimate the Consumer Price Index rose 0.52% in May, which would push the year-over-year rate up to a three-year high of 4.2%. Higher costs of necessities continue to pinch consumers. We estimate energy goods (primarily gasoline) rose 8% in May, while food prices advanced 0.3%.

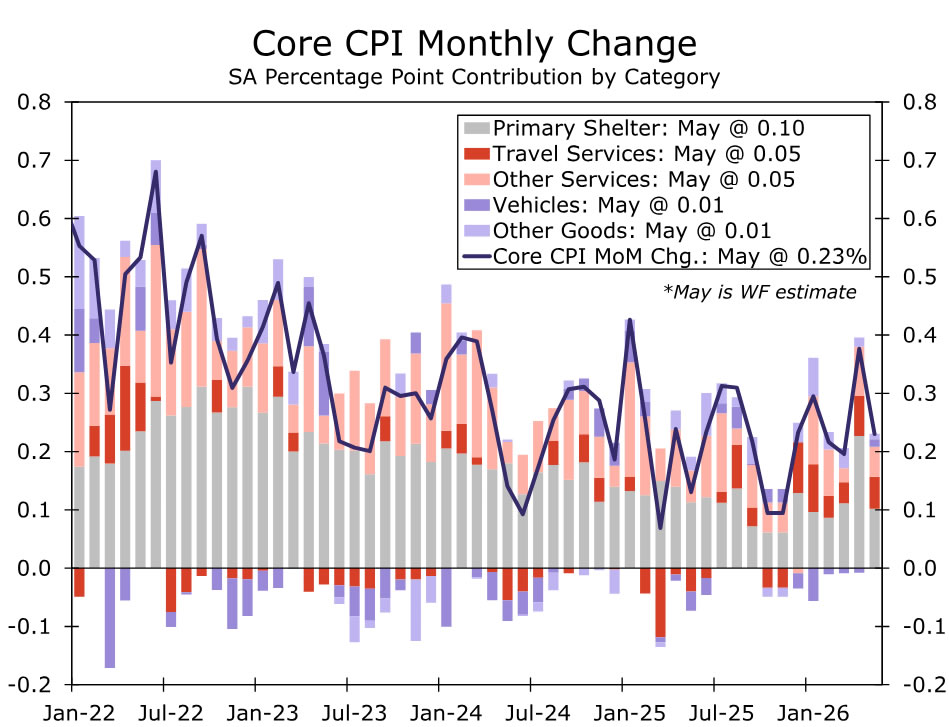

Excluding food and energy, we estimate prices rose a more moderate 0.23%. Core good prices look set for a modest pickup in May thanks to a lift from used autos, as the CPI index has yet to reflect the pickup in wholesale auction prices since the start of the year. Inflation among other goods, however, is likely to have eased slightly as tariff-related price hikes ebb and the Iran conflict’s second-round effects on costs for transportation, packaging, etc. are slow to filter into retail prices.

One area of the core in which the impact of the Iran conflict should be readily apparent though is airline fares. The surge in jet fuel costs since early March along with the bankruptcy of Spirit Airline’s set the stage for another solid rise (we’ve penciled in an increase of 3%). But we do not expect to see a broad re-acceleration in price growth across remaining services. Primary shelter looks to set to revert to its 0.2-0.3% monthly pace following April’s “catch up” reading that was a lingering quirk of the government not collecting data last October during the shutdown. Meantime, a rebound in medical care is likely to be mostly offset by weakness in motor vehicle insurance and personal services, keeping the six-month pace of core services ex-shelter and travel unchanged at 2.5% and in line with its pre-COVID pace.

G10 Week Ahead

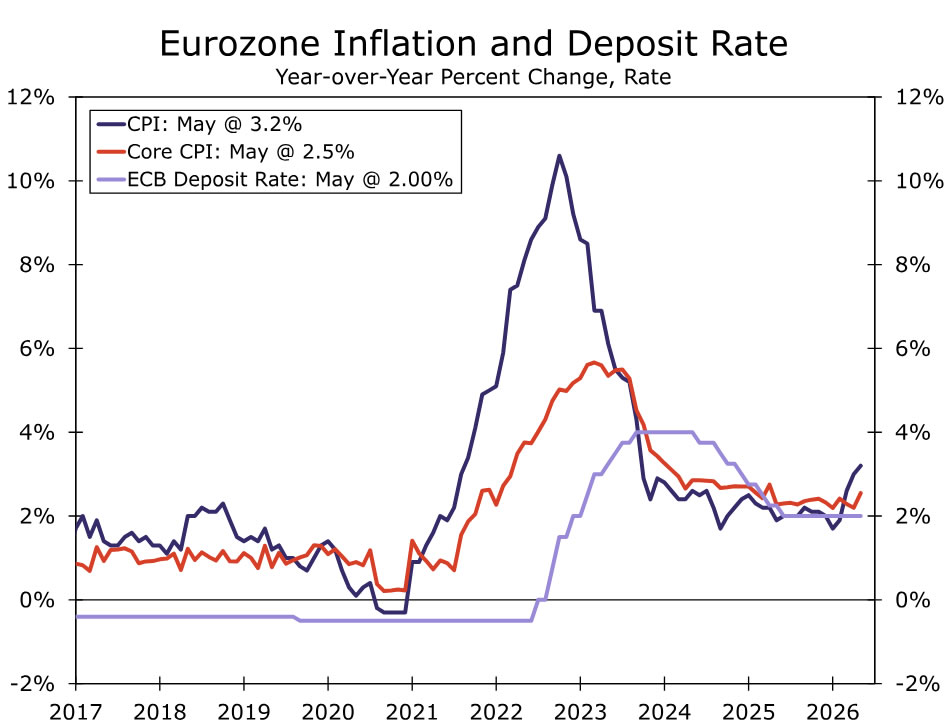

ECB Monetary Policy Meeting • Thursday

We expect the ECB to hike rates by 25bp next week, taking the deposit rate to 2.25% and the main refinancing rate to 2.40%. The macro backdrop has evolved broadly in line with the ECB’s March adverse scenario. Shipping disruptions persist, energy inventories are being drawn down, and prices remain elevated despite ongoing volatility. The May flash CPI reinforces the inflation story, pointing to both acceleration and broadening pressures. Three‑month annualized headline and core inflation now stand at 9.6% and 8%, respectively, well above the 3.2% and 2.5% year‑over‑year rates. Beyond energy, price pressures have firmed across services and non‑energy industrial goods over the past 3 months.

Against this backdrop, we expect a hawkish signal from the ECB, emphasizing the need to cool demand to limit second‑round effects. This should be reflected in updated staff projections and refreshed scenario analysis, likely incorporating more severe assumptions given that the previous adverse scenario now resembles the baseline. June should mark the start of the hiking cycle, with at least one additional move in Q3, likely in July.

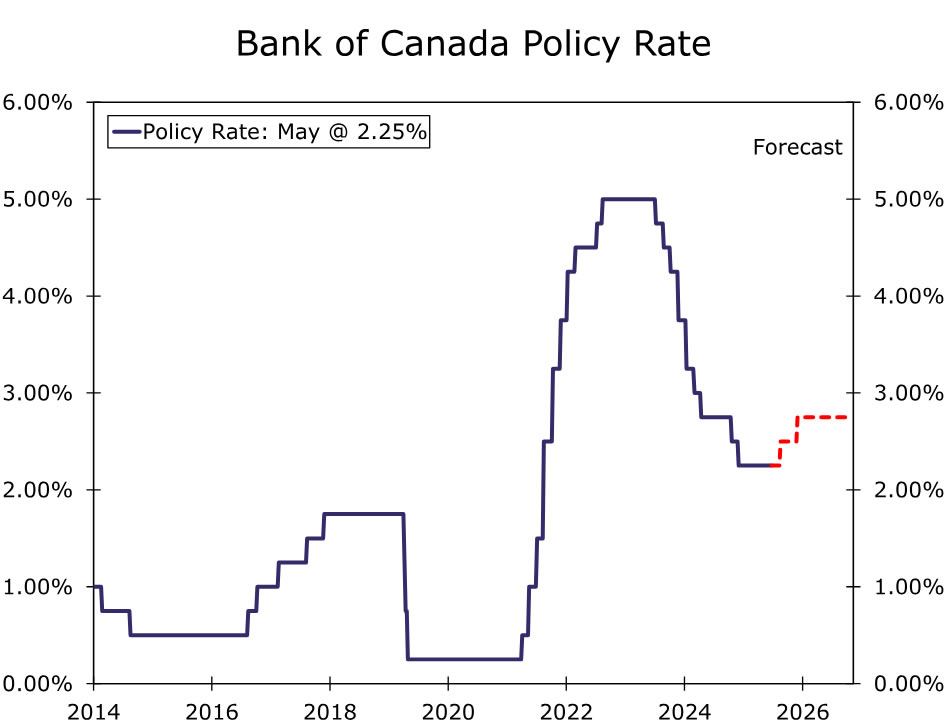

Bank of Canada Monetary Policy Meeting • Wednesday

We expect the BoC to remain on hold next week, keeping the policy rate at 2.25%. Our baseline expectation remains for a July hike, although our conviction has declined with the weaker‑than‑expected Q1 GDP print and near‑term softness in core inflation. We continue to expect an additional hike in Q4, leaving the policy path biased toward higher rates over the coming months.

Elevated energy and commodity prices should act as an inflationary tailwind for Canada, supporting both consumer demand and labor markets through resource‑linked activity. At the same time, labor supply constraints remain binding. An aging workforce and softer immigration flows continue to weigh on participation, likely keeping the unemployment rate low and underpinning wage growth. In this context, we see core inflation as having bottomed, with risks tilted to the upside.

The July 1 USMCA review looms large. Our baseline assumes a shift to an annual review process within the existing framework. This extends medium‑term uncertainty and may weigh on business investment, but preserves low‑tariff access and limits the near‑term economic impact.

EM Week Ahead

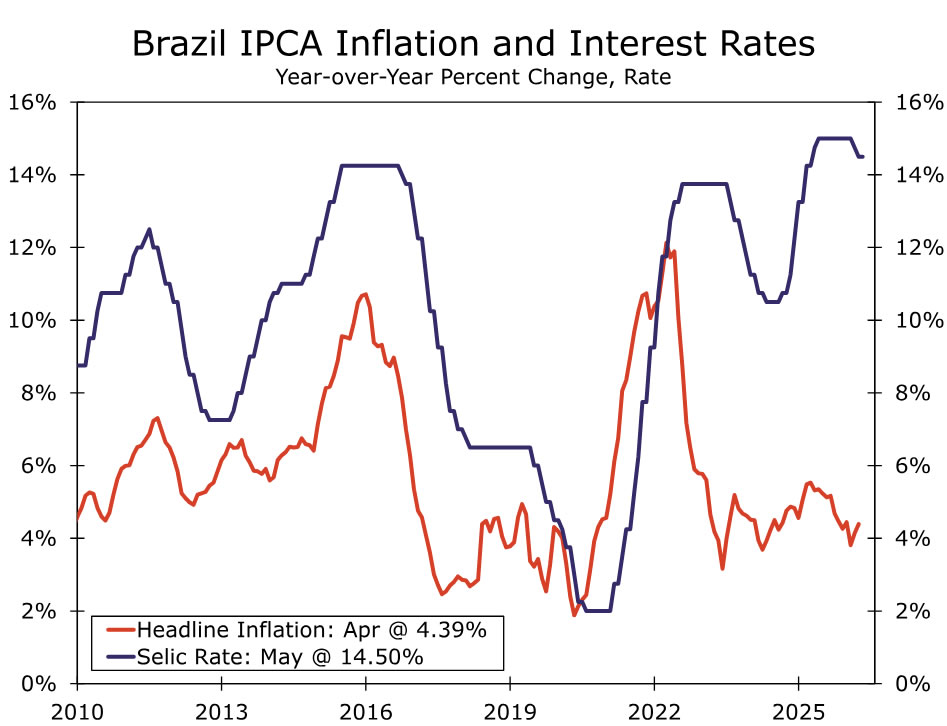

Brazil May CPI • Friday

We look for May IPCA inflation to accelerate to 4.65% y/y from 4.39%, moving above the upper bound of the BCB’s 4.5% target band. While m/m inflation likely moderates to 0.6% from 0.67%, the broader inflation outlook remains firmly skewed to the upside.

Global supply chain disruptions are set to persist, with price pressures likely rotating from energy toward food in the coming months. This is particularly relevant for Brazil, where food carries a higher weight in the CPI basket than in advanced economies. At the same time, we expect fiscal policy to continue supporting demand, partially offsetting the drag from eroding real incomes and tighter monetary conditions. The policy mix is likely to remain pro‑growth, especially in an election year.

Rising US‑Brazil tensions may further bolster Lula’s political support, potentially providing cover for additional populist measures. Against this backdrop, while we expect the BCB to deliver a rate cut in June, we see scope for a pause in Q3 as inflation dynamics deteriorate and external and domestic pressures intensify.