- Equities are signaling optimism while households are signaling strain. That divide matters because investors and consumers are pulling in different directions. The path of energy prices matters too.

- The municipal bond market is impacted by both. It is helping to finance the infrastructure behind the next economy, while investors are still relying on the credit strength of the current economy.

- This is why municipals still offer opportunities, but also why credit selection matters more than it did when the backdrop was easier to read, and the divide was narrower.

Sentiment, S&P 500, AI, Oil Shock

This is a harder market to read than the headline indices suggest. Stocks are pushing to new highs, household sentiment is scraping record lows, oil related risk remains unresolved, and the municipal bond market sits in the middle of all of it. There is opportunity in municipals, but it must be understood in the context of a broader economy that is sending mixed and increasingly divergent signals. Overall, this is a modestly challenging market to read, but there are opportunities.

The difficulty in reading the signals around the market is not just because of volatility. The difficulty is in the many contradictions that exist now. Heavy technology spending is still supporting growth, equity investors remain highly optimistic, geopolitical risk continues to move in and out of focus, and consumers are telling us they feel materially worse. For municipal investors, the opening remains in still-attractive, even generationally attractive, yields and a credit backdrop that is holding, even as it softens at the margin.

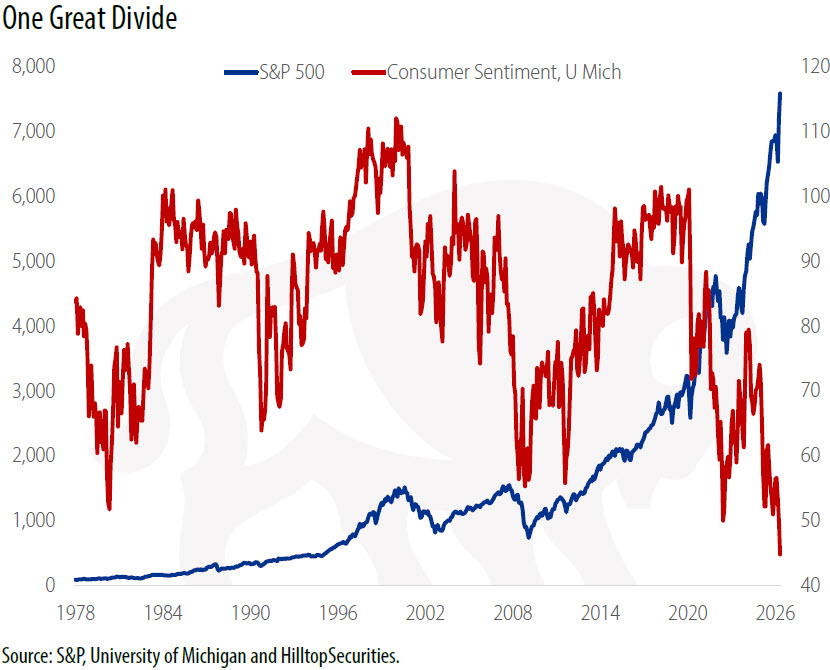

Our line chart, found on the first page, captures two very different readings of what is happening in America. One line, the S&P 500 Index, is moving toward record highs and signaling confidence in a more productive and profitable future economy, driven in large part by technology spending and the expected gains from artificial intelligence.

Technology spending is still doing a great deal of the work in the broader economy. First quarter 2026 GDP was revised down to 1.6% from 2.0%, but that was still an improvement from the 0.5% growth rate in the fourth quarter of 2025. Recent data releases also point to some softening, as HilltopSecurities’ Scott McIntyre also detailed at the end of last week.

The other line in our chart on page one shows consumer sentiment falling to record lows. It is telling us that households still feel pinned down by the cost of groceries, insurance, housing, fuel, and borrowing, with little confidence that relief is close. The University of Michigan’s final May reading fell to 44.8, a record low, as higher costs and the risk of further energy-driven inflation remained front and center. Equity investors are pricing in transformation. Households, still struggling with inflation on the ground in their day-to-day activity, are trying to figure out how to pay for the present. That divide between market confidence and household confidence deserves close attention because it tells us who or which side is actually feeling the expansion and which side is not.

There is another divide that matters. It is the widening gap between diplomatic rhetoric and operating reality in the Middle East. The concern has bounced around for weeks. Even if talks continue in process, they may still fail to produce what markets need, which is a durable reopening of the Strait of Hormuz. If that does not happen, oil prices could remain under upward pressure for longer than many investors expect.

By the middle of last week, more market participants were openly questioning whether the Strait of Hormuz would reopen anytime soon, with the obvious implication that oil prices could stay elevated. Walter Kunisch and I discussed that energy risk in our recent Hilltop Talks podcast, The Oil Shock and the New Energy Reality.

Brookings highlighted the issue also in The timing of the impending crude crisis, writing that “the supply shortfall will build in coming months as temporary buffers are depleted” and that oil prices may rise materially higher if markets grow more pessimistic about a resolution. On Monday, President Trump also said he did not care if Iran negotiations were over, a reminder that policy signaling and market reassurance are no substitute for an operational outcome.

The municipal bond market straddles both divides. It is helping finance the infrastructure required for an AI-driven economy, including public power, water and sewer systems, K-12 schools, public safety, and the basic operating backbone of communities across the country. But the credit quality municipal investors rely on is still rooted in present conditions. It depends on property tax bases that are generally still holding up, household income that is still broadly supportive, and public sector discipline that we continue to watch closely.

For municipal investors, we continue to see opportunity in solid credit quality. But, as we wrote a few weeks ago, credit selection matters more because these divides and structural pressures are no longer abstract. They are beginning to show up in borrower differentiation. Demand for municipals still looks like the defining story of 2026, as we argued last week in Investors are Choosing Stability, Tax-Exempt Income, and the Bonds that Finance America’s Infrastructure. The day after that report was published, another $2.3 billion flowed into municipal mutual funds, reinforcing the view that the drivers of demand remain durable in the near term. Attractive municipal yields are still here. They may not stay this attractive indefinitely.

Readers may view all of the HilltopSecurities Municipal Commentary here.

About Tom Kozlik

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or [email protected].

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or [email protected].

Learn more about HilltopSecurities.