Ignorance is bliss.

Awareness is a curse.

Also, we do not think (no thanks partly to AI) that many read beyond the headlines.

Especially, when it comes to what is happening in the world of private credit and how the banks are interconnected, almost everyone is in a total blissful state.

For those who still choose to read for the sake of knowledge and awareness, here you go. This is a big read. So, grab a coffee or wine. We are writing this to CI members and our clients. Well, because we care and we think it is critical to understand the interconnected nature of the economic mess we are in. So one could invest responsibly on the short/long side.

We are seeing three converging signals in May 2026 that confirm that bank exposure to private credit is now globally interconnected through warehouse lending, NAV loans, and synthetic risk transfers, and is materially larger than the official “limited direct exposure” framing allows for.

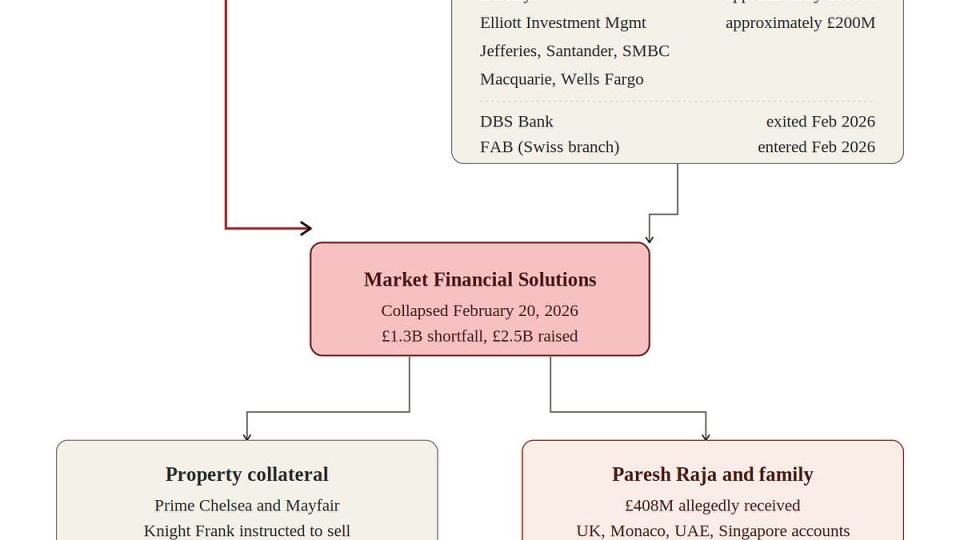

The Market Financial Solutions (MFS) collapse cost HSBC roughly $400 million via an Apollo-affiliated warehouse, drew in DBS Bank of Singapore and First Abu Dhabi Bank in the UAE, and exposed Barclays, Jefferies, Elliott, Santander, Sumitomo Mitsui, Macquarie, and Wells Fargo. We broke the news about MFS before the mainstream media. Here is our initial analysis. As we continue to say, Tricolor, First Brands, and MFS – none of them are isolated.

JPMorgan is in discussions to offload first-loss risk on a $4 billion NAV loan pool to private equity funds. The Significant Risk Transfer (SRT) market has scaled past $1 trillion in cumulative hedged assets. The ECB confirmed in its May 27, 2026, Financial Stability Review that insurers, not banks, are the entity most exposed to a private credit shock in Europe. Each of these data points was knowable independently. Their convergence is what is new now.

This article walks through the cascading impact. We document the direct channels (warehouse lending, NAV loans, SRTs), the indirect channels (life insurer private placements, affiliated issuance, reinsurance), and the second- and third-order pathways through which a default at a single non-bank lender now reaches global G-SIB balance sheets within weeks. We map US and European exposure using primary regulatory data where possible. We close with a candid view on what could stop the funding crack, who will be impacted, and why the prevailing official line that direct bank exposure is limited misses the point.

This is for Confidential Insights Members Only.