Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

There’s a strange kind of double counting that’s unique to commodity markets. The closure of the Strait of Hormuz means oil exports out of the Persian Gulf – including what goes through Saudi Arabia’s pipeline to the Red Sea – are running at roughly half their ordinary capacity. This has many folks worried because they think this “physical” shortage will now push prices up a lot. But this kind of logic ignores that markets are forward-looking. Oil prices have risen substantially from before the war, presumably in anticipation of exactly the physical shortages we see now. So when folks talk about how prices need to rise, they’re double counting. This is why I’ve been arguing that $150 or even $200 are unrealistic, including on the podcast with Paul Krugman that aired on March 21.

Given all the chatter about physical scarcity, today’s post revisits my piece from back in March on why oil prices aren’t going inexorably higher. I then fold that into what global growth looks like. I’m more bullish than consensus on the US, but I’m worried about Europe and parts of Asia (not China given its huge stockpiles of crude).

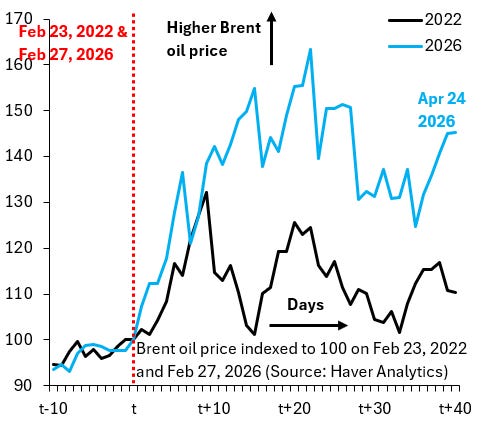

When I first started arguing that oil prices wouldn’t go to $150 or $200, I made two basic points. The first compared the current shock to Russia’s invasion of Ukraine. Russia exports around seven million barrels per day. In normal times, about twenty million barrels transit the Strait of Hormuz daily. This means the current shock is about three times as important as Ukraine for global oil markets and – as the chart above shows – this is pretty much what markets price for Brent, which is up around fifty percent from before the war (blue line) versus ten percent on a comparable time scale back in 2022 (black line). If anything, the rise in oil prices looks a bit much.

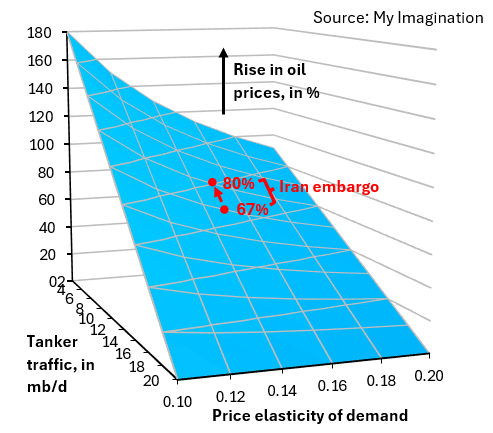

The second point maps the physical shortfall into prices for a reasonable range of the price elasticity of demand. The chart above gives volumes out of the Persian Gulf on the axis going away from the reader, where the shortfall rises as you move off into the distance, and a range from 0.10 to 0.20 for the price elasticity on the horizontal axis, where I think the midpoint of this range – 0.15 – is the safest bet. If we assume that volumes out of the Gulf are at half their pre-war capacity, this means oil prices should rise 67 percent. If we assume the Iran blockade has cut exports out of the Gulf a bit more, then oil prices need to rise 80 percent. All in all, factoring in that Asian prices have risen a lot more than Brent or WTI, we’re basically there. The “physical” shortage everyone’s talking about got priced long ago.

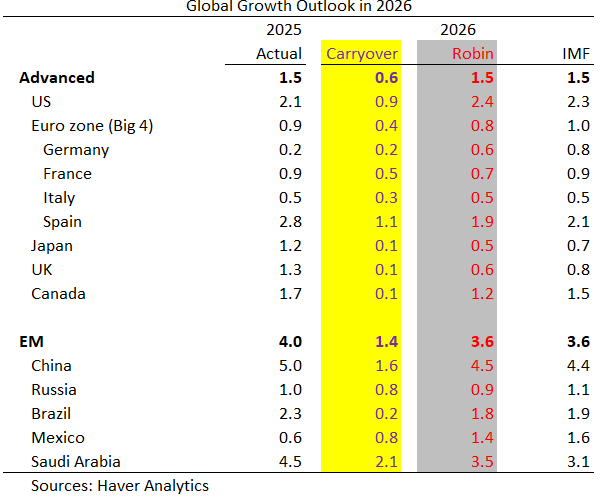

What does all this mean for global growth? The table above shows a selection of G10 countries and emerging markets, where I’ve averaged these up into an “advanced” and “emerging markets” (EM) category using PPP weights from the IMF’s World Economic Outlook. The first column shows annual average growth in 2025. The second column shows statistical carryover from 2025 into 2026. This might sound nerdy, but it’s really important. This is what growth would be in 2026 if GDP flatlines, i.e. doesn’t grow at all beyond Q4 2025. Countries that had strong growth in the course of 2025 will have high carryover, which is just a mathematical construct and not really growth. So you want to compare the third column (in gray) – my growth forecasts – to the second (in yellow). A strong growth picture must have projected growth substantially above carryover. If that isn’t the case, GDP is flatlining. The last column is the IMF’s forecasts from a few weeks ago for reference.

My headline numbers are similar to the IMF, but the composition is different. I’m more optimistic on the US, because the shock is still comparatively mild here, while I’m more pessimistic on Europe, where physical shortage of refined product is looking acute. I’m more optimistic on China because of its large stockpiles of crude and huge refining capacity, but more pessimistic for much of the rest of EM. If we get a peace deal over the weekend, these numbers will have to get revised up for the US. If the closure of the Strait drags on, there’s a bit of downside risk across the board.