On April 8, 2026, we published Blackstone’s Defense of Private Credit. There is a Problem with Its Defense. In it, Blackstone argued that concerns about BDCs are overblown, that credit quality is resilient, that the semi-liquid structure works as designed, and that software exposure is well protected.

Well, last week we reviewed the loan book. BCRED, Blackstone’s $45 billion credit machine, prorated redemptions for the first time in its history. We read all 859 pages of its latest filings and parsed all 1,288 positions in its investment schedule to find out why.

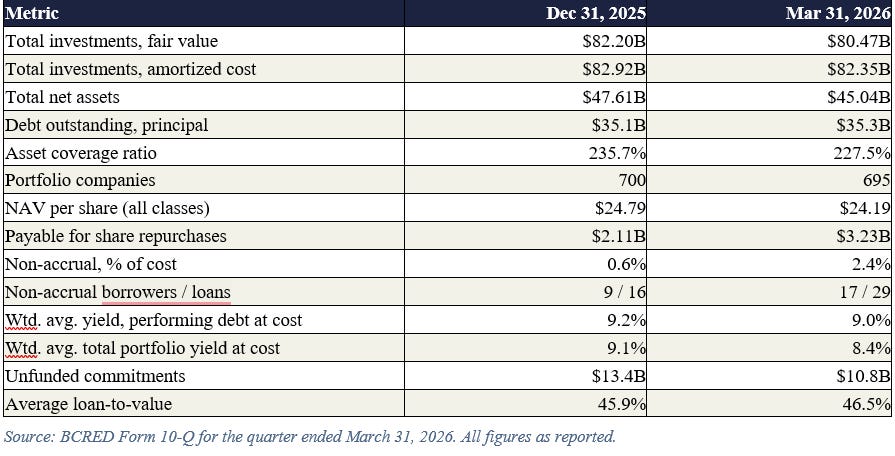

Five years ago, Blackstone launched a fund that let ordinary investors do what banks do: lend money to hundreds of American companies and collect the interest. It worked spectacularly as a fundraise. BCRED became the largest fund of its kind on earth, with $80 billion in loans to 695 companies, funded by $45 billion in shareholder capital and $35 billion in debt.

Then, this spring, the shareholders started asking for their money back. In the first quarter of 2026, they tendered 7% of the fund. The Board lifted its own 5% quarterly cap to pay everyone in full, $3.2 billion out the door, and Blackstone and its employees put their own money into the fund to help meet the wave; press reports of how much range from $150 million (CNBC) to roughly $400 million (AltsWire), and the fund itself has quantified it nowhere. One quarter later, requests hit 10%. This time the fund held the line at 5% and, for the first time ever, told the other half to get back in the queue.

The filings behind that decision are the most revealing documents the private credit boom has produced so far, and we went through them line by line. A few of the things sitting in there:

The fund’s biggest exposure to any single company is not a private equity buyout. It is $1.6 billion across two loans to Dropbox, a publicly traded company, under a facility that Dropbox itself said could fund its stock buybacks. While BCRED’s own investors were pulling $3.2 billion this quarter, the fund funded roughly $870 million of additional Dropbox draws, because it had promised to.

The share of the portfolio that has stopped paying quadrupled in a single quarter, from 0.6% to 2.4% of cost, as the borrower count nearly doubled from 9 to 17. One of them, a software company called Medallia, is carried at 62 cents on the dollar of its cost, and the recapitalization its lenders signed in June is set to wipe out roughly $5 billion of Thoma Bravo’s equity in one of the largest private credit restructurings ever. BCRED is the biggest BDC holder of its debt.

The fund earned $0.54 a share this quarter. Markdowns took back $0.54. It paid a $0.60 distribution anyway.

Nearly a third of the borrower names in the loan book are not operating businesses. They are shells: Bidco, BorrowerCo, Purchaser, Topco. And nested inside the fund, off its balance sheet, is a second loan fund, levered at roughly 2.6 times, with a bad-loan rate already double the parent’s.

The full report traces who actually borrowed the $80 billion, sector by sector and name by name, and works through the question nobody in this market wants asked out loud: what does this fund’s NAV look like when the new money stops coming in, and what happens to 695 companies, and their employees, when the lender they built their balance sheets around goes into run-off?

The numbers are not reassuring, and it probably applies to every one of BCRED’s peers. We know, because we have already dissected them: Apollo’s ADS, Cliffwater’s CCLFX, now, BCRED.