Hedge funds are not abandoning risk; they are abandoning the easy version of it. Index and ETF exposure is holding up while single-stock longs, especially in technology, are being cut back.

The AI trade has moved from a one-way beta chase into a stock-picker’s market. Semis, memory and hardware remain central to the story, but crowded ownership has made the path far less forgiving.

Japan’s record sell flow and Korea’s reversal of year-to-date buying show that Asia’s strongest trades are now being actively harvested, not simply admired from afar.

Goldman’s client base remains modestly bullish on risky assets, but the preference for developed-market equities over credit says it clearly: investors still want upside, just not the kind that leaves no margin for a wobble.

The boom is still alive. But the market is beginning to ask the question it avoided during the easy phase: who can actually turn investment into earnings, and who was merely standing near the fireworks?

How hedge funds started July

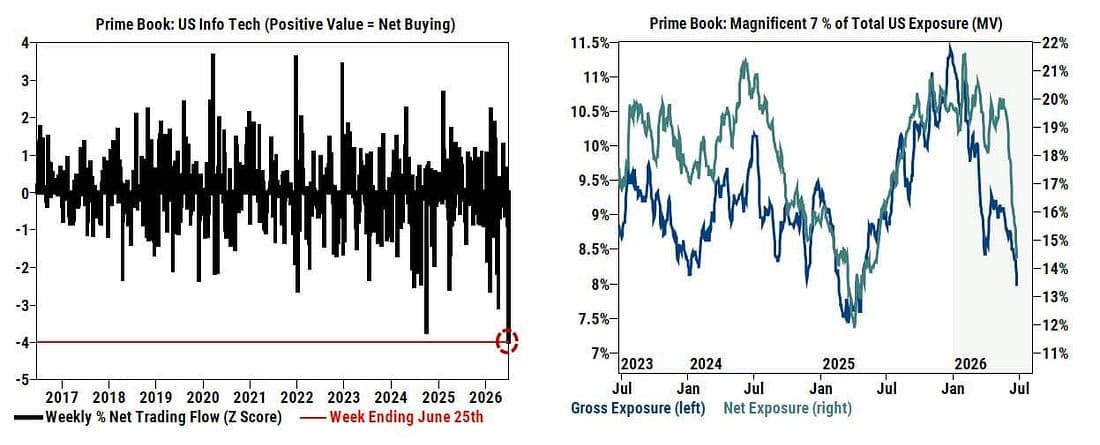

A week ago, Goldman Sachs Prime Brokerage was already flagging a remarkable retreat from technology: hedge funds had sold the sector at a record pace just ahead of the Russell rebalance, when outsized index-related flows threatened to turn an ordinary adjustment into a much louder event. The result was a sharp reduction in both gross and net exposure to the Magnificent Seven, pushing positioning to its lowest point of the year.

The important point is that this was not simply a bearish macro call on US equities. It looked more like risk managers taking some furniture out of the room before the crowd arrived. When rebalancing volumes are set to explode, crowded winners become vulnerable not only to fresh fundamental doubts but also to the mechanical need to cut, hedge, and rebalance. Goldman’s data suggested hedge funds had already begun that work in earnest.

Our view is that the positioning reset matters more than the weekly headline. A lower Mag 7 ownership base can eventually make the group less fragile, but only once the market is satisfied that the selling has moved from forced de-risking to discretionary rotation. Until then, every weak session in tech risks inviting another round of exposure trimming, particularly among funds that spent much of the year leaning into the same handful of growth names.