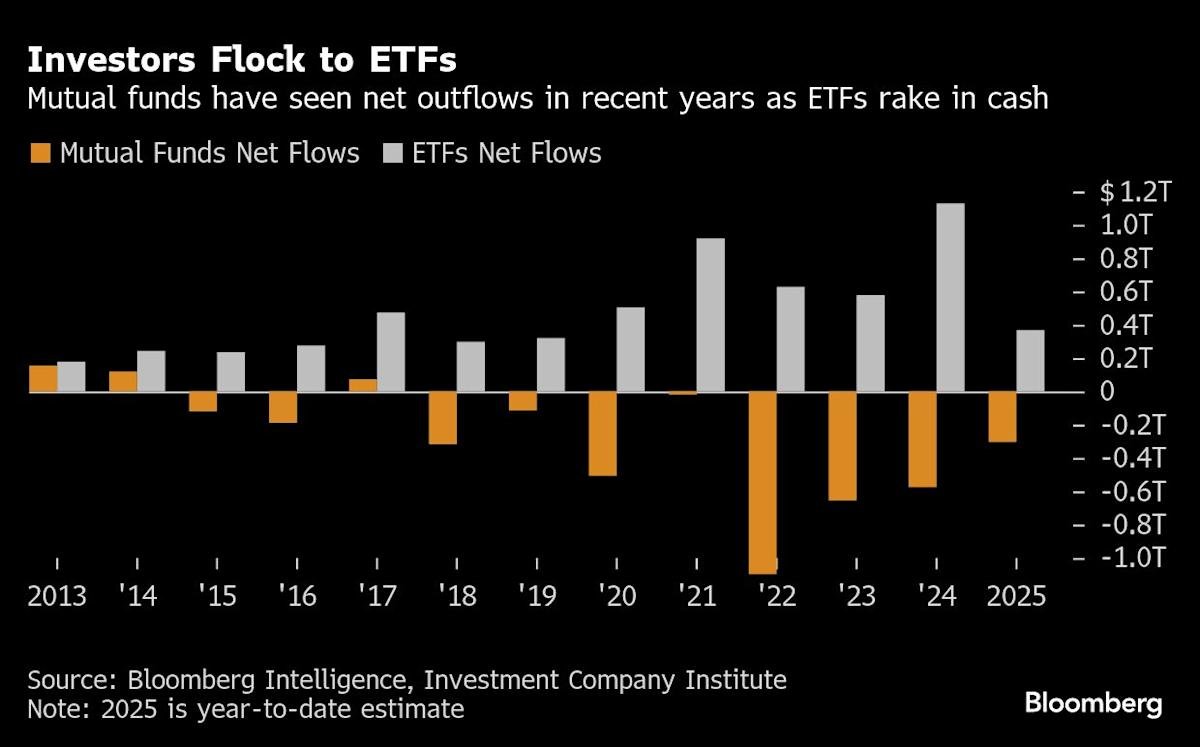

(Bloomberg) — Exchange-traded funds have amassed trillions of dollars by offering investors greater tax efficiency, liquidity and lower costs than mutual funds. Now, a looming regulatory shift is poised to bring the two vehicles closer together — and threatens to complicate the very features that fueled the ETF boom.

Most Read from Bloomberg

The US Securities and Exchange Commission is expected to approve applications for dual-share-class structures, perhaps as soon as this summer, allowing managers to add an ETF sleeve to an existing mutual fund. More than 50 firms, including BlackRock Inc. and State Street Corp., are waiting for the regulator’s greenlight to deploy the hybrid structure — made possible after Vanguard Group Inc.’s exclusive patent expired two years ago.

The two-in-one blueprint is a tantalizing prospect for asset managers looking to break into the ETF market at scale, without having to launch a new strategy from scratch. It also offers a lifeline to firms battered by years of mutual-fund outflows, as investors fled for more tax-efficient alternatives. The hybrid structure famously helped Vanguard save its clients billions in taxes over two decades.

Yet replicating that playbook may prove harder than it looks. Some Wall Street experts caution the shake-up could erode key benefits of the wrapper, especially if hybrid funds face significant withdrawals during market stress.

“I’ve been in the ETF business for 20 years — we have spent it talking about how great they are at managing capital gains, and I don’t think folks have an appreciation for how more ETFs could potentially end up paying capital gains distributions,” said Brandon Clark, director of ETF business at Federated Hermes, who previously led the ETF capital markets team at Vanguard.

At the heart of the concern is a tax dynamic that ETFs were built to avoid. These funds rarely pay capital-gains tax distributions, thanks to their in-kind redemption process, which allows the issuer to swap securities with authorized participants rather than sell them outright.

By contrast, mutual funds redeem in cash, meaning managers may need to sell securities to meet outflows. If those sales generate capital gains, they may distribute them to investors. In a hybrid vehicle, those taxable gains risk getting passed onto ETF shareholders, too.

“For mutual funds drawing inflows or net zero flows, there should be no issues, but for ones with outflows, there’s a potential risk for the ETF holders,” said Bloomberg Intelligence senior ETF analyst Eric Balchunas, in a note.

About two-thirds of ETF issuers surveyed by consulting firm Cerulli Associates flagged this spillover issue. There’s precedent. In 2009, a Vanguard fund distributed a 14% capital gain across both share classes, after a large mutual-fund withdrawal, Bloomberg data show. Though rare, the episode underscores the fiscal complications in the event a fund experiences outsized outflows within a shared portfolio.

“The investors that stand to benefit most immediately are the ones that already own the fund, as it can only improve the fund’s tax efficiency,” said Ben Johnson, head of client solutions at Morningstar Inc.

Wirehouses like UBS Group Inc., which list funds for financial advisers, are studying how this would impact which funds they will offer on their platforms.

An ETF share class could “run the risk of receiving tax distributions they otherwise wouldn’t have,” said Mustafa Osman, who runs due diligence on funds before they are added to the platform as head of ETF and mutual fund strategy and analytics at UBS.

The SEC refers to this issue as “cross-subsidization” and has directed applicants to detail how they’ll mitigate it. In response, firms like Dimensional Fund Advisors have amended their applications to detail a governance structure where the fund works with its independent board to determine if the dual structure is beneficial to both shareholders, while monitoring risks like cross-subsidization before and after launch. Among issues that would be considered: cash levels, unrealized gains and losses, and turnover.

Even standalone ETFs are paying out more capital gains more frequently these days, as more products track derivatives or assets that have risen markedly in value. In 2024, roughly 5% of passive ETFs paid out capital gains, the most since 2021, and 12% of active ones did, the highest since 2022, data compiled by Bloomberg show. Those figures are much larger for mutual funds, of course, with more than 50% paying them out last year.

Another complication lies in how the structure would impact the economics of ETF listings on big-name platforms. Cerulli estimates wirehouses and broker-dealer platforms could lose as much as $30 billion in revenue if mutual fund assets shift to ETF share classes in droves.

To stem the loss of revenue, intermediaries could begin to introduce revenue-sharing agreements with ETF issuers, which may ultimately raise costs for investors.

“This trend of trying to recapture some of that revenue that’s been slowly melting from the mutual funds has been in place for ETFs for the last few years,” said Ben Slavin, global head of ETFs at BNY.

Beyond fees and tax advantages, ETFs famously offer more liquidity than mutual funds — a selling point that may be undermined in some instances, if the two models are combined. According to Cerulli, ETFs that struggle to scale could see wider bid-ask spreads, with costs ultimately passed onto investors.

All told, this is uncharted territory. Vanguard’s success relied on stable flows, deep relationships with market makers and highly liquid portfolios. Large firms may be able to follow suit smoothly, but smaller managers holding less liquid assets could find the road ahead trickier.

“It’s not evident that authorized participants are ready for a plethora of smaller ETFs as a share class exposures, especially outside the most liquid underlying markets,” Cerulli researchers wrote in a report.