IDFC First Bank reported more than 20% year-on-year growth in deposits and advances in FY25. Management aims to sustain this pace of growth over the next few years. This has enthused investors, resulting in the stock bouncing back from its 52-week low. It has rallied by 28% in just over two months, registering steep outperformance over the broader sector’s 13% return.

But recent events threaten to dent investors’ newfound confidence. Will this mark the end of a short-lived bounce-back, or is it just a blip in a long-term rally?

Stumbling block in fundraise plans

Management has ambitious plans for the bank’s growth. But it has seen a persistent drag on profits from slippages and provisions in recent quarters, even as new business lines are yet to break even. So, it has been fueling growth by raising capital – more than ₹13,000 crore over the past five years.

Last month the bank’s board voted to raise another round of capital, and a large one at that. A fundraise of ₹7,500 crore was approved – ₹4,876 crore from an affiliate of Warburg Pincus and ₹2,624 crore from a wholly owned subsidiary of the private-equity division of Abu Dhabi Investment Authority. The fundraise will give the two investors a 14.5% stake, taking the bank’s total equity dilution over the past five years to 40%.

Also read: Defence stocks are soaring again, but can fundamentals support the rally?

But this week the plan hit a stumbling block. The proposal to induct a non-retiring board member from Warburg Pincus failed to secure the required consensus. Citing issues with Warburg’s shareholding at less than 10%, a majority of institutional investors voted against the proposal. Only 64.1% of shareholders approved the appointment, well short of the 75% regulatory requirement.

Capital adequacy comfortable, but growth at risk

If the fundraise falls through, the bank may need to go in for smaller and more frequent ones. This could cause delays in raising capital, hindering the bank’s ambitious plans for growth and profitability.

In its quest to become a full-suite universal bank, IDFC has made investments in new business lines including credit cards, cash management and wealth management, which are yet to achieve profitable scale. The bank was counting on the fresh capital to accelerate this.

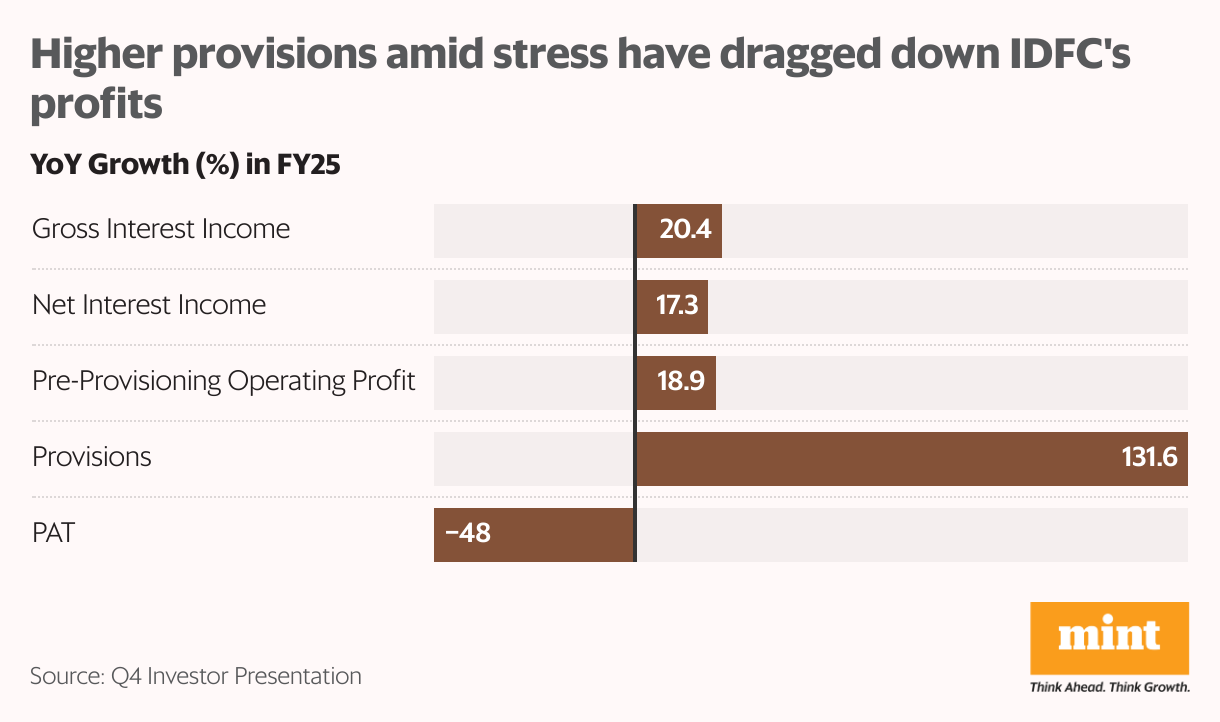

This holds even more relevance given the underwhelming profitability posted for FY25. Despite more than 20% growth in interest income and 19% growth in pre-provisioning operating profit, a 132% rise in provisions resulted in profits being slashed by half year-on-year. For a bank that is unable to compound capital by accumulating profits, raising capital is the last resort to fuel growth.

That said, the bank’s capital adequacy is sufficient even without the fresh capital.

Stress from infrastructure and microfinance

While retail loans are the bank’s mainstay, this is not a cause for concern. Coincidental delinquency in the segment is significantly superior to that of the industry, and collection efficiency has remained stable at 99.5%.

Also, only 14% of the total loan book is unsecured retail credit, where the bank has managed to maintain credit quality with gross non-performing assets (NPAs) contained at 1.89% and net NPA at 0.56%.

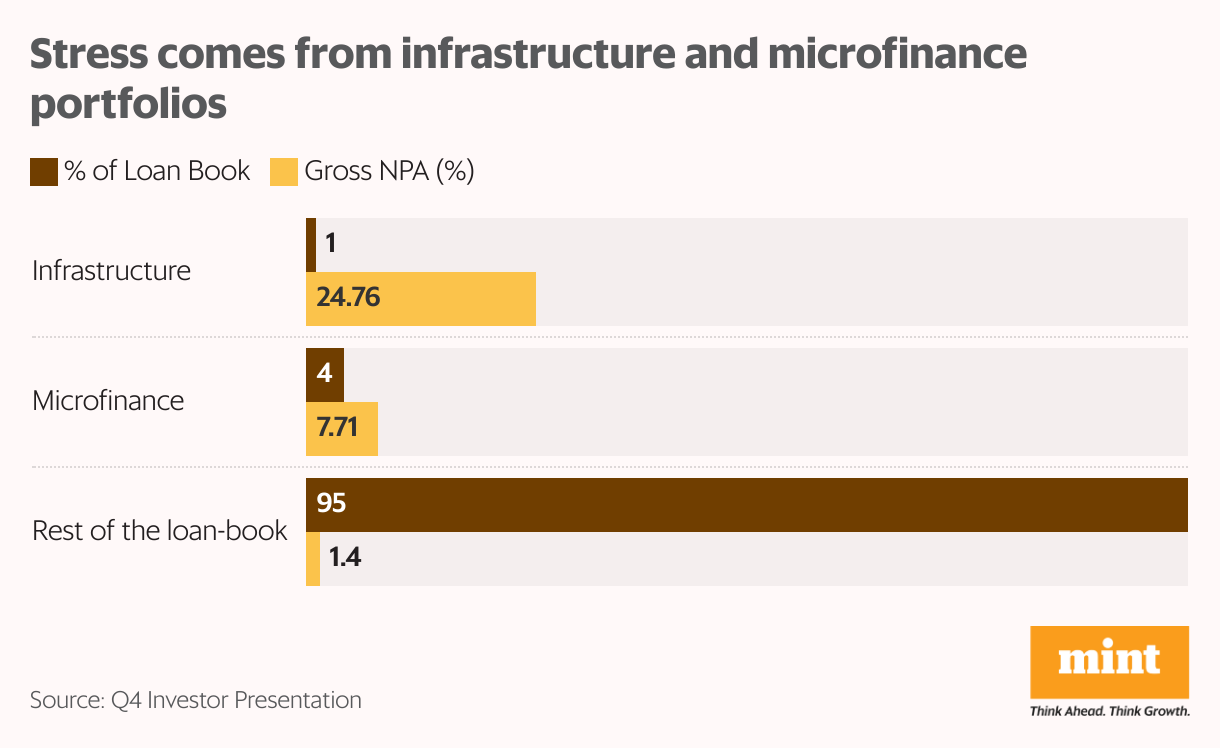

The stress in its books comes primarily from its microfinance portfolio and a toll-focussed infrastructure business that went belly-up during the year. Overall gross NPA as of March 2025 stood at 1.87%, but those in the microfinance and infrastructure portfolios were much higher at 7.71% and 24.76%, respectively.

Early indicators of reduced stress

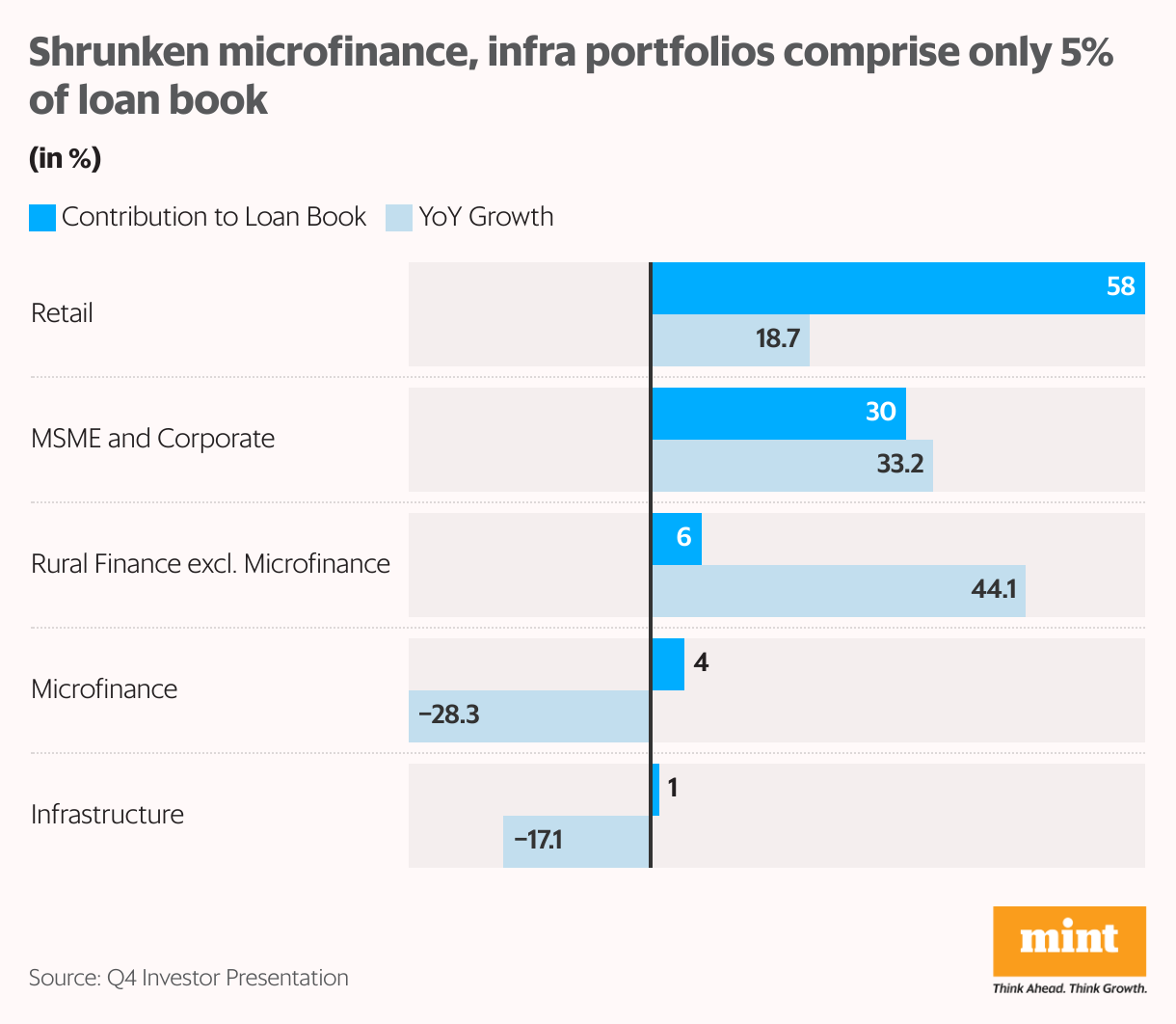

But these portfolios have been pared down in response to the stress. They have seen degrowth of 28% and 17% during the year, and together constitute only 5% of the bank’s book.

Also read: Chalet Hotels is gearing up for a major expansion. Should investors check in now?

The infrastructure portfolio has been all but written off entirely, and there are early indicators of improvement in the microfinance portfolio. While fresh slippages have increased sequentially from ₹437 crore to ₹572 crore, and SMA-1&2 (loans overdue by 30 to 90 days) has expanded from 4.56% to 5.1% for the microfinance portfolio, SMA-0 (loans overdue by less than 30 days) has seen a 45% sequential decline.

Moreover, incremental disbursements towards microfinance since 2024 have been covered under the Credit Guarantee Fund for Micro Units (CGFMU). About 66% of the bank’s microfinance book is currently covered under CGFMU. Finally, IDFC First has been proactive on provisioning. The provision coverage ratio has improved from 68.8% to 72.3% over FY25, reducing the risk of hidden stress.

Laggards are looking up

The bank’s cost-to-income (C-I) ratio is on the higher side at 73%, thanks to expansion of branch banking and credit cards, which are yet to achieve a profitable scale. Their C-I stands at 171% and 100%, respectively.

But losses have been shrinking in branch banking, and credit cards achieved breakeven in FY25. Management is aiming for a capital-driven scale to reduce the overall C-I to 65% by FY27. Income growth is expected to outpace growth in operating expenditure, thereby enhancing operating leverage and improving profitability.

Deposit growth continues to support margin growth

Since its merger with Capital First in 2018, the bank has persistently worked on shedding legacy high-cost borrowings while doubling down on low-cost current account and savings account (CASA) deposits.

While loans have doubled since the merger, deposits have grown six-fold. With the branch footprint expanding from 206 to more than 1,000, high interest-rates, monthly interest payouts, focus on advertising, and consistent improvement in technology and customer support, the bank has managed to grow its sticky and low-cost CASA base by 22 times.

Also read: Why Tata Teleservices is drawing institutional bets despite mounting losses

FY25 saw the trend continue. The bank paid off ₹7,000 crore of high-cost borrowings during the year, and plans on retiring them almost entirely by FY26. Meanwhile, customer deposits have expanded by 25.2%. Thanks to deposit growth outpacing credit growth, the incremental credit-deposit (CD) ratio for the fiscal moderated to 76.1%. A lower CD ratio creates room for profitable credit growth by sidestepping the need to supplement funds with high-cost borrowings. The bank’s cost of funds stood at 6.48% – among the lowest in mid-cap banks. Its net interest margin (NIM) was at 6.1%.

Rounding it up

Robust growth, early signs of moderating stress, and improving profitability of laggards suggest the recent dip in the bank’s profits is likely a blip on the way to a business turnaround. IDFC First Bank is confident of working through Warburg’s board seat holdup. The re-entry of Warburg into the bank’s cap table also speaks to its potential for long-term growth.

So, notwithstanding short-term headwinds, management is gunning for 20% credit growth over the medium term. Given the bank’s history of frequent capital raises, what’s more promising is that it is also aiming for return on equity to expand to 18-19% by FY29.

Of course, slippages in subsequent quarters and the performance of branch banking and credit cards will need to be monitored closely.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.