pcess609

Softer than expected latest inflation based on the consumer price index [CPI] at 2.9% year-on-year (YoY) in July, further confirms what has already become clear. The Fed could start cutting policy interest rates very soon. The markets are already pricing in a cut in September.

But here, I consider the following question: Is there anything in the fine print of the CPI report that can hold the Fed back? This is followed with a brief look at which way other key economic indicators point. And finally, there’s a discussion on why the impending rate cuts, in September or later, can be good news for investors anyway.

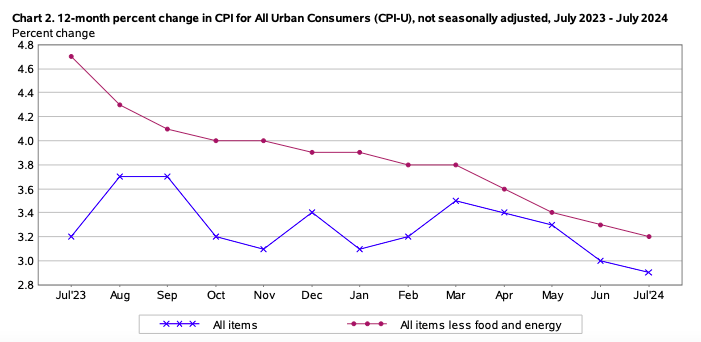

Annual inflation numbers are encouraging…

There are two highlights to the headline inflation figure. First, it’s the slowest rate seen since March 2021. Second, it’s also a shade lower than the forecast 3% YoY. Core inflation, which is inflation ex-food and energy that make up the volatile components, also softened to the slowest level since April 2021 at 3.2%. It was down from 3.3% YoY last month and is in line with projections.

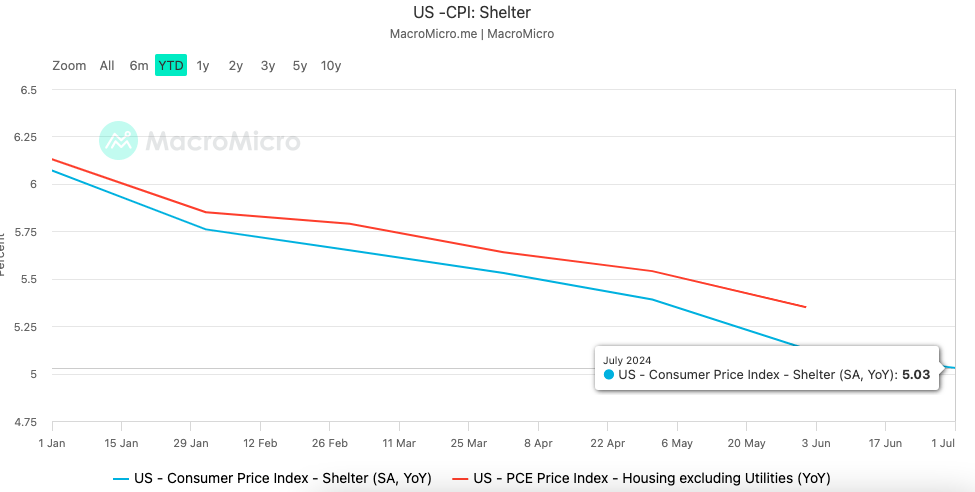

Significantly, shelter inflation also continued its consistent softening year-to-date [YTD] (see second chart below) and is now down to the lowest level since April 2022. The number, which now stands at 5.1% YoY, is significant since the shelter has a 36% weight in the CPI. It also continues to be the big driving force for inflation, accounting for 70% of the YoY inflation increase as per the latest release.

Source: Bureau of Labor Statistics Source: MacroMicro

…but monthly inflation is as projected

However, that’s where the progress on disinflation ends. The month-on-month (MoM) figures are far less encouraging. Here’s why:

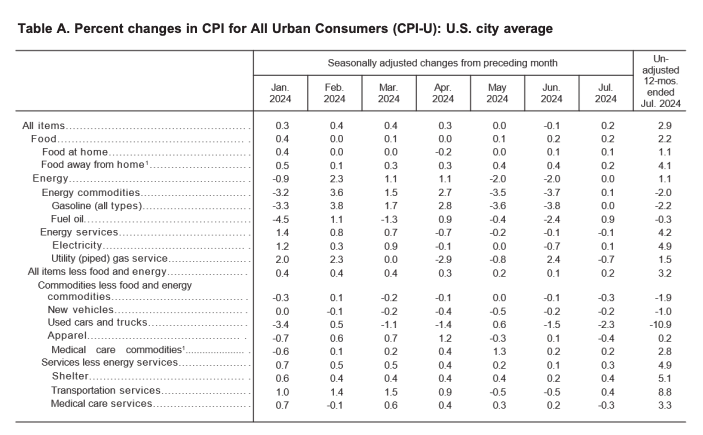

- Headline inflation was at 0.2% MoM, an about-turn after a 0.1% deflation in June and nil inflation in May. In other words, it’s the biggest monthly inflation in a quarter. In fact, the figure is exactly at the average inflation level YTD. It is, however, in line with expectations, so at least no negative surprise here.

- Core inflation also rose by 0.2% MoM, in line with forecasts but inching up from the 0.1% MoM figure in June and coming back to the same level as seen in May. It is, however an improvement over the YTD average figure of 0.3%.

- Shelter inflation remains sticky. At 0.4% MoM, it has risen from 0.2% in June and is exactly at the YTD average level. In fact, it accounted for 90% of the total MoM rise in CPI.

Source: Bureau of Labor Statistics

Essentially, the CPI report indicates that while there is definite improvement in inflation figures on a YoY basis, there’s not so much on a monthly basis. It’s some solace that the MoM numbers were in line with expectations, but the fact remains that there could be further progress.

How inflation sits against key economic trends

Key economic activity-related data, the labor market, and GDP, also pose contradictory trends. The unemployment rate rose to 4.3% for July, the highest level in over two and a half years. After the latest print, it’s even higher than the Fed’s projection of 4% in the final quarter of this year (Q4 2024).

While this indicates that the reserve can ease rates now, the fact remains that on the other hand, GDP growth is strong at 2.8% in Q2 2024. Added to this, the monthly inflation data isn’t entirely convincing even as annual inflation is encouraging indeed. The point here is, that the case for a rate cut in September can then be argued either way.

Stock markets price in cut…

Nevertheless, rate cuts are widely expected by market participants in September, with the biggest brokerages pencilling in a 25-50 bps cut. Possibly reflecting this, major indices are slightly up but not significantly, indicating that the cut could already be priced in. As I write after the inflation report, major indices are trading slightly up. The Dow Jones Industrial Average Index (DJI) has made 0.5% gains, followed by the S&P 500 Index (SP500, SPX) at 0.3% and the NASDAQ 100-Index (NDX) is up by 0.2%.

…but bigger market gains could be in-store

Whether the rate cut happens in September or later, going by a recent Wells Fargo Advisors study, though, the stock markets could be in for a boost in the coming months anyway. The study points out that the “why” behind a rate cut is important in determining the fortunes of the stock markets in the following months. In the past, when the Fed has slashed rates following easing inflation, rather than in response to a recession, equity markets have performed well. Here’s precisely what it says:

Historically, the index has continued its upward trajectory 18 months past the initial cut in periods when the Fed easing cycle did not correspond with a recession. Alternatively, when the Fed rate cut cycle did correspond with a recession, performance was choppy before ending essentially flat over the 18-month period.

The study also compares the present situation with 1995, since the two periods are similarly placed. At that time, in the 12 months following a cut, the S&P 500 was up by 23%. The biggest sectoral gainers were healthcare, consumer staples, and financials, in that order, with each showing 30%+ annual gains after the first cut.

Options for risk-averse investors

Still, the past and present aren’t a perfect correlation. So there are no guarantees that 2025 will play out like 1995. The risk to economic growth, for example, can tell on the stock markets. And if growth truly does slow down considerably, it can play on both companies’ numbers and the stock markets.

But there are several investing opportunities for the more risk-averse investors as well. In fact, I’ve pointed towards healthcare as a potentially good defensive sector in the past, and in light of the gains it made in 1995, there’s one more reason to consider it now. For medium-to-long-term investors, value stocks would also be worth considering now.

In conclusion

In conclusion, the latest CPI inflation report indicates that the market might just be on point regarding a rate cut in September, with the annual inflation figure coming in slightly below expectations. It’s also backed by a weaker-than-expected unemployment rate. But considering less progress on monthly inflation and strong GDP numbers for Q2 2024, I wouldn’t rule out some probability of a rate cut further down the line and not in September.

Still, the fact that the rate cuts will be driven by softening inflation and not an economy in the doldrums, could be a significant positive for the equity markets, going by a recent Wells Fargo study. Interestingly, though, whether the markets perform well or not, a highlight sector is healthcare, which seems to offer an upside right now.