Southeast municipal bond issuance bounced back in the first half of 2024, with dollar volume rising 42.4% from the first half of 2023.

This followed a

The Southeast bond volume increase in first half of 2024 from the first half 2023 was better than the 32.3% national increase over the same period, according to LSEG data.

“The Southeast has continued to grow rapidly in population requiring more public improvements,” said John Hallacy, president of John Hallacy Consulting LLC. “Issuance for healthcare, transportation, and utilities all increased by 100% or more versus the prior year. Rates have cooperated this year by maintaining lower levels. Last year rates remained higher for longer [and] that served to hold issuance back to a degree.”

First half Southeast dollar volume was $45.5 billion, with $18.3 billion coming in the first quarter and $27.2 billion in the second quarter. The second quarter saw an increase from the second quarter 2023 of 57.7%, compared to a national second quarter increase of 35.4%.

“The positive performance in the second quarter is due to moderating rates,” Hallacy said. “Also, federal aid that has been flowing has been received for projects by now and issuers need to provide more of their financing on their own.”

The first half’s $45.5 billion

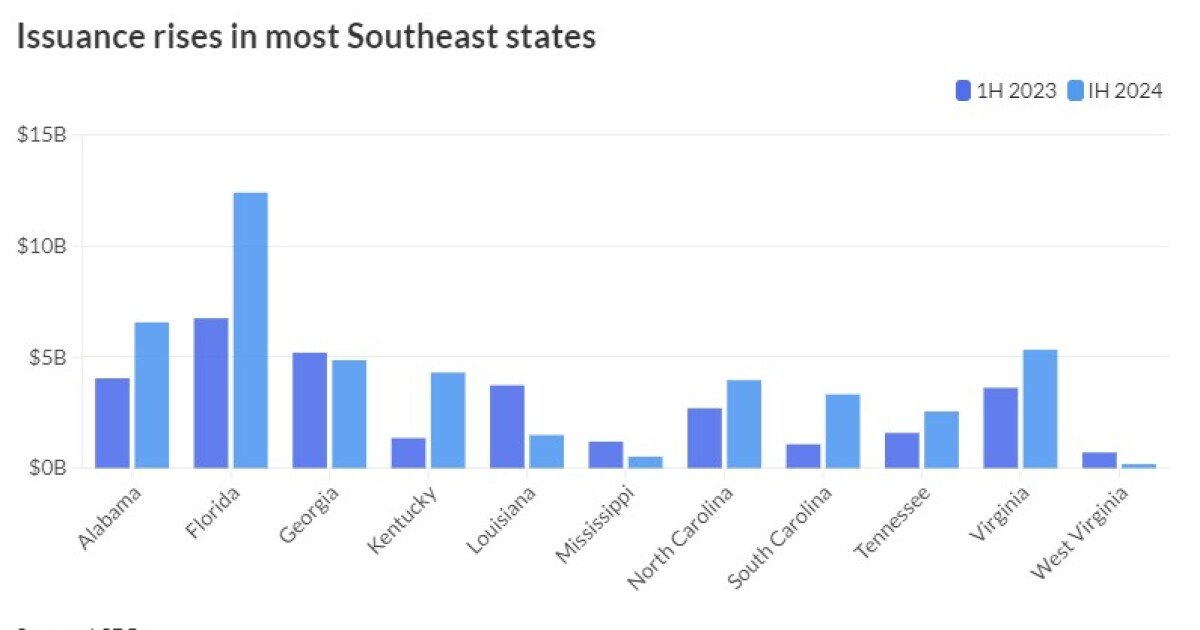

State by state

Issuers in Florida led the way, selling $12.4 billion of municipal debt, an 83.9% increase year-over-year.

Alabama was second, at $6.57 billion, a 62.2% gain, followed by Virginia, at$5.33 billion, Georgia with $4.86 billion and, Kentucky with $4.3 billion.

Other states seeing increases of more than 60% year-over-year were Kentucky with 217.9%, South Carolina with 208.9% and Tennessee with 60.9%.

On the flip side, West Virginia issuance contracted 73.7% to $185 million, Louisiana saw a drop of 60% to $1.5 billion and Mississippi slipped back 56.6% to $519 million.

Georgia was the other state to see volume fall year over year, down 6.4% to $4.9 billion.

The number of issues in the regions increased only 6% to 566 from 534. In the five states with the biggest dollar volume percent increases, the issue numbers increased moderately in three of them. The exceptions were South Carolina, where the number of issues declined to 31 from 33, and Tennessee, where the number of issues increased to 32 from 14.

Tax-exempt issuance in the region was up 43.7% to $37.7 billion.

Taxable issuance was down 20% to $3.8 billion. Bonds with interest subject to the alternative minimum tax more than quadrupled in volume to $3.98 billion, on the back of a $3.1 billion Florida Development Finance Corp. AMT deal in April

Refunding volume in the region was up 65.5% to $7.8 billion, outpacing the U.S.’s 56.6% increase. The region had $33.7 billion in new money issues and $4 billion in issues LSEG classifies as combined new money and refunding.

Trends with revenue and general obligation bonds also fit this pattern. While U.S. revenue bond volume increased 54.5%, in the Southeast it went up 62.7%. In the U.S. GO bond volume increased a modest 3.4% but in the Southeast it slid 20%.

The Southeast had $39.2 billion of volume LSEG classes as revenue bonds but only $6.3 billion of GO volume.

The Southeast’s 14% share for GO bonds is well below the 34% share nationally.

Hallacy explained that in the first half the region had more focus on systems with revenue cash flows, like utilities.

The region saw $35.5 billion in negotiated bond volume, $8.9 billion in competitive, and $1.1 billion in private placements. The first two were up 68.5% and 30.8% respectively from the first half of 2023, while the last was down 72.6%.

Sectors

The sector with the most volume was utilities with $12.6 billion, doubling the year-ago number. That figure is driven by energy prepayment deals, which

The next-busiest sectors were education at $7.2 billion, transportation at $6.6 billion and general purpose with $6.1 billion.

Education volume increased 25.7%. The number of issues increased to 156 from 133.

In the first half of 2024, education issuance was 15.8% of all municipal bond issuance in the Southeast compared to a 26.6% slice in the United States. Hallacy said smaller schools are holding back on issuance and some deals are getting done away from the municipal market.

Transportation volume doubled.

While the environmental facilities sector was the smallest sector overall in dollar volume, at $628 million, it did see the biggest jump in volume at 206.3%. However, both the first half of 2023 and the first half of 2024 saw just three issues each.

Biggest deals

The Brightline deal was the region’s largest of the first half at $3.144 billion. Morgan Stanley was the lead manager on the April 26 alternate minimum tax bond sold through the Florida Development Finance Corp.

The

Next on the list was a $1.91 billion South Carolina Jobs Economic Development Authority deal

The fourth-biggest bond was a natural gas prepay refunding from Kentucky Public Energy Authority on June 18, managed by Morgan Stanley.

The fifth-largest bond and the only other bond above $1 billion in the first half was issued by the Florida State Board of Administration Finance Corporation for the

The taxable bond was priced on April 18 with Morgan Stanley, BofA Securities, JP Morgan, and Wells Fargo jointly managing it.

League tables

The biggest senior managers in the half were Morgan Stanley, credited by LSEG with underwriting $7.51 billion, BofA Securities with $7.36 billion, RBC Capital Markets with $5.11 billion, Raymond James with $4.78 billion, and JP Morgan with $4.65 billion.

The top municipal advisor was PFM Financial Advisors, credited with $9.75 billion, followed by Municipal Capital Markets Group with $3.99 billion, Davenport with $2.99 billion, Public Resources Advisory Group with $2.96 billion, and Kaufman Hall & Associates with $2.12 billion.

Greenberg Traurig topped the bond counsel chart, credited with $5.64 billion, followed by Kutak Rock with $5.2 billion, Balch & Bingham with $2.35 billion, Alston & Bird with $2.3 billion, and Nabors Giblin & Nickerson with $1.8 billion.

The use of bond insurance increased both compared to first half of 2023 and as a proportion of all deals. Insured volume was up 66% from a year earlier to $3.6 billion. The share of the dollar volume carrying insurance increased to 7.9% from 6.8%. The share of deals carrying insurance increased to 9.2% from 7.7%.

The biggest issuers of the half were Florida Development Finance Corp. driven by the Brightline deal, with $4.4 billion, Main Street Natural Gas with $2.3 billion, Jefferson County with $2.24 billion, South Carolina Jobs Economic Development Authority with $2.01 billion, and the Kentucky Public Energy Authority with $1.76 billion.