In recent years, government-issued bonds have become some of the most attractive instruments in Nigeria’s financial ecosystem.

With yields ranging between 14% and 18%, Federal Government bonds, Sukuk instruments, and treasury bills have drawn in a flood of investor capital.

On the surface, this looks like a win for fiscal stability.

After all, the government is raising funds to plug budget gaps and finance infrastructure.

But beneath the surface lies a growing disruption: these bonds are quietly reshaping the investment landscape, often to the detriment of real-sector growth and private capital formation.

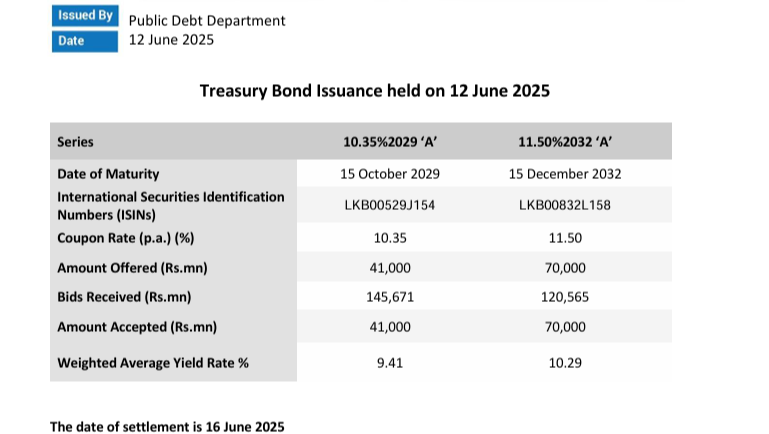

In May 2025, the Federal Government of Nigeria broke records when the Series VII of the Sovereign Sukuk recorded an unprecedented subscription level of over N2.21 trillion, representing an over-subscription of 735 percent. Many public narratives frame this as evidence of investor trust.

In reality, it’s the high yield interest rates, not a strong policy environment, that attract capital to these instruments.

In an environment where private equity struggles, IPOs are rare, and startups face capital droughts, investors are simply chasing the safest and most profitable option available. Government securities, with their sovereign backing and high returns, tick that box.

But when the public sector offers double-digit yields on risk-free instruments, it becomes irrational for banks, funds, or individuals to support private risk or venture capital. In short: why bet on business when you can lend to the government and earn more?

Those who still manage to invest in the private sector must contend with Nigeria’s long-standing struggle with ease of doing business. High regulatory costs, multiple taxation layers, inconsistent policy enforcement, poor infrastructure, and security risks; all of these make subscribing to government-issued bonds far more appealing.

There have been reform attempts, such as the Presidential Enabling Business Environment Council (PEBEC), set up in 2016 to remove bureaucratic constraints to doing business. Efforts like the digitization of company registration by the Corporate Affairs Commission (CAC) and executive orders targeting port efficiency are notable. But progress is painfully slow, and the reforms remain mostly administrative, not systemic.

Foreign Direct Investment (FDI) thrives on policy stability, regulatory clarity, and supportive infrastructure. Yet FDI into Nigeria has steadily declined, while government bond issuance has expanded.

Rather than building investor trust through policy certainty and infrastructure guarantees, Nigeria is rewarding passive capital with risk-free, high-return instruments. Ironically, these instruments compete with and suppress the very investments the country desperately needs.

This sends a poor signal to long-term investors: we are a high-yield debt market, not a growth opportunity. It is no surprise that FDI flows into manufacturing, services, and agribusiness have dropped in recent years, while portfolio investors chase government bonds instead.

This is not to say bonds are bad. They are necessary tools for sovereign financing and infrastructure development. But Nigeria must urgently strike a better balance between sovereign borrowing and private sector stimulation.

The government should prioritize legal reforms that encourage tax-efficient private investment, reduce regulatory bottlenecks for venture capital and equity markets, and enforce prudent borrowing practices. If Nigeria is to grow its productive base, it must stop rewarding passivity and start incentivizing innovation, equity, and enterprise.

This article is written by Jawondo Ibrahim, Esq., an Associate at Veblen Solicitors, specializing in capital markets, Islamic finance, regulatory compliance, and corporate practice.