Take a look at the essential concepts, terms, quotes, or phenomena every day and brush up your knowledge. Here’s your knowledge nugget on the Government Securities (G-Secs) and related economy terms for your UPSC CSE Prelims 2026.

(Relevance: In 2018, a Prelims question was asked on G-Secs. This topic reflects the government borrowing programme, fiscal deficit management, and overall macroeconomic stability— core areas in the Indian Economy. Therefore, it is important to understand this topic for your Prelims 2026.)

The Reserve Bank of India (RBI) has retained the percentage limits for foreign portfolio investors (FPIs) investments in the debt market for the year 2026-27. The limits for FPI investment in Government Securities (G-Secs), State Government Securities (SGSs) and corporate bonds will remain unchanged at 6%, 2% and 15% respectively, of the outstanding stocks of securities for FY27 for the general route, as per the RBI’s circular of 6th April, 2026.

Key takeaways:

1. G-secs, or government securities or government bonds, are tradable instruments issued by the Central Government or the State Governments. It is used by the government to borrow money from the public.

Bond Yield vs Bond Price: The Inverse Relationship Explained

THE BASICS

A bond is a loan you give to the government

Government Securities (G-Secs) are tradable instruments issued by the Central or State Governments to borrow from the public. The government pays you annual interest (coupon) and returns your principal at maturity. G-Secs carry practically no default risk — they are called risk-free gilt-edged instruments.

◆

Face Value

The original price of the bond — typically ₹100. The government repays this exact amount at the end of the bond’s tenure.

₹

Coupon Payment

Fixed annual interest paid by the government. Example: ₹5 per year on a ₹100 bond = 5% coupon rate. This amount never changes regardless of market conditions.

%

Yield (Effective Return)

Yield = Coupon ÷ Market Price. Unlike the coupon, yield is not fixed — it changes as the bond’s market price changes in response to demand.

THE INVERSE RULE

As bond price rises, yield falls — and vice versa

A 10-year G-Sec with face value ₹100 pays a fixed coupon of ₹5. If two buyers compete for this bond, the market price gets bid up. The coupon stays fixed at ₹5 — but as the price rises, the effective yield falls. At ₹125, the ₹5 coupon delivers exactly 4% yield.

₹100

Face value price → Yield = 5%

₹110

Demand pushes price up → Yield = 4.5%

₹125

Equilibrium price → Yield = 4%

THE MECHANISM

Bond yields track the prevailing interest rate in the economy

If the economy’s prevailing rate is 4% and a new G-Sec offers 5% yield, investors rush to buy it. Demand pushes the price up and yield down — until yield converges with the 4% market rate at a bond price of ₹125.

①

G-Sec yield exceeds market rate

Investors spot a better return than what the economy offers. Demand for the bond surges.

②

Rising demand pushes price up

Competitive bidding raises the bond’s market price above its face value of ₹100.

③

Fixed coupon, falling yield

The ₹5 coupon stays unchanged. As market price rises, the effective yield (₹5 ÷ price) falls towards the market rate.

④

Equilibrium restored

Price settles at ₹125 — where yield equals the 4% prevailing rate. Excess demand stops.

“If market interest rate levels rise, the price of a bond falls. Conversely, if interest rates or market yields decline, the price of the bond rises.”

— Reserve Bank of India

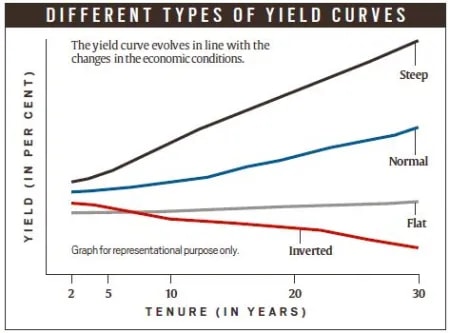

THE YIELD CURVE

A graph that reveals what the market expects from the economy

A yield curve plots yields of government bonds of equal credit rating across different maturities. Its shape — normal, flat, or inverted — signals the market’s collective view on growth, inflation, and future risk.

↗

Normal Curve (Upward Sloping)

Longer-tenure bonds offer higher yields — investors demand more reward for longer lock-ins. Signals a growing economy. A steeper slope = faster expected growth.

→

Flat Curve

Short and long-term yields are nearly equal. Signals marginal or slowing growth — investors see little difference in risk across time horizons.

↘

Inverted Curve — Recession Warning

Longer-tenure yields fall below short-tenure yields. Investors expect sharp future growth decline and lower money demand. Historically a reliable predictor of recession.

Sources: Reserve Bank of India · Indian Express Explained · UPSC Essentials, April 2026

2. The two key categories are treasury bills and dated securities. Treasury bills are short-term instruments which mature in 91 days, 182 days, or 364 days, and dated securities or government bonds are long-term instruments, which mature anywhere between 5 years and 40 years.

3. In 2010, the RBI introduced a new short-term instrument, known as Cash Management Bills (CMBs) with the aim to manage the temporary cash flow mismatches. CMBs, having the same generic character of T-Bills, are issued for maturities less than 91 days.

4. Treasury bills, or T bills are zero coupon securities and pay no interest. They are issued at a discount and redeemed at the face value at maturity. Let’s understand this through an example:

Story continues below this ad

A 91 day Treasury bill of ₹100 (face value) may be issued at say ₹ 98.20, that is, at a discount of say, ₹1.80 and would be redeemed at the face value of ₹100. The return to the investors is the difference between the maturity value or the face value (that is ₹100) and the issue price (that is ₹ 98.20).

5. According to the RBI, “In India, the Central Government issues both, treasury bills and bonds or dated securities while the State Governments issue only bonds or dated securities, which are called the State Development Loans (SDLs). G-Secs carry practically no risk of default and, hence, are called risk-free gilt-edged instruments.”

6. The RBI is the sole authority for the G-Secs which issues it through auctions. The auctions are conducted on an electronic platform called the E-Kuber, the Core Banking Solution (CBS) platform of RBI. Commercial banks, Urban Co-operative Banks (UCBs), Insurance companies, and others who are members of E-Kuber can place their bids in the auction through this electronic platform.

Bond yield and its relationship with the bond price

1. The effective interest on the government bonds is called yield. But the rate of return is not fixed — it changes with the price of the bond. But to understand that, one must first understand how bonds are structured. Every bond has a face value and a coupon payment. There is also the price of the bond, which may or may not be equal to the face value of the bond.

Story continues below this ad

Bond yield curves

Bond yield curves

2. Suppose the face value of a 10-year G-sec is Rs 100, and its coupon payment is Rs 5. Buyers of this bond will give the government Rs 100 (the face value); in return, the government will pay them Rs 5 (the coupon payment) every year for the next 10 years, and will pay back their Rs 100 at the end of the tenure. In this case, the bond’s yield, or effective rate of interest, is 5%. The yield is the investor’s reward for parting with Rs 100 today, but for staying without it for 10 years.

3. Imagine a situation in which there is just one bond, and two buyers (or people willing to lend to the government). In such a scenario, the selling price of the bond may go from Rs 100 to Rs 105 or Rs 110 because of competitive bidding by the two buyers. Importantly, even if the bond is sold at Rs 110, the coupon payment of Rs 5 will not change. Thus, as the price of the bond increases from Rs 100 to Rs 110, the yield falls to 4.5%.

4. Bond yields are in line with the prevailing interest rate in the economy. With reference to the above example, if the prevailing interest rate is 4% and the government announces a bond with a yield of 5% (that is, a face value of Rs 100 and a coupon of Rs 5) then a lot of people will rush to buy such a bond to earn a higher interest rate.

5. This increased demand will start pushing up bond prices, even as the yields fall. This will carry on until the time the bond price reaches Rs 125 — at that point, a Rs-5 coupon payment would be equivalent to a yield of 4%, the same as in the rest of the economy.

Story continues below this ad

6. According to the RBI, “If market interest rate levels rise, the price of a bond falls. Conversely, if interest rates or market yields decline, the price of the bond rises. In other words, the yield of a bond is inversely related to its price.”

7. A yield curve is a graphical representation of yields for bonds (with an equal credit rating) over different time horizons. Typically, the term is used for government bonds — which come with the same sovereign guarantee.

8. If bond investors expect the economy to grow normally, then they would expect to be rewarded more (that is, get more yield) when they lend for a longer period. This gives rise to a normal — upward sloping — yield curve.

9. The steepness of this yield curve is determined by how fast an economy is expected to grow. The faster it is expected to grow the more the yield for longer tenures. When the economy is expected to grow only marginally, the yield curve is “flat”.

Story continues below this ad

10. Yield inversion happens when the yield on a longer tenure bond becomes less than the yield for a shorter tenure bond. It portends a recession. An inverted yield curve shows that investors expect the future growth to fall sharply; in other words, the demand for money would be much lower than what it is today and hence the yields are also lower.

BEYOND THE NUGGET: Open Market Operations (OMOs)

1. The RBI uses Open market operations (OMOs) in order to adjust the rupee liquidity conditions in the market on a durable basis. When the Reserve Bank feels that there is excess liquidity in the market, it resorts to the sale of government securities, thereby sucking out the rupee liquidity.

2. Similarly, when the liquidity conditions are tight, the central bank buys securities from the market, thereby releasing liquidity into the market. It’s used as a tool to rein in inflation and money supply in the system.

3. However, when liquidity is sucked out, it can lead to a spike in bond yields as the RBI will release more government securities into the market and bond buyers demand more interest rate on these securities.

Post Read Question

Consider the following statements: (UPSC CSE 2018)

Story continues below this ad

1. The Reserve Bank of India manages and services Government of India Securities but not any State Government Securities.

2. Treasury bills are issued by the Government of India and there are no treasury bills issued by the State Governments.

3. Treasury bills offer are issued at a discount from the par value.

Which of the statements given above is/are correct?

(a) 1 and 2 only

(b) 3 only

(c) 2 and 3 only

(d) 1, 2 and 3

(Sources: Explained: Bonds, yields, and inversions, Explained: What are government securities, why the sudden push?, Explained: What are G-Sec yields, and how and why do they go up and down?)

Story continues below this ad

Subscribe to our UPSC newsletter. Stay updated with the latest UPSC articles by joining our Telegram channel – IndianExpress UPSC Hub, and follow us on Instagram and X.

🚨 Click Here to read the UPSC Essentials magazine for March 2026. Share your views and suggestions in the comment box or at manas.srivastava@indianexpress.com🚨