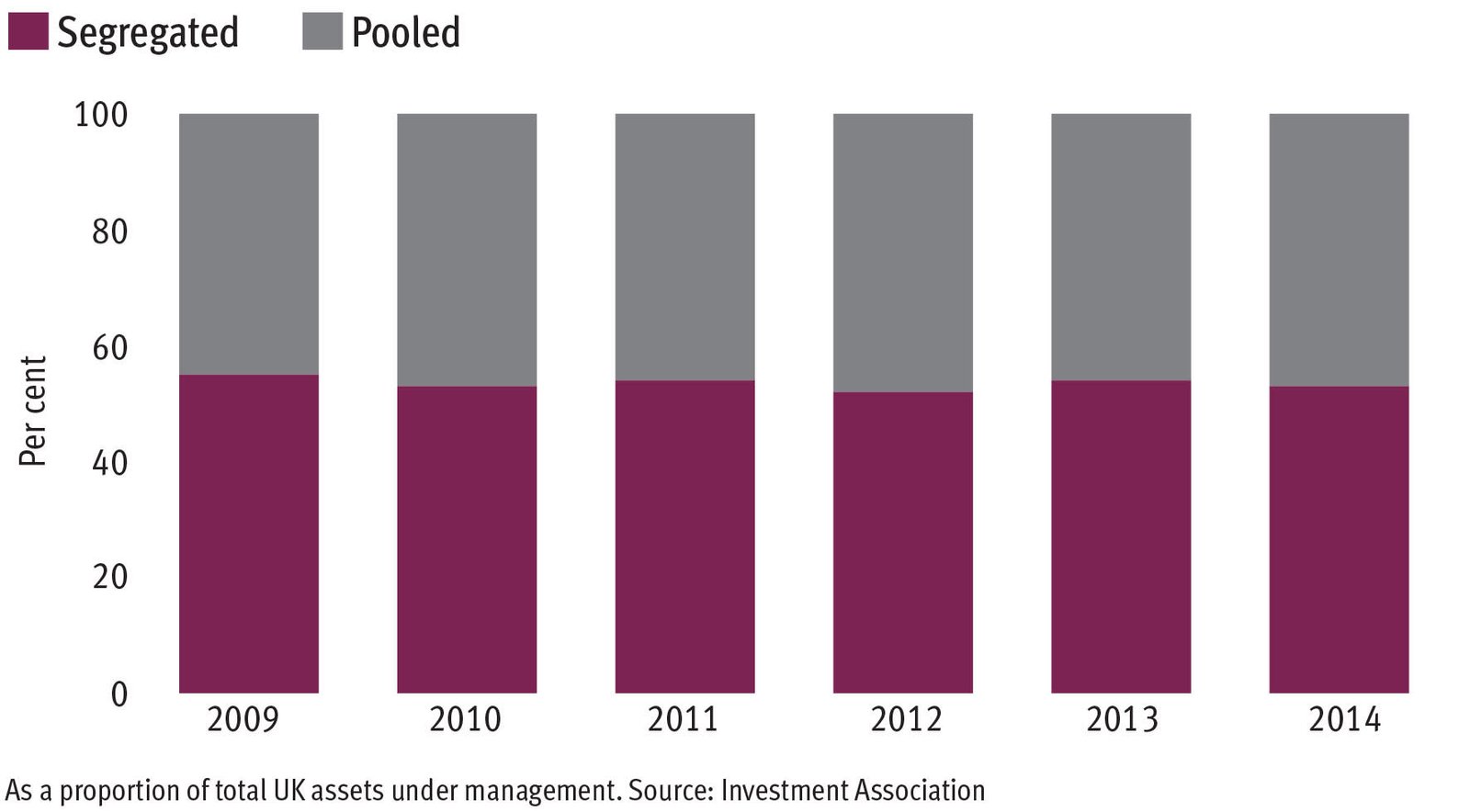

A growing trend for adviser and discretionary firms to seek segregated mandates from asset managers, rather than using traditional pooled vehicles, has been tipped to continue despite the increased regulatory requirements involved.

The use of these mandates – a favoured investment method for institutions and other large investors – has gradually filtered down to discretionary fund managers (DFMs) and larger adviser firms in recent years. The advantages are in keeping with those usually associated with economies of scale: lower fees and more control.

As adviser consolidation continues, and assets under management at DFMs grow, the structures have become more accessible to many in the market. But using them means an advisory firm is, in the eyes of the regulator, effectively running assets itself. That requires a new set of permissions and may increase capital adequacy requirements.

Fergus McCarthy, head of UK and Ireland intermediary distribution at BNY Mellon Investment Management, said: “It’s inevitable that if you’re a restricted advice firm of a large enough size, with the right resources, it’s a fairly straightforward decision.

“You tend to find that fees for segregated mandates are more institutional-like in their pricing because of the amounts of money involved.”

Independent advisers are less likely to consider this approach because a fund in their name may conflict with their commitment to consider the whole of the market. But restricted firms and DFMs are different.

Simon Hillenbrand, Henderson’s head of UK retail, said: “The number of advisers has shrunk post-RDR and the number of firms that conduct investment management business has become smaller. With continued consolidation you could make a case for some of the larger firms looking at this option.”

Scale is not the only driver of the increased use of such mandates. DFM Psigma, for example, uses segregated mandates for its fixed income exposure, in part because of liquidity concerns.

The absence of other holders also limits “co-investor risk” – a situation where a fund is dominated by, and therefore beholden to, the asset allocation decisions of one large investor.

Despite these benefits, some in product development have warned of the risk of firms ending up in the regulator’s cross hairs if they use lower fees to boost their own margins.

Alan Gadd, head of product and distribution development at Artemis, said such shifts may prove unfeasible given the higher focus on fee transparency.

He said: “[The use of segregated mandates] will grow, but I don’t think it’s quite the El Dorado that some advisers might think. If they want to go in with disguised fees they will have to think again.

“Clearly, the FCA is concerned about conflicts of interest and, coming out of the asset management study, the way that fees or margins are disclosed is going to have to be a lot more transparent.”

Dennis Hall, managing director at Yellowtail Financial Planning, said: “[Advice firms] would be stupid not to pass on cost savings because they could say, ‘we have got these funds at this price, so why would you go to someone else’. It is a logical thing for larger firms to do as a way to differentiate their offering.”

David Thomas, chief executive at multi-asset specialist Seneca Investment Management, stressed the need for “cultural alignment” between advice firms and fund houses, particularly in areas such as fees.

“Quite often you can look at those [mandates] and think ‘that is quite small’, and it’s probably not very important to that big fund manager who’s running it,” Mr Thomas said.

“You don’t want to end up with funds being managed that are last in the queue.”