Investment funds, tax advisors, decentralized finance projects, and the fifteen percent of Americans who own cryptocurrency should pay close attention to the proposed bill “Digital Asset Market Clarity Act,” known as the CLARITY Act. Here is what this post covers:

- How the bill divides jurisdiction between the SEC and the CFTC, and why the line between a “digital commodity” and an “investment contract asset” matters;

- Whether stablecoin platforms can pay interest;

- Closing the crypto wash-sale loophole under IRC § 1091 and why the planning window may be short;

- Expanded Form 1099-DA reporting and what it means for smaller or DeFi-adjacent platforms;

- The apparent exemption of decentralized finance and peer-to-peer activity from registration, and the potential loophole risk that creates; and

- Material favoring of U.S.-domiciled offerors.

The Current Cryptocurrency Issue

On April 8, 2026, Treasury Secretary Scott Bessent published an op-ed in the Wall Street Journal calling on the Senate to quickly pass the CLARITY Act. His message was simple: “A growing share of crypto development relocated to places with clear rules. The benefits of domiciling in the U.S. rarely outweighed the risks.” Scott Bessent, The Wall Street Journal, April 8, 2026.

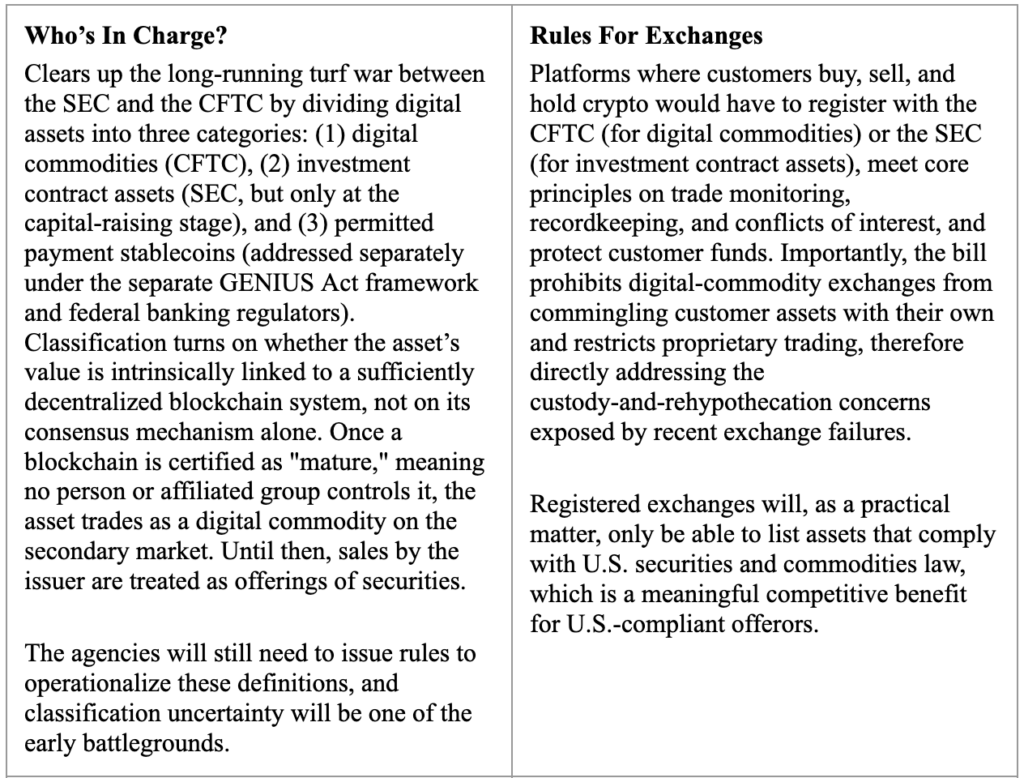

The central legal issue the CLARITY Act tries to resolve is straightforward: which digital-asset activity should be regulated as a public offering or public exchange of a security or commodity, and which should be unregulated as private, peer-to-peer activity?

The bill draws that line in three places: (1) how digital assets are classified (commodity vs. security); (2) how exchanges and brokers are registered; and (3) what is carved out for decentralized finance and peer-to-peer transactions. Additional questions worth asking are: who gains from where those lines fall? U.S.-domiciled offerors and registered exchanges that will enjoy a compliant, predictable market. And who may lose? Retail purchasers on the DeFi side of the line, where the traditional investor-protection rationale for regulation still applies but the statutory regime may not.

What the Clarity Act Does

The CLARITY Act is a proposed rulebook for the public side of the U.S. digital-asset market covering initial coin offerings, registered exchanges, and the brokers and dealers operating on those exchanges. It leaves decentralized, peer-to-peer activity largely outside that perimeter. The core mechanics are following:

Where Does the Bill Stand Right Now?

The bill was introduced in May 2025 and cleared the House in July 2025 by a 294–134 vote. That was the easy part. Two Senate committees, Banking and Agriculture, are each marking up their own version covering different pieces of the market. Both must be finalized, merged, and then reconciled with the House version. That is a lot of moving pieces, and the window is narrowing: if the Senate does not act before midterm-election campaigns pick up this summer, the bill risks losing momentum entirely. Two fights are causing this delay.

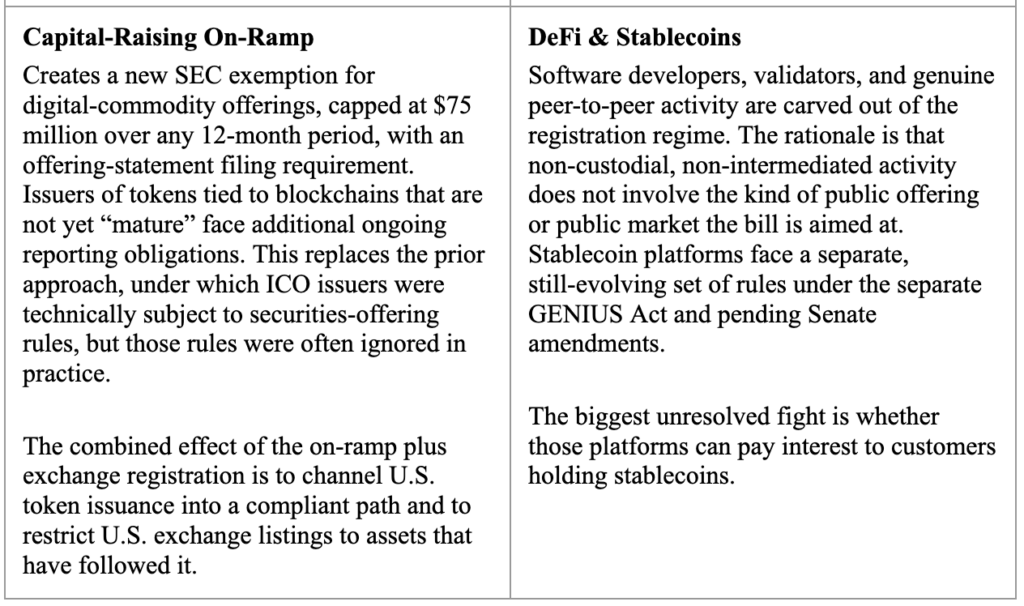

The first is stablecoin interest and whether platforms can pay holders a yield on stablecoin balances. Banks say no, because interest-bearing stablecoins compete directly with insured deposits. Crypto firms say yes, because yield is central to the product. Coinbase, the largest U.S.-based cryptocurrency exchange, withdrew its support for the bill over this issue earlier this year.

The second is the scope of the DeFi carve-out. The bill’s rationale for exempting decentralized, peer-to-peer activity is conceptually sound because it is not a public offering or a public exchange. But the classical securities-law exemptions for private transactions rest on knowing the purchaser’s sophistication, relationship to the issuer, or accredited status. DeFi counterparties are anonymous. That mismatch is likely to create a loophole that sophisticated projects will structure into, and that will expose less sophisticated retail purchasers to risks the regulated structure was designed to prevent.

What This Means For Crypto Holders and the Practitioners Who Advise Them

In the short term, nothing changes. The bill has not passed. But the practical implications are close enough that holders and practitioners should be positioning now rather than reacting later. The items below combine the client-facing takeaway with the practitioner action item in each case.

- THE CRYPTO WASH-SALE WINDOW MAY BE CLOSING. Under current law, IRC § 1091 applies to “stock or securities” and, by its terms, does not reach cryptocurrency. That means a cryptocurrency holder can sell crypto at a loss to harvest a tax deduction and immediately repurchase the same position. This strategy is not available for stocks. The CLARITY Act and parallel tax proposals are widely expected to close this loophole. Clients who rely on year-end crypto loss harvesting should be counseled that the window may shut quickly, potentially without a long transition period. Practitioners should document the planning rationale for any harvesting done in 2026 while the exemption still exists and flag any post-enactment transition rules as they emerge.

- EXPANDED TAX REPORTING AND THE 1099-DA REGIME. Form 1099-DA is already in effect for 2025 transactions, and the CLARITY Act would expand the definition of “broker” required to file it, pulling in additional platforms. For holders, that means more transactions will be reported directly to the IRS, closing much of the visibility gap on unreported gains. Clients with activity on smaller or DeFi-adjacent platforms may have reporting exposures that should be identified and addressed proactively before the IRS begins cross-referencing data. Practitioners should map client exchange activity against the expanded broker definition now, because a retroactive cleanup is materially more expensive than getting it right in the current year.

-

START THE CFTC/SEC CLASSIFICATION CONVERSATION AND RECOGNIZE THE U.S.-OFFEROR TAILWIND. The bill’s core framework turns on whether a given digital asset is a “digital commodity” (CFTC) or an “investment contract asset” (SEC), and that classification drives the entire regulatory treatment of each transaction. For clients holding or dealing in less-established tokens, classification uncertainty should be part of current risk discussions – not something addressed after the rules are finalized. There is a related point worth exploring with issuer clients: because registered U.S. exchanges will, as a practical matter, only be able to list assets compliant with U.S. securities and commodities laws, the CLARITY Act is likely to be a meaningful competitive boost to U.S.-domiciled, compliant offerors, and a corresponding headwind for offshore projects that have historically relied on ambiguous U.S. distribution.

- WATCH THE DEFI EXCLUSION LANGUAGE CLOSELY. The bill carves out decentralized and peer-to-peer activity from registration, but the scope is still being negotiated. For clients building or investing in DeFi infrastructure, the difference between qualifying and not qualifying for the exclusion could determine whether the platform faces full broker-dealer-style regulation. And from a policy perspective, practitioners should expect regulators, plaintiffs, and legislators to continue pressing on this: the traditional exemptions from securities regulation rest on a counterparty’s sophistication, accreditation, or pre-existing relationship with the issuer. DeFi transactions satisfy none of those conditions. That gap makes the DeFi carve-out the most likely source of future enforcement actions, technical corrections, and retail-investor loss scenarios.

Conclusion

The CLARITY Act is the most serious attempt yet to give crypto a proper legal home in the United States. It is not perfect — the stablecoin-interest fight alone could derail it, and the DeFi carve-out is likely to be the source of the next generation of enforcement disputes — but the political momentum is real, and the administration is pushing hard. For holders, the most actionable near-term item is the crypto wash-sale window, which may not survive the bill. For practitioners, the work to do now is classification analysis, 1099-DA reporting review, and a careful read of the DeFi carve-out language as it evolves. Waiting for the final text is not a strategy.

Sources and References

- Scott Bessent, “Digital Assets Rules Need Clarity,” The Wall Street Journal (April 8, 2026), https://www.wsj.com/opinion/digital-assets-rules-need-clarity-6dfcab70.

- H.R. 3633, Digital Asset Market Clarity Act of 2025, 119th Congress — Congress.gov.

- U.S. Senate Committee on Banking, Housing, and Urban Affairs, “The Facts: The CLARITY Act” (January 13, 2026).

- Latham & Watkins, U.S. Crypto Policy Tracker (last updated February 2026).

- Arnold & Porter, “Clarifying the CLARITY Act: What To Know About the House Crypto Market Structure Bill and Its Path to Law” (August 2025).

- Morgan Lewis, “Crypto Clarity: SEC and CFTC Issue Comprehensive Crypto Asset Guidance” (March 2026).

- Congressional Research Service, “Crypto Legislation: An Overview of H.R. 3633, the CLARITY Act.”

- FinTech Weekly, “What Is the CLARITY Act?” (updated March/April 2026).

- CoinGecko API Blog, “What the CLARITY Act Means for Crypto” (March 9, 2026).

- Reuters, “Bessent urges Congress to pass crypto regulation bill” (April 8, 2026).

- CoinDesk, “U.S. Treasury’s Bessent calls out crypto ‘nihilists’ resisting market structure bill” (February 5, 2026).

- IRS Notice 2014-21 (property classification of cryptocurrency).

- Revenue Ruling 2023-14 (staking rewards as ordinary income).

- IRC § 1091 (wash-sale rules).

- Form 1099-DA final broker reporting regulations (effective 2025 transactions).