The global economic landscape at mid-year presents a striking divergence between American resilience and European stagnation. Speaking during a webinar on 1 July 2026, Christopher Dembik, senior investment advisor at Pictet Asset Management, argued that a maturing AI revolution is shifting its focus from raw computing power to the constraints of energy infrastructure.

While the US economy continues to defy stagflation fears through robust productivity gains, the Eurozone remains on a low-growth trajectory, with even major stimulus efforts unlikely to shift the long-term paradigm.

As investors navigate seasonal volatility and record-high levels of retail leverage in Asian markets, the strategic focus is moving toward cost efficiency and the “picks and shovels” of the digital age—specifically, the power grids required to fuel the next phase of automation.

A tale of two economies: Stagnation vs dynamism

The Eurozone is currently facing a period of “slow stagnation,” with economic growth expected to hover around its 1% potential for the foreseeable future. Even the ambitious €1trn German recovery plan, unveiled in February 2025, is expected to offer only a temporary boost between 2027 and 2029 before growth returns to its estimated long-term potential of 1–1.5%.

In sharp contrast, the US economy remains dynamic, with nearly every sector contributing positively. Approximately one-third of quarterly US growth is now supported by AI investments, while a “wealth effect” driven by the stock market sustains strong household consumption. Dembik argued that around 60% of US households face recession-like financial conditions, including rising consumer credit delinquencies, but that these do not pose a systemic risk.

Unlike the ECB, the Fed rarely raises rates only once

Furthermore, US labour productivity is rising above its long-term average, a measurable early effect of AI integration that could eventually push US potential growth toward 3%, according to Dembik.

The Fed’s high-stakes balancing act

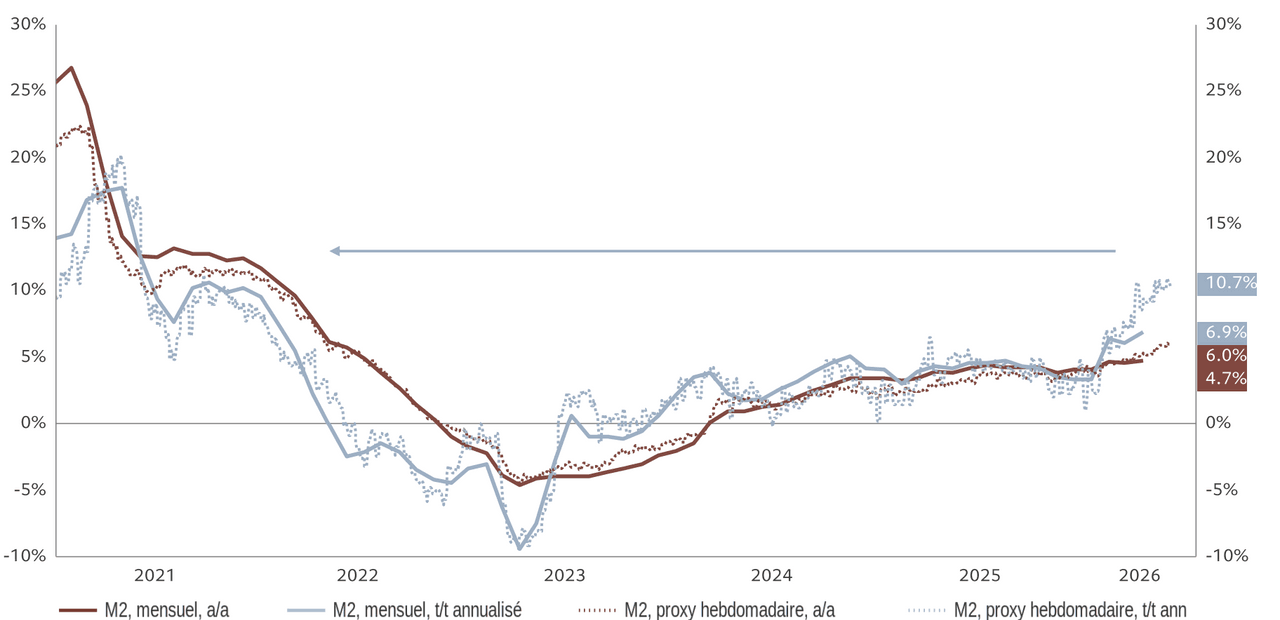

As shown in Chart 1, money supply is growing at a 10% annualised rate while inflation remains stubbornly above 3%. Against this backdrop, a contrarian but plausible scenario suggests the Fed may be forced to hike rates rather than cut them, despite Fed Chair Kevin Warsh arguing that AI will prove deflationary over the long term.

Chart 1: Broad money supply in the United States (monthly release and weekly proxy) Source: Refinitiv, Pictet Asset Management

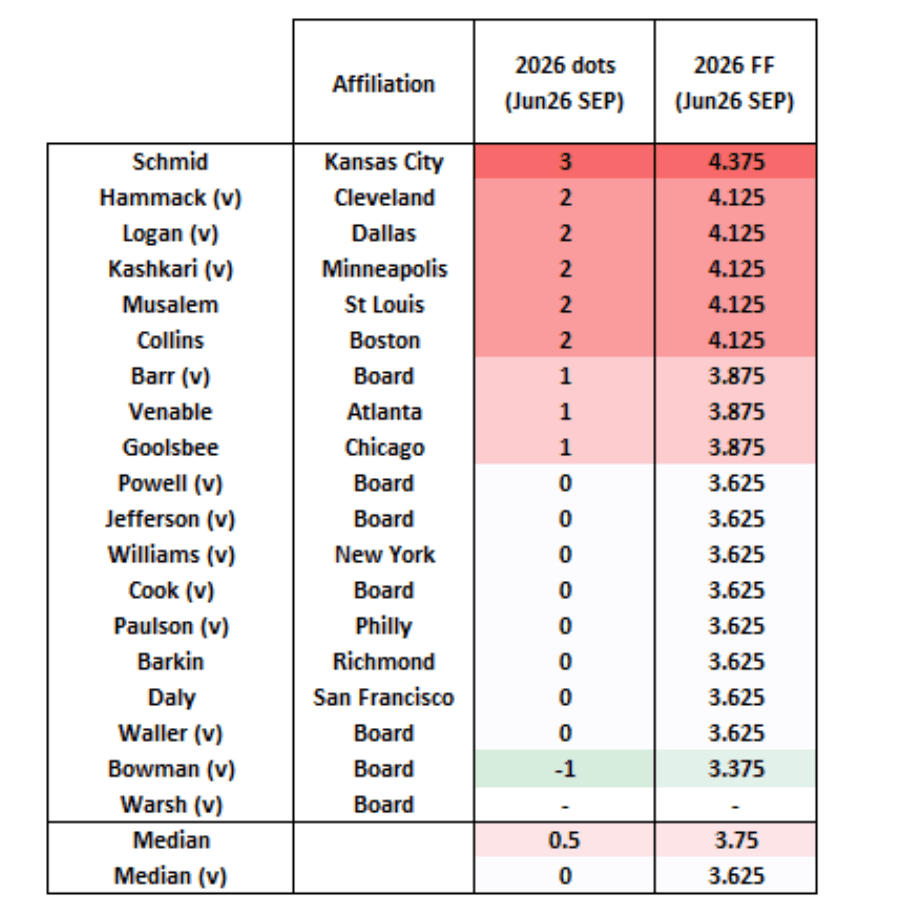

To return inflation to the 2% target, Dembik argued that the Fed might need to reverse the three “insurance cuts” of 2025, potentially implementing three 25-basis-point hikes totalling 75 basis points (see Chart 2). “Unlike the ECB, the Fed rarely raises rates only once,” he said. This minority view in the market, if realised, would trigger significant market volatility and necessitate hedging strategies, as the market has yet to price in such a hawkish pivot.

Chart 2: 2026 federal funds rate forecasts (FOMC dot plot, internal estimate) Source: Refinitiv, Pictet Asset Management (attribution des dots : estimation interne)

Beyond chips: The energy bottleneck in AI

Beyond the macroeconomic outlook, Dembik argued that investors should also rethink where value is emerging within the AI ecosystem. The AI sector is maturing, with the narrative shifting from spectacular demonstrations to large-scale, cost-effective deployment. While the focus has long been on semiconductor supply, the new “bottleneck” is energy infrastructure.

Connecting new data centres to existing power grids has become a primary challenge. For instance, Denmark recently signalled that it would prioritise the rest of its economy over energy supplies for data centres. Consequently, investment strategies are pivoting toward the energy value chain, specifically electricity providers and renewable energy storage, which offer the most rapidly deployable and cost-effective solutions for the growing power demands of AI and robotics.

Leverage and liquidity: Monitoring the red flags

Market stability is currently threatened by “extreme levels” of retail leverage, particularly in Asia. In South Korea, margin debt has reached $26bn—levels not seen since just before the dot-com bubble—leading to forced sales and trading halts during recent corrections.

Similarly, in the US, retail investors have moved from following trends to initiating them, with 50% of retail option activity now concentrated in “0DTE” (zero days to expiration) contracts. This explosion in leverage, combined with market liquidity that is increasingly concentrated in the largest 15 mega-cap stocks, creates a fragile environment where any sentiment shift can be rapidly amplified.

Strategic shifts in emerging markets and gold

In terms of asset allocation, there is a strong preference for emerging market debt in local currencies, supported by a structural downward trend in the US dollar. While Asian markets have seen a “salutary correction” in semiconductors, Dembik stressed that Latin American stocks remain attractive due to low valuations and resilience during geopolitical risks.

Finally, while gold is in a consolidation phase following a 15% drop linked to rising US bond yields, the long-term outlook remains positive, with 50% of global central banks planning to increase their gold reserves by year-end.